Advertisement

Sarawak Consolidated Industries Berhad's (KLSE:SCIB) Financials Are Too Obscure To Link With Current Share Price Momentum: What's In Store For the Stock?

Sarawak Consolidated Industries Berhad (KLSE:SCIB) has had a great run on the share market with its stock up by a significant 11% over the last week. But the company's key financial indicators appear to be differing across the board and that makes us question whether or not the company's current share price momentum can be maintained. Particularly, we will be paying attention to Sarawak Consolidated Industries Berhad's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

View our latest analysis for Sarawak Consolidated Industries Berhad

How To Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Sarawak Consolidated Industries Berhad is:

3.2% = RM4.8m ÷ RM152m (Based on the trailing twelve months to June 2024).

The 'return' is the profit over the last twelve months. Another way to think of that is that for every MYR1 worth of equity, the company was able to earn MYR0.03 in profit.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

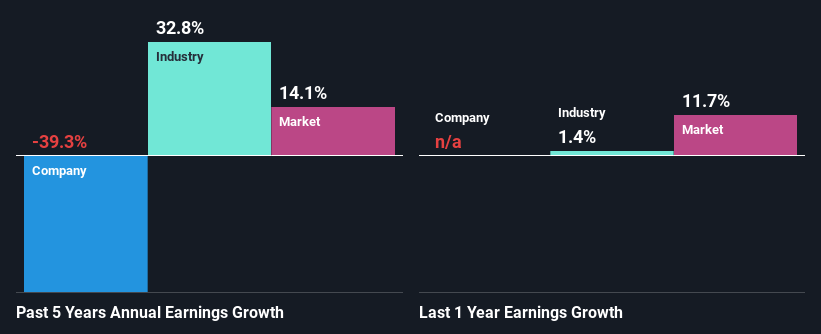

A Side By Side comparison of Sarawak Consolidated Industries Berhad's Earnings Growth And 3.2% ROE

It is hard to argue that Sarawak Consolidated Industries Berhad's ROE is much good in and of itself. Even compared to the average industry ROE of 4.8%, the company's ROE is quite dismal. Given the circumstances, the significant decline in net income by 39% seen by Sarawak Consolidated Industries Berhad over the last five years is not surprising. We reckon that there could also be other factors at play here. For instance, the company has a very high payout ratio, or is faced with competitive pressures.

That being said, we compared Sarawak Consolidated Industries Berhad's performance with the industry and were concerned when we found that while the company has shrunk its earnings, the industry has grown its earnings at a rate of 33% in the same 5-year period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Sarawak Consolidated Industries Berhad is trading on a high P/E or a low P/E, relative to its industry.

Is Sarawak Consolidated Industries Berhad Using Its Retained Earnings Effectively?

Sarawak Consolidated Industries Berhad doesn't pay any regular dividends, meaning that potentially all of its profits are being reinvested in the business, which doesn't explain why the company's earnings have shrunk if it is retaining all of its profits. So there could be some other explanations in that regard. For instance, the company's business may be deteriorating.

Summary

In total, we're a bit ambivalent about Sarawak Consolidated Industries Berhad's performance. Even though it appears to be retaining most of its profits, given the low ROE, investors may not be benefitting from all that reinvestment after all. The low earnings growth suggests our theory correct. Wrapping up, we would proceed with caution with this company and one way of doing that would be to look at the risk profile of the business. You can see the 3 risks we have identified for Sarawak Consolidated Industries Berhad by visiting our risks dashboard for free on our platform here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:SCIB

Sarawak Consolidated Industries Berhad

An investment holding company, manufactures and sells precast concrete products and industrialized building systems for use in the infrastructure and construction industries primarily in Malaysia.

Adequate balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor