Advertisement

- Malaysia

- /

- Consumer Durables

- /

- KLSE:PANAMY

Panasonic Manufacturing Malaysia Berhad's (KLSE:PANAMY) Dividend Will Be MYR0.47

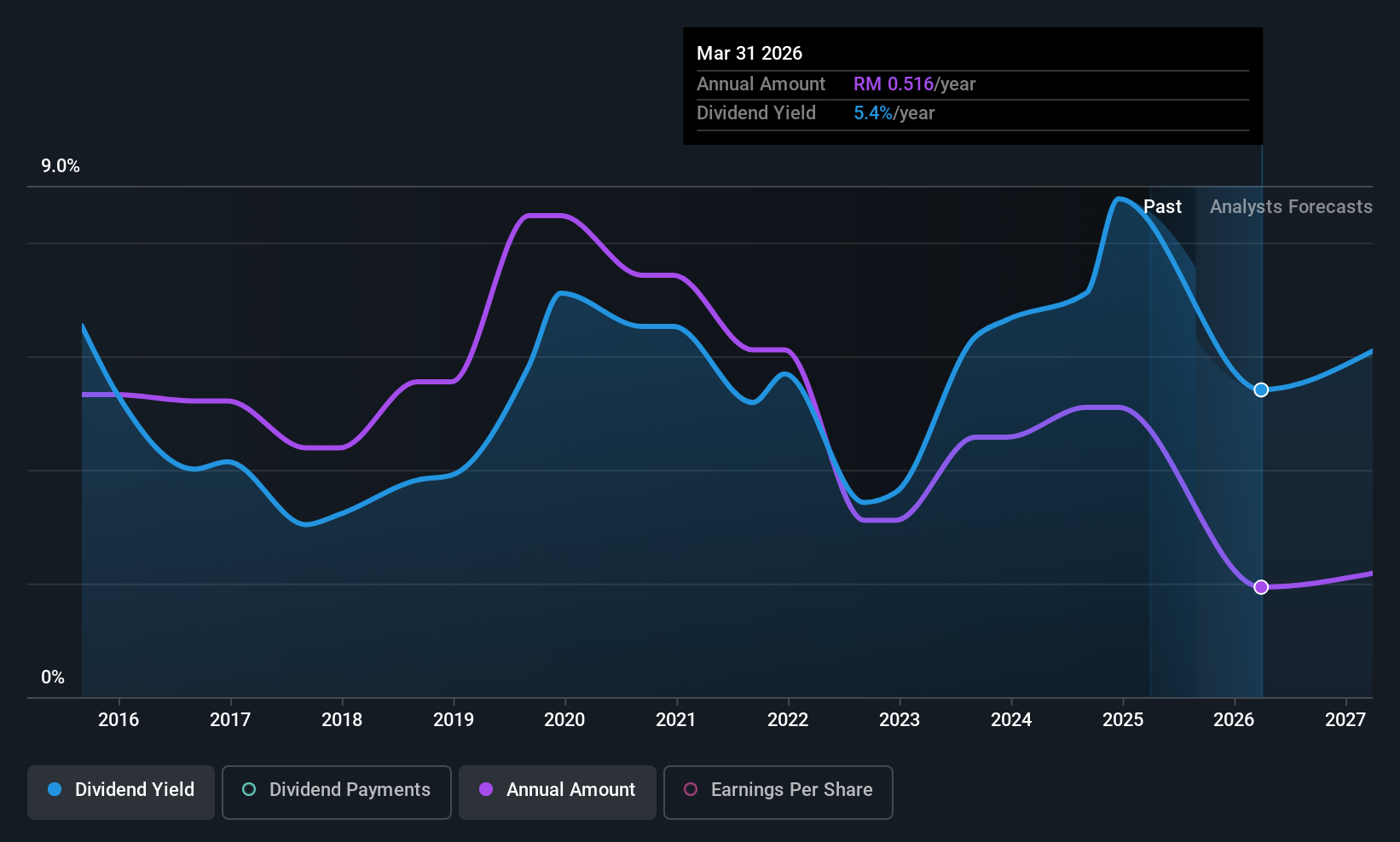

Panasonic Manufacturing Malaysia Berhad (KLSE:PANAMY) will pay a dividend of MYR0.47 on the 19th of September. The yield is still above the industry average at 6.5%.

Panasonic Manufacturing Malaysia Berhad's Payment Could Potentially Have Solid Earnings Coverage

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Before making this announcement, the company's dividend was much higher than its earnings. It will be difficult to sustain this level of payout so we wouldn't be confident about this continuing.

EPS is set to grow by 14.9% over the next year. Assuming the dividend continues along recent trends, our estimates say the payout ratio could reach 92% - on the higher side, but we wouldn't necessarily say this is unsustainable.

See our latest analysis for Panasonic Manufacturing Malaysia Berhad

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. The annual payment during the last 10 years was MYR0.50 in 2015, and the most recent fiscal year payment was MYR0.62. This works out to be a compound annual growth rate (CAGR) of approximately 2.2% a year over that time. It's encouraging to see some dividend growth, but the dividend has been cut at least once, and the size of the cut would eliminate most of the growth anyway, which makes this less attractive as an income investment.

The Dividend Has Limited Growth Potential

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Panasonic Manufacturing Malaysia Berhad's EPS has fallen by approximately 16% per year during the past five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future. Over the next year, however, earnings are actually predicted to rise, but we would still be cautious until a track record of earnings growth can be built.

We're Not Big Fans Of Panasonic Manufacturing Malaysia Berhad's Dividend

In summary, it's not great to see that the dividend is being cut, but it is probably understandable given that the current payment level was quite high. The company seems to be stretching itself a bit to make such big payments, but it doesn't appear they can be consistent over time. Overall, the dividend is not reliable enough to make this a good income stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Just as an example, we've come across 2 warning signs for Panasonic Manufacturing Malaysia Berhad you should be aware of, and 1 of them shouldn't be ignored. Is Panasonic Manufacturing Malaysia Berhad not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:PANAMY

Panasonic Manufacturing Malaysia Berhad

Manufactures and sells electrical home appliances and related components in Malaysia, Japan, rest of Asia, Europe, the Middle East, and internationally.

Flawless balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|49.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|7.0% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|22.5% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|52.5% overvalued

RO

Community Contributor