Advertisement

Do You Know What Leong Hup International Berhad's (KLSE:LHI) P/E Ratio Means?

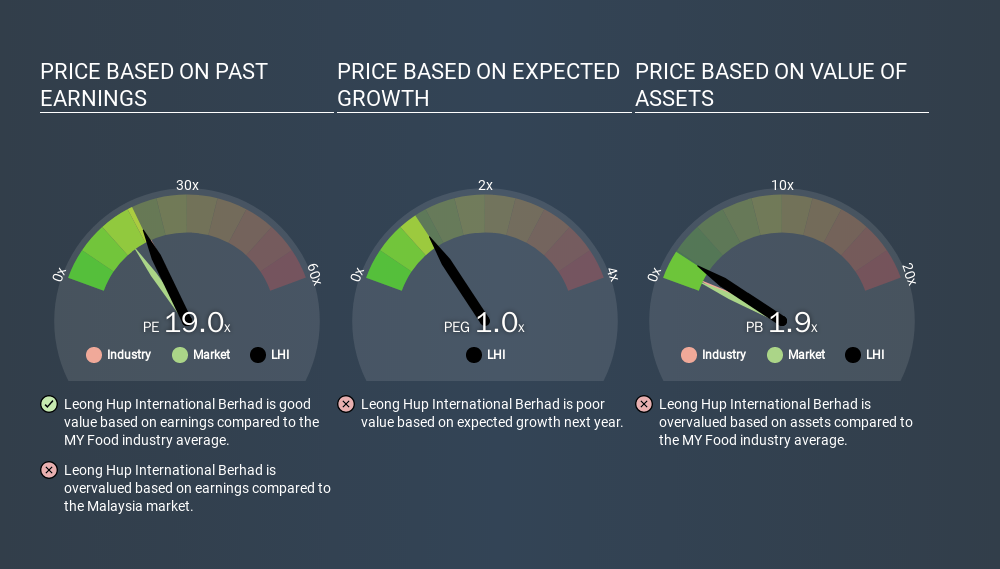

The goal of this article is to teach you how to use price to earnings ratios (P/E ratios). We'll look at Leong Hup International Berhad's (KLSE:LHI) P/E ratio and reflect on what it tells us about the company's share price. Leong Hup International Berhad has a price to earnings ratio of 18.99, based on the last twelve months. That means that at current prices, buyers pay MYR18.99 for every MYR1 in trailing yearly profits.

See our latest analysis for Leong Hup International Berhad

How Do You Calculate A P/E Ratio?

The formula for P/E is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for Leong Hup International Berhad:

P/E of 18.99 = MYR0.83 ÷ MYR0.04 (Based on the year to September 2019.)

Is A High Price-to-Earnings Ratio Good?

The higher the P/E ratio, the higher the price tag of a business, relative to its trailing earnings. That isn't a good or a bad thing on its own, but a high P/E means that buyers have a higher opinion of the business's prospects, relative to stocks with a lower P/E.

Does Leong Hup International Berhad Have A Relatively High Or Low P/E For Its Industry?

We can get an indication of market expectations by looking at the P/E ratio. The image below shows that Leong Hup International Berhad has a P/E ratio that is roughly in line with the food industry average (19.7).

Its P/E ratio suggests that Leong Hup International Berhad shareholders think that in the future it will perform about the same as other companies in its industry classification. The company could surprise by performing better than average, in the future. Checking factors such as director buying and selling. could help you form your own view on if that will happen.

How Growth Rates Impact P/E Ratios

When earnings fall, the 'E' decreases, over time. That means unless the share price falls, the P/E will increase in a few years. Then, a higher P/E might scare off shareholders, pushing the share price down.

Leong Hup International Berhad shrunk earnings per share by 20% over the last year. But over the longer term (5 years) earnings per share have increased by 6.4%. And EPS is down 6.4% a year, over the last 3 years. This could justify a low P/E.

Remember: P/E Ratios Don't Consider The Balance Sheet

The 'Price' in P/E reflects the market capitalization of the company. In other words, it does not consider any debt or cash that the company may have on the balance sheet. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Spending on growth might be good or bad a few years later, but the point is that the P/E ratio does not account for the option (or lack thereof).

Leong Hup International Berhad's Balance Sheet

Leong Hup International Berhad has net debt worth 57% of its market capitalization. If you want to compare its P/E ratio to other companies, you should absolutely keep in mind it has significant borrowings.

The Bottom Line On Leong Hup International Berhad's P/E Ratio

Leong Hup International Berhad has a P/E of 19.0. That's higher than the average in its market, which is 14.7. With relatively high debt, and no earnings per share growth over twelve months, it's safe to say the market believes the company will improve its earnings growth in the future.

When the market is wrong about a stock, it gives savvy investors an opportunity. If the reality for a company is better than it expects, you can make money by buying and holding for the long term. So this free visual report on analyst forecasts could hold the key to an excellent investment decision.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with modest (or no) debt, trading on a P/E below 20.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About KLSE:LHI

Leong Hup International Berhad

Operates as a poultry producers in Malaysia, Singapore, Indonesia, Vietnam, and the Philippines.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor