Advertisement

Hap Seng Plantations Holdings Berhad (KLSE:HSPLANT) Is Increasing Its Dividend To MYR0.05

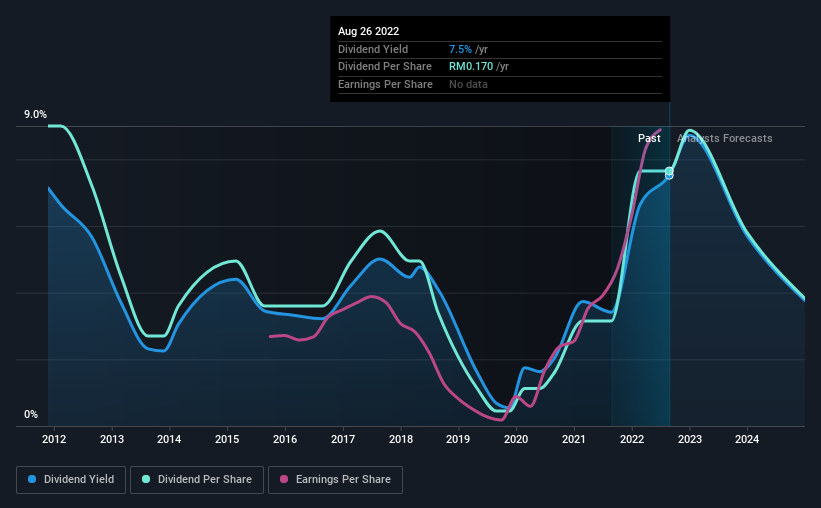

Hap Seng Plantations Holdings Berhad's (KLSE:HSPLANT) periodic dividend will be increasing on the 22nd of September to MYR0.05, with investors receiving 233% more than last year's MYR0.015. This takes the dividend yield to 7.5%, which shareholders will be pleased with.

Check out our latest analysis for Hap Seng Plantations Holdings Berhad

Hap Seng Plantations Holdings Berhad Is Paying Out More Than It Is Earning

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. The last dividend was quite easily covered by Hap Seng Plantations Holdings Berhad's earnings. This indicates that a lot of the earnings are being reinvested into the business, with the aim of fueling growth.

Looking forward, earnings per share is forecast to fall by 63.7% over the next year. If the dividend continues along the path it has been on recently, the payout ratio in 12 months could be 147%, which is definitely a bit high to be sustainable going forward.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The annual payment during the last 10 years was MYR0.20 in 2012, and the most recent fiscal year payment was MYR0.17. This works out to be a decline of approximately 1.6% per year over that time. A company that decreases its dividend over time generally isn't what we are looking for.

The Dividend Looks Likely To Grow

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. We are encouraged to see that Hap Seng Plantations Holdings Berhad has grown earnings per share at 18% per year over the past five years. Shareholders are getting plenty of the earnings returned to them, which combined with strong growth makes this quite appealing.

Hap Seng Plantations Holdings Berhad Looks Like A Great Dividend Stock

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. The earnings easily cover the company's distributions, and the company is generating plenty of cash. If earnings do fall over the next 12 months, the dividend could be buffeted a little bit, but we don't think it should cause too much of a problem in the long term. All of these factors considered, we think this has solid potential as a dividend stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Case in point: We've spotted 2 warning signs for Hap Seng Plantations Holdings Berhad (of which 1 can't be ignored!) you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Hap Seng Plantations Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:HSPLANT

Hap Seng Plantations Holdings Berhad

An investment holding company, operates as an oil palm plantation company in Malaysia.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor