Advertisement

- Malaysia

- /

- Trade Distributors

- /

- KLSE:PGLOBE

Health Check: How Prudently Does Paragon Globe Berhad (KLSE:PGLOBE) Use Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Paragon Globe Berhad (KLSE:PGLOBE) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Paragon Globe Berhad

What Is Paragon Globe Berhad's Net Debt?

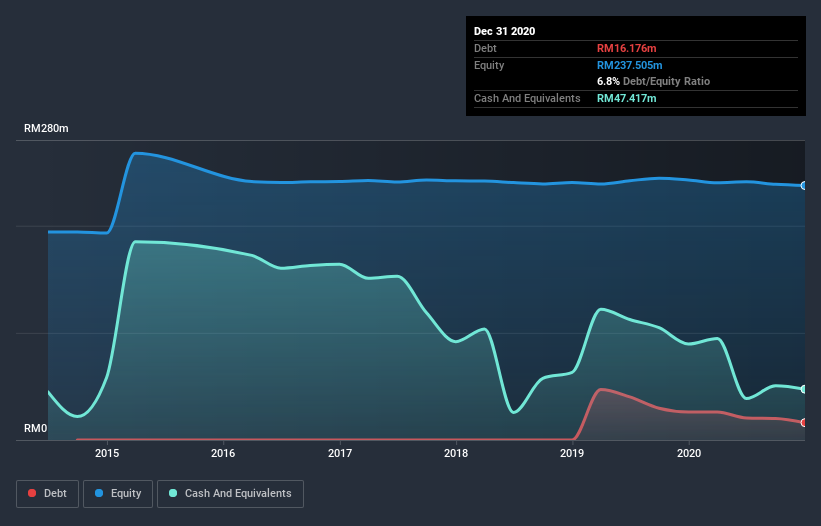

As you can see below, Paragon Globe Berhad had RM16.2m of debt at December 2020, down from RM26.1m a year prior. However, it does have RM47.4m in cash offsetting this, leading to net cash of RM31.2m.

How Strong Is Paragon Globe Berhad's Balance Sheet?

We can see from the most recent balance sheet that Paragon Globe Berhad had liabilities of RM11.1m falling due within a year, and liabilities of RM22.1m due beyond that. On the other hand, it had cash of RM47.4m and RM20.3m worth of receivables due within a year. So it actually has RM34.6m more liquid assets than total liabilities.

This surplus suggests that Paragon Globe Berhad is using debt in a way that is appears to be both safe and conservative. Because it has plenty of assets, it is unlikely to have trouble with its lenders. Simply put, the fact that Paragon Globe Berhad has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Paragon Globe Berhad will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Paragon Globe Berhad had a loss before interest and tax, and actually shrunk its revenue by 55%, to RM29m. To be frank that doesn't bode well.

So How Risky Is Paragon Globe Berhad?

While Paragon Globe Berhad lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow RM20m. So taking that on face value, and considering the net cash situation, we don't think that the stock is too risky in the near term. With mediocre revenue growth in the last year, we're don't find the investment opportunity particularly compelling. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 2 warning signs for Paragon Globe Berhad (1 shouldn't be ignored) you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade Paragon Globe Berhad, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:PGLOBE

Paragon Globe Berhad

An investment holding company, invests, develops, and trades in properties in Malaysia.

Solid track record and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor