Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Kejuruteraan Asastera Berhad (KLSE:KAB) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Kejuruteraanstera Berhad

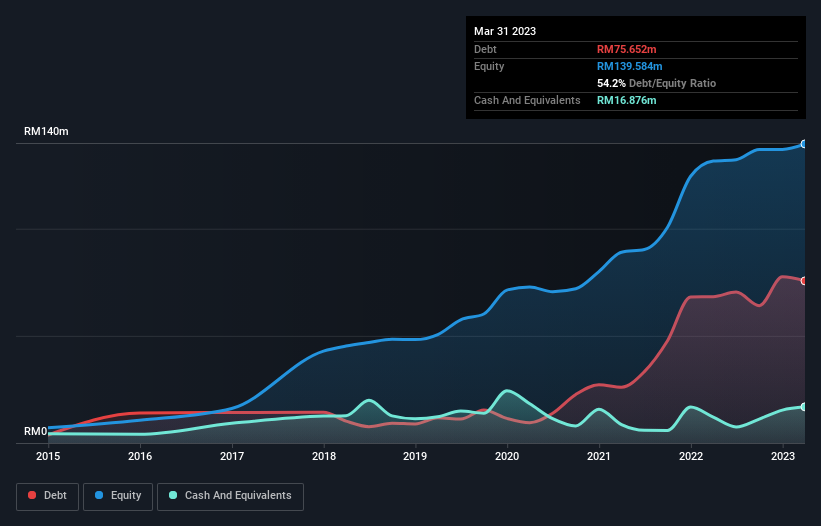

How Much Debt Does Kejuruteraanstera Berhad Carry?

The image below, which you can click on for greater detail, shows that at March 2023 Kejuruteraanstera Berhad had debt of RM75.7m, up from RM68.3m in one year. However, it also had RM16.9m in cash, and so its net debt is RM58.8m.

How Healthy Is Kejuruteraanstera Berhad's Balance Sheet?

We can see from the most recent balance sheet that Kejuruteraanstera Berhad had liabilities of RM106.0m falling due within a year, and liabilities of RM37.1m due beyond that. On the other hand, it had cash of RM16.9m and RM134.0m worth of receivables due within a year. So it actually has RM7.82m more liquid assets than total liabilities.

This state of affairs indicates that Kejuruteraanstera Berhad's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the RM641.8m company is struggling for cash, we still think it's worth monitoring its balance sheet.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While we wouldn't worry about Kejuruteraanstera Berhad's net debt to EBITDA ratio of 4.7, we think its super-low interest cover of 2.4 times is a sign of high leverage. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. Another concern for investors might be that Kejuruteraanstera Berhad's EBIT fell 13% in the last year. If that's the way things keep going handling the debt load will be like delivering hot coffees on a pogo stick. There's no doubt that we learn most about debt from the balance sheet. But it is Kejuruteraanstera Berhad's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Kejuruteraanstera Berhad saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

We'd go so far as to say Kejuruteraanstera Berhad's conversion of EBIT to free cash flow was disappointing. But at least it's pretty decent at staying on top of its total liabilities; that's encouraging. Overall, we think it's fair to say that Kejuruteraanstera Berhad has enough debt that there are some real risks around the balance sheet. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 3 warning signs with Kejuruteraanstera Berhad (at least 2 which are significant) , and understanding them should be part of your investment process.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Kinergy Advancement Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KAB

Kinergy Advancement Berhad

Provides electrical and mechanical engineering services for commercial, industrial, and residential infrastructure in Malaysia, Vietnam, Thailand, Indonesia, and Hong Kong.

High growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.1% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|3.6% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor