Advertisement

- Malaysia

- /

- Consumer Durables

- /

- KLSE:PARAGON

Paragon Union Berhad (KLSE:PARAGON) Is Making Moderate Use Of Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Paragon Union Berhad (KLSE:PARAGON) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Paragon Union Berhad

What Is Paragon Union Berhad's Debt?

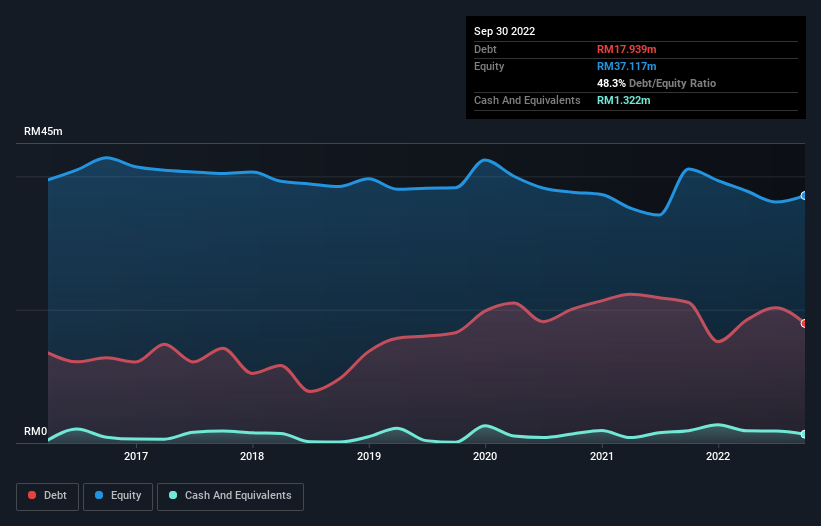

The image below, which you can click on for greater detail, shows that Paragon Union Berhad had debt of RM17.9m at the end of September 2022, a reduction from RM21.1m over a year. However, because it has a cash reserve of RM1.32m, its net debt is less, at about RM16.6m.

How Strong Is Paragon Union Berhad's Balance Sheet?

The latest balance sheet data shows that Paragon Union Berhad had liabilities of RM22.9m due within a year, and liabilities of RM10.7m falling due after that. On the other hand, it had cash of RM1.32m and RM15.4m worth of receivables due within a year. So its liabilities total RM16.9m more than the combination of its cash and short-term receivables.

Given Paragon Union Berhad has a market capitalization of RM189.5m, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Paragon Union Berhad will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Paragon Union Berhad reported revenue of RM62m, which is a gain of 66%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

Despite the top line growth, Paragon Union Berhad still had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at RM13m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through RM5.6m of cash over the last year. So suffice it to say we do consider the stock to be risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 3 warning signs we've spotted with Paragon Union Berhad (including 2 which shouldn't be ignored) .

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:PARAGON

Paragon Union Berhad

An investment holding company, engages in the manufacturing and trading of car and commercial carpets, and automotive components.

Adequate balance sheet very low.

Similar Companies

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|60.9% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|19.7% undervalued

ZW

Community Contributor