Advertisement

- Malaysia

- /

- Trade Distributors

- /

- KLSE:SCC

Capital Allocation Trends At SCC Holdings Berhad (KLSE:SCC) Aren't Ideal

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Although, when we looked at SCC Holdings Berhad (KLSE:SCC), it didn't seem to tick all of these boxes.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for SCC Holdings Berhad, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

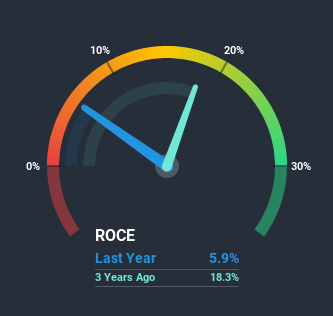

0.059 = RM2.6m ÷ (RM51m - RM6.3m) (Based on the trailing twelve months to December 2020).

Therefore, SCC Holdings Berhad has an ROCE of 5.9%. On its own that's a low return on capital but it's in line with the industry's average returns of 6.4%.

Check out our latest analysis for SCC Holdings Berhad

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of SCC Holdings Berhad, check out these free graphs here.

So How Is SCC Holdings Berhad's ROCE Trending?

In terms of SCC Holdings Berhad's historical ROCE movements, the trend isn't fantastic. To be more specific, ROCE has fallen from 23% over the last five years. And considering revenue has dropped while employing more capital, we'd be cautious. This could mean that the business is losing its competitive advantage or market share, because while more money is being put into ventures, it's actually producing a lower return - "less bang for their buck" per se.

In Conclusion...

In summary, we're somewhat concerned by SCC Holdings Berhad's diminishing returns on increasing amounts of capital. Investors must expect better things on the horizon though because the stock has risen 5.6% in the last five years. Regardless, we don't like the trends as they are and if they persist, we think you might find better investments elsewhere.

One final note, you should learn about the 3 warning signs we've spotted with SCC Holdings Berhad (including 1 which makes us a bit uncomfortable) .

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

When trading SCC Holdings Berhad or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:SCC

SCC Holdings Berhad

An investment holding company, engages in the distribution, marketing, and sale of food service equipment and animal health products in Malaysia.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor