Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that TPC Plus Berhad (KLSE:TPC) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does TPC Plus Berhad Carry?

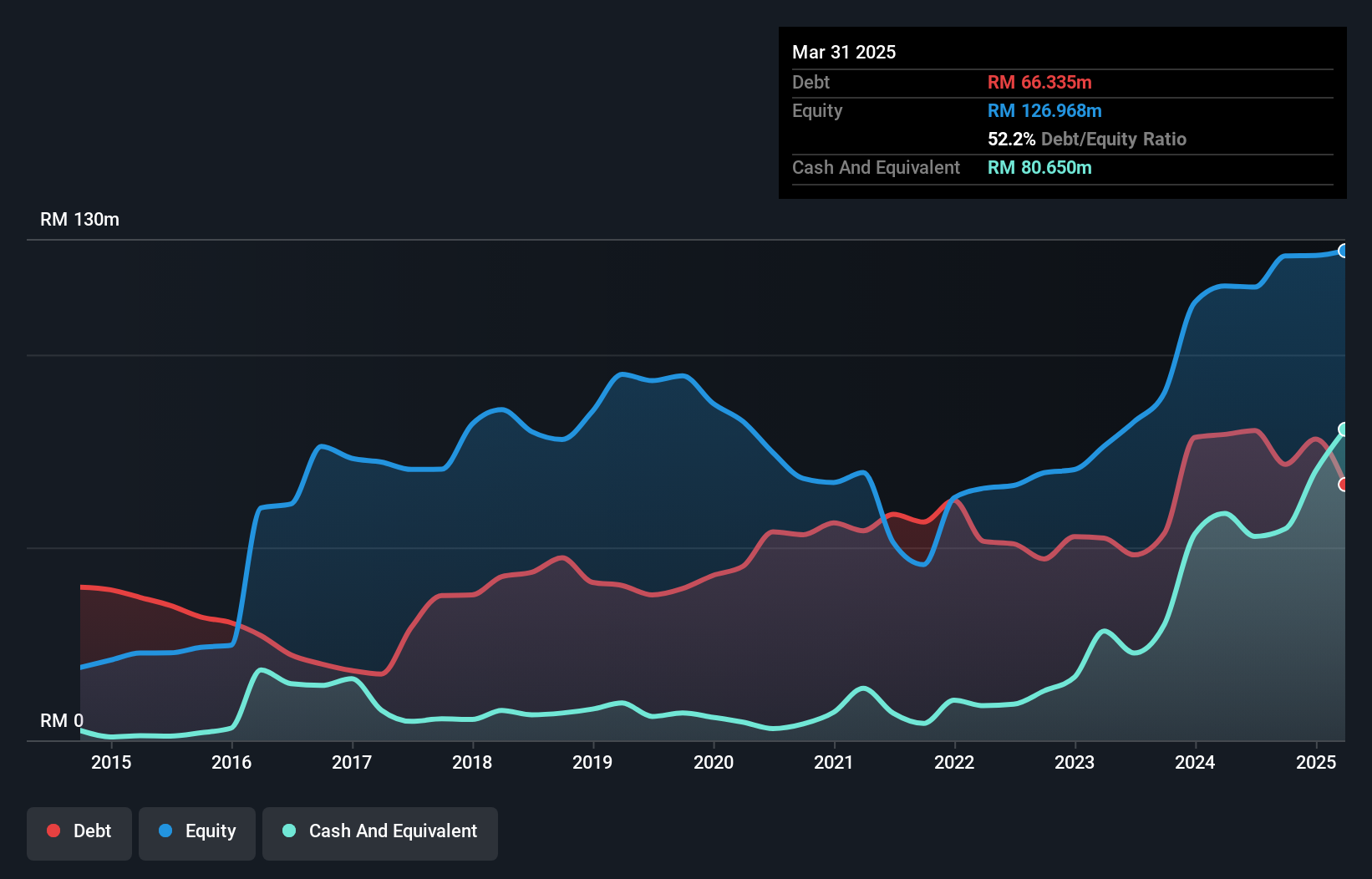

The image below, which you can click on for greater detail, shows that TPC Plus Berhad had debt of RM66.3m at the end of March 2025, a reduction from RM79.3m over a year. However, it does have RM80.7m in cash offsetting this, leading to net cash of RM14.3m.

How Healthy Is TPC Plus Berhad's Balance Sheet?

We can see from the most recent balance sheet that TPC Plus Berhad had liabilities of RM172.6m falling due within a year, and liabilities of RM32.5m due beyond that. Offsetting this, it had RM80.7m in cash and RM96.4m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by RM28.1m.

This deficit isn't so bad because TPC Plus Berhad is worth RM104.8m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. Despite its noteworthy liabilities, TPC Plus Berhad boasts net cash, so it's fair to say it does not have a heavy debt load!

View our latest analysis for TPC Plus Berhad

Shareholders should be aware that TPC Plus Berhad's EBIT was down 80% last year. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. When analysing debt levels, the balance sheet is the obvious place to start. But it is TPC Plus Berhad's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While TPC Plus Berhad has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, TPC Plus Berhad actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing Up

While TPC Plus Berhad does have more liabilities than liquid assets, it also has net cash of RM14.3m. And it impressed us with free cash flow of RM49m, being 2,096% of its EBIT. So we are not troubled with TPC Plus Berhad's debt use. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 2 warning signs for TPC Plus Berhad you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if TPC Plus Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TPC

TPC Plus Berhad

An investment holding company, engages in the poultry farming business in Malaysia.

Excellent balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|60.9% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|19.7% undervalued

ZW

Community Contributor