Advertisement

- Malaysia

- /

- Electrical

- /

- KLSE:SCOMNET

Supercomnet Technologies Berhad's (KLSE:SCOMNET) 26% Price Boost Is Out Of Tune With Earnings

Supercomnet Technologies Berhad (KLSE:SCOMNET) shareholders would be excited to see that the share price has had a great month, posting a 26% gain and recovering from prior weakness. Looking further back, the 14% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

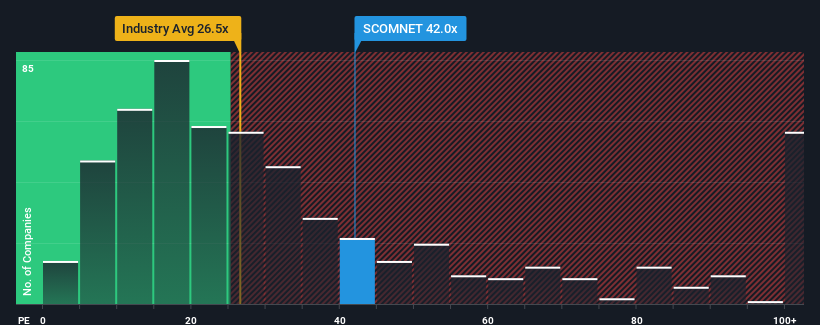

Since its price has surged higher, Supercomnet Technologies Berhad may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 42x, since almost half of all companies in Malaysia have P/E ratios under 16x and even P/E's lower than 10x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Supercomnet Technologies Berhad could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be extremely nervous about the viability of the share price.

Check out our latest analysis for Supercomnet Technologies Berhad

Is There Enough Growth For Supercomnet Technologies Berhad?

In order to justify its P/E ratio, Supercomnet Technologies Berhad would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered a frustrating 11% decrease to the company's bottom line. This has erased any of its gains during the last three years, with practically no change in EPS being achieved in total. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Shifting to the future, estimates from the three analysts covering the company suggest earnings should grow by 15% over the next year. With the market predicted to deliver 17% growth , the company is positioned for a weaker earnings result.

In light of this, it's alarming that Supercomnet Technologies Berhad's P/E sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Key Takeaway

Shares in Supercomnet Technologies Berhad have built up some good momentum lately, which has really inflated its P/E. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Supercomnet Technologies Berhad currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for Supercomnet Technologies Berhad that you should be aware of.

If you're unsure about the strength of Supercomnet Technologies Berhad's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:SCOMNET

Supercomnet Technologies Berhad

Engages in the manufacture and sale of PVC compounds, and cables and wires for electronic devices and data control switches in Malaysia, the Dominican Republic, the United States, Denmark, Singapore, Taiwan, and Hong Kong.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|8.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.6% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor