Advertisement

- Malaysia

- /

- Healthcare Services

- /

- KLSE:G3

We Think G3 Global Berhad (KLSE:G3) Can Afford To Drive Business Growth

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So, the natural question for G3 Global Berhad (KLSE:G3) shareholders is whether they should be concerned by its rate of cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. Let's start with an examination of the business' cash, relative to its cash burn.

View our latest analysis for G3 Global Berhad

When Might G3 Global Berhad Run Out Of Money?

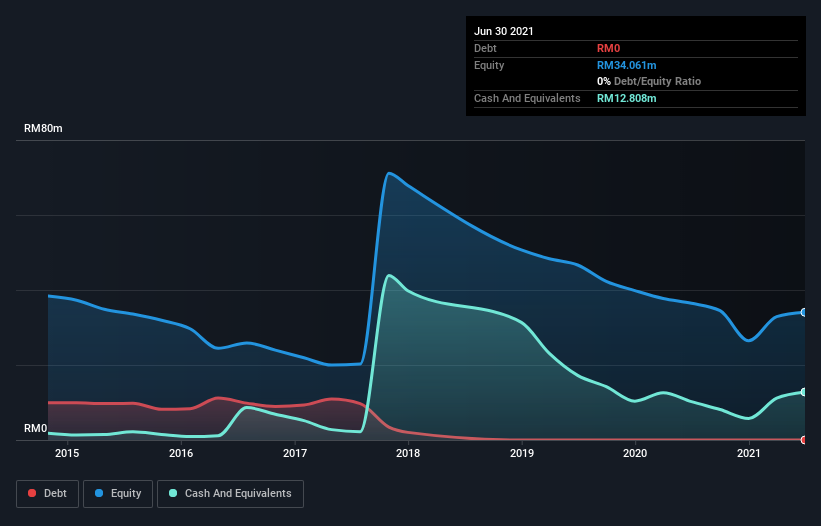

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. In June 2021, G3 Global Berhad had RM13m in cash, and was debt-free. Importantly, its cash burn was RM4.4m over the trailing twelve months. So it had a cash runway of about 2.9 years from June 2021. That's decent, giving the company a couple years to develop its business. You can see how its cash balance has changed over time in the image below.

Is G3 Global Berhad's Revenue Growing?

Given that G3 Global Berhad actually had positive free cash flow last year, before burning cash this year, we'll focus on its operating revenue to get a measure of the business trajectory. Unfortunately, the last year has been a disappointment, with operating revenue dropping 23% during the period. Of course, we've only taken a quick look at the stock's growth metrics, here. This graph of historic earnings and revenue shows how G3 Global Berhad is building its business over time.

How Hard Would It Be For G3 Global Berhad To Raise More Cash For Growth?

Given its problematic fall in revenue, G3 Global Berhad shareholders should consider how the company could fund its growth, if it turns out it needs more cash. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Many companies end up issuing new shares to fund future growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

G3 Global Berhad's cash burn of RM4.4m is about 2.9% of its RM151m market capitalisation. So it could almost certainly just borrow a little to fund another year's growth, or else easily raise the cash by issuing a few shares.

So, Should We Worry About G3 Global Berhad's Cash Burn?

It may already be apparent to you that we're relatively comfortable with the way G3 Global Berhad is burning through its cash. In particular, we think its cash runway stands out as evidence that the company is well on top of its spending. While its falling revenue wasn't great, the other factors mentioned in this article more than make up for weakness on that measure. After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash, as it seems on track to meet its needs over the medium term. On another note, we conducted an in-depth investigation of the company, and identified 6 warning signs for G3 Global Berhad (2 can't be ignored!) that you should be aware of before investing here.

Of course G3 Global Berhad may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:G3

G3 Global Berhad

An investment holding company, provides information and communication technology services in Malaysia.

Flawless balance sheet with very low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor