Advertisement

- Malaysia

- /

- Industrials

- /

- KLSE:INCKEN

Inch Kenneth Kajang Rubber (KLSE:INCKEN) Is In A Good Position To Deliver On Growth Plans

Even when a business is losing money, it's possible for shareholders to make money if they buy a good business at the right price. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

So should Inch Kenneth Kajang Rubber (KLSE:INCKEN) shareholders be worried about its cash burn? In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

See our latest analysis for Inch Kenneth Kajang Rubber

When Might Inch Kenneth Kajang Rubber Run Out Of Money?

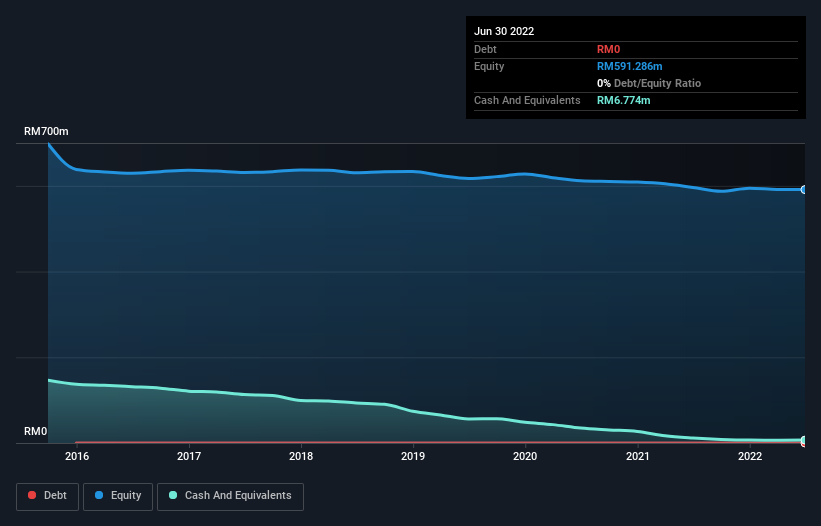

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at June 2022, Inch Kenneth Kajang Rubber had cash of RM6.8m and no debt. Looking at the last year, the company burnt through RM6.6m. Therefore, from June 2022 it had roughly 12 months of cash runway. While that cash runway isn't too concerning, sensible holders would be peering into the distance, and considering what happens if the company runs out of cash. You can see how its cash balance has changed over time in the image below.

How Well Is Inch Kenneth Kajang Rubber Growing?

Inch Kenneth Kajang Rubber managed to reduce its cash burn by 69% over the last twelve months, which suggests it's on the right flight path. This reduction was no doubt supported by its strong revenue growth of 60% in the same period. Considering these factors, we're fairly impressed by its growth trajectory. In reality, this article only makes a short study of the company's growth data. You can take a look at how Inch Kenneth Kajang Rubber is growing revenue over time by checking this visualization of past revenue growth.

How Easily Can Inch Kenneth Kajang Rubber Raise Cash?

While Inch Kenneth Kajang Rubber seems to be in a fairly good position, it's still worth considering how easily it could raise more cash, even just to fuel faster growth. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Commonly, a business will sell new shares in itself to raise cash and drive growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Inch Kenneth Kajang Rubber's cash burn of RM6.6m is about 3.5% of its RM187m market capitalisation. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

So, Should We Worry About Inch Kenneth Kajang Rubber's Cash Burn?

As you can probably tell by now, we're not too worried about Inch Kenneth Kajang Rubber's cash burn. For example, we think its revenue growth suggests that the company is on a good path. Its weak point is its cash runway, but even that wasn't too bad! Considering all the factors discussed in this article, we're not overly concerned about the company's cash burn, although we do think shareholders should keep an eye on how it develops. On another note, Inch Kenneth Kajang Rubber has 3 warning signs (and 2 which are potentially serious) we think you should know about.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:INCKEN

Inch Kenneth Kajang Rubber

An investment holding company, engages in the oil palm plantation, tourist resort, rubber, property development, and leasing of property businesses in Malaysia and Thailand.

Mediocre balance sheet low.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|35.9% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|15.6% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|23.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|2.5% overvalued

TO

Community Contributor