Advertisement

- Malaysia

- /

- Energy Services

- /

- KLSE:DAYANG

Is Dayang Enterprise Holdings Bhd (KLSE:DAYANG) Using Too Much Debt?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Dayang Enterprise Holdings Bhd (KLSE:DAYANG) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Dayang Enterprise Holdings Bhd

What Is Dayang Enterprise Holdings Bhd's Debt?

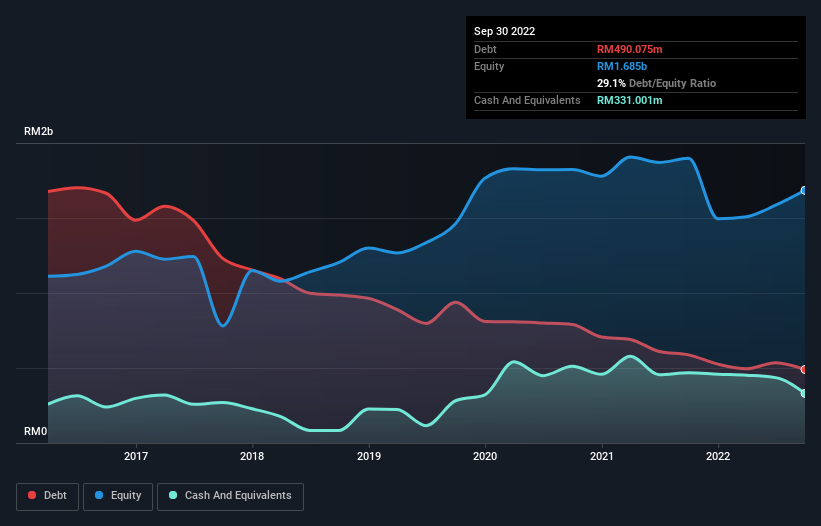

As you can see below, Dayang Enterprise Holdings Bhd had RM490.1m of debt at September 2022, down from RM587.6m a year prior. However, because it has a cash reserve of RM331.0m, its net debt is less, at about RM159.1m.

How Strong Is Dayang Enterprise Holdings Bhd's Balance Sheet?

The latest balance sheet data shows that Dayang Enterprise Holdings Bhd had liabilities of RM391.9m due within a year, and liabilities of RM466.3m falling due after that. On the other hand, it had cash of RM331.0m and RM498.2m worth of receivables due within a year. So it has liabilities totalling RM29.1m more than its cash and near-term receivables, combined.

Having regard to Dayang Enterprise Holdings Bhd's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the RM1.68b company is struggling for cash, we still think it's worth monitoring its balance sheet.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While Dayang Enterprise Holdings Bhd's low debt to EBITDA ratio of 0.59 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 6.8 times last year does give us pause. So we'd recommend keeping a close eye on the impact financing costs are having on the business. Even more impressive was the fact that Dayang Enterprise Holdings Bhd grew its EBIT by 394% over twelve months. That boost will make it even easier to pay down debt going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Dayang Enterprise Holdings Bhd can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Dayang Enterprise Holdings Bhd actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

The good news is that Dayang Enterprise Holdings Bhd's demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. And the good news does not stop there, as its EBIT growth rate also supports that impression! Considering this range of factors, it seems to us that Dayang Enterprise Holdings Bhd is quite prudent with its debt, and the risks seem well managed. So the balance sheet looks pretty healthy, to us. While Dayang Enterprise Holdings Bhd didn't make a statutory profit in the last year, its positive EBIT suggests that profitability might not be far away. Click here to see if its earnings are heading in the right direction, over the medium term.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:DAYANG

Dayang Enterprise Holdings Bhd

An investment holding company, provides offshore topside maintenance services, minor fabrication works, and offshore hook-up and commissioning services to the oil and gas companies in Malaysia.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor