Advertisement

What Did Resintech Berhad's (KLSE:RESINTC) CEO Take Home Last Year?

The CEO of Resintech Berhad (KLSE:RESINTC) is Kim Teh, and this article examines the executive's compensation against the backdrop of overall company performance. This analysis will also look to assess whether the CEO is appropriately paid, considering recent earnings growth and investor returns for Resintech Berhad.

Check out our latest analysis for Resintech Berhad

How Does Total Compensation For Kim Teh Compare With Other Companies In The Industry?

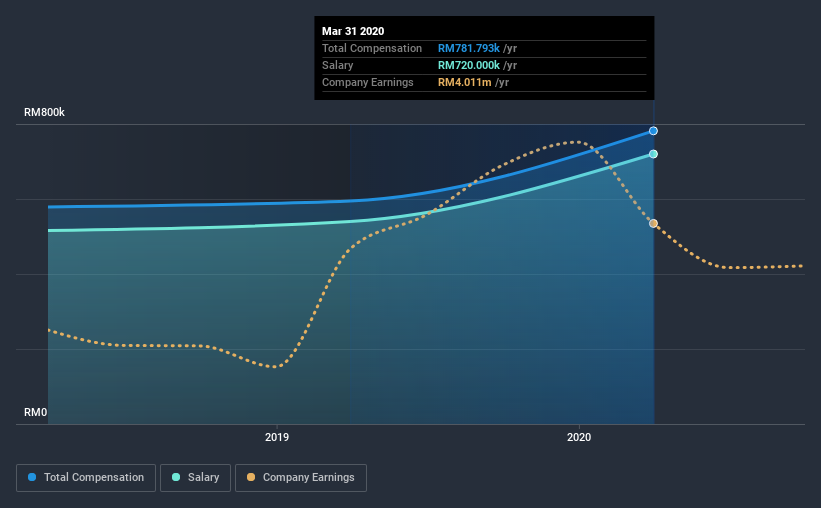

At the time of writing, our data shows that Resintech Berhad has a market capitalization of RM51m, and reported total annual CEO compensation of RM782k for the year to March 2020. That's a notable increase of 31% on last year. We note that the salary portion, which stands at RM720.0k constitutes the majority of total compensation received by the CEO.

For comparison, other companies in the industry with market capitalizations below RM808m, reported a median total CEO compensation of RM340k. Hence, we can conclude that Kim Teh is remunerated higher than the industry median. Furthermore, Kim Teh directly owns RM25m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | RM720k | RM540k | 92% |

| Other | RM62k | RM55k | 8% |

| Total Compensation | RM782k | RM595k | 100% |

Speaking on an industry level, nearly 71% of total compensation represents salary, while the remainder of 29% is other remuneration. According to our research, Resintech Berhad has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Resintech Berhad's Growth Numbers

Over the last three years, Resintech Berhad has shrunk its earnings per share by 27% per year. In the last year, its revenue is down 19%.

Overall this is not a very positive result for shareholders. And the impression is worse when you consider revenue is down year-on-year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Resintech Berhad Been A Good Investment?

With a total shareholder return of 20% over three years, Resintech Berhad shareholders would, in general, be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

To Conclude...

As previously discussed, Kim is compensated more than what is normal for CEOs of companies of similar size, and which belong to the same industry. Meanwhile, EPS has not been growing sufficiently to impress us, over the last three years. And shareholder returns are decent but not great. So you can understand why we do not think CEO compensation is particularly modest!

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. That's why we did our research, and identified 5 warning signs for Resintech Berhad (of which 1 is a bit concerning!) that you should know about in order to have a holistic understanding of the stock.

Important note: Resintech Berhad is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you decide to trade Resintech Berhad, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:RESINTC

Resintech Berhad

An investment holding company, designs, manufactures, trades, and markets uPVC and polyethylene products in Malaysia, Indonesia, Cambodia, Singapore, and internationally.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor