Advertisement

Magni-Tech Industries Berhad (KLSE:MAGNI) Could Be A Buy For Its Upcoming Dividend

Readers hoping to buy Magni-Tech Industries Berhad (KLSE:MAGNI) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. Investors can purchase shares before the 17th of December in order to be eligible for this dividend, which will be paid on the 8th of January.

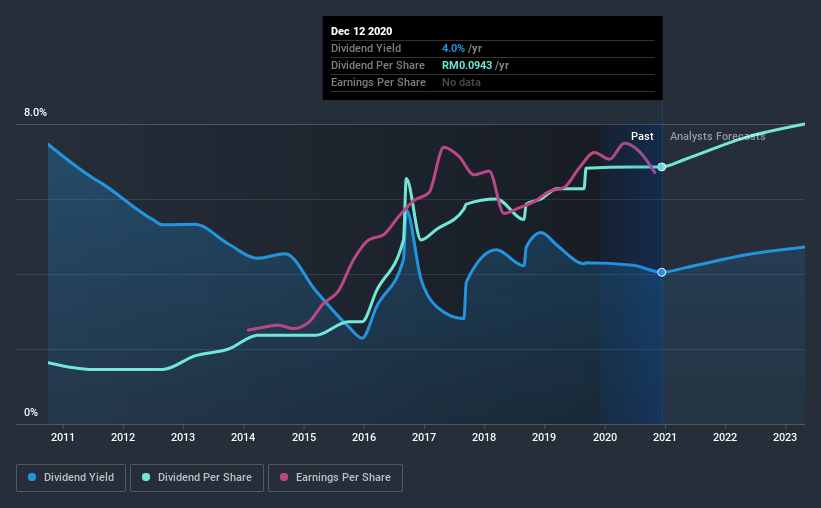

Magni-Tech Industries Berhad's next dividend payment will be RM0.018 per share, on the back of last year when the company paid a total of RM0.094 to shareholders. Looking at the last 12 months of distributions, Magni-Tech Industries Berhad has a trailing yield of approximately 4.0% on its current stock price of MYR2.33. If you buy this business for its dividend, you should have an idea of whether Magni-Tech Industries Berhad's dividend is reliable and sustainable. So we need to investigate whether Magni-Tech Industries Berhad can afford its dividend, and if the dividend could grow.

View our latest analysis for Magni-Tech Industries Berhad

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Magni-Tech Industries Berhad paid out a comfortable 32% of its profit last year. A useful secondary check can be to evaluate whether Magni-Tech Industries Berhad generated enough free cash flow to afford its dividend. Thankfully its dividend payments took up just 40% of the free cash flow it generated, which is a comfortable payout ratio.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see how much of its profit Magni-Tech Industries Berhad paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. For this reason, we're glad to see Magni-Tech Industries Berhad's earnings per share have risen 16% per annum over the last five years. Earnings per share are growing rapidly and the company is keeping more than half of its earnings within the business; an attractive combination which could suggest the company is focused on reinvesting to grow earnings further. Fast-growing businesses that are reinvesting heavily are enticing from a dividend perspective, especially since they can often increase the payout ratio later.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. In the past 10 years, Magni-Tech Industries Berhad has increased its dividend at approximately 15% a year on average. It's exciting to see that both earnings and dividends per share have grown rapidly over the past few years.

To Sum It Up

From a dividend perspective, should investors buy or avoid Magni-Tech Industries Berhad? It's great that Magni-Tech Industries Berhad is growing earnings per share while simultaneously paying out a low percentage of both its earnings and cash flow. It's disappointing to see the dividend has been cut at least once in the past, but as things stand now, the low payout ratio suggests a conservative approach to dividends, which we like. There's a lot to like about Magni-Tech Industries Berhad, and we would prioritise taking a closer look at it.

So while Magni-Tech Industries Berhad looks good from a dividend perspective, it's always worthwhile being up to date with the risks involved in this stock. In terms of investment risks, we've identified 1 warning sign with Magni-Tech Industries Berhad and understanding them should be part of your investment process.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Magni-Tech Industries Berhad, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KLSE:MAGNI

Magni-Tech Industries Berhad

An investment holding company, engages in the manufacture and sale of garments and packaging materials in Malaysia and Vietnam.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

92 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative