Advertisement

- Malaysia

- /

- Construction

- /

- KLSE:ADVCON

The Trends At Advancecon Holdings Berhad (KLSE:ADVCON) That You Should Know About

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. However, after briefly looking over the numbers, we don't think Advancecon Holdings Berhad (KLSE:ADVCON) has the makings of a multi-bagger going forward, but let's have a look at why that may be.

What is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for Advancecon Holdings Berhad:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.05 = RM13m ÷ (RM401m - RM147m) (Based on the trailing twelve months to September 2020).

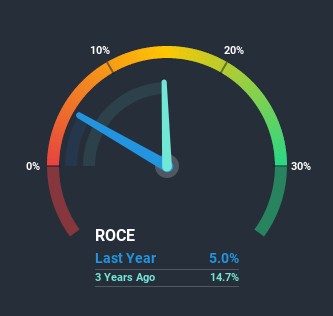

Thus, Advancecon Holdings Berhad has an ROCE of 5.0%. On its own that's a low return on capital but it's in line with the industry's average returns of 5.2%.

Check out our latest analysis for Advancecon Holdings Berhad

Above you can see how the current ROCE for Advancecon Holdings Berhad compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering Advancecon Holdings Berhad here for free.

So How Is Advancecon Holdings Berhad's ROCE Trending?

In terms of Advancecon Holdings Berhad's historical ROCE movements, the trend isn't fantastic. Around five years ago the returns on capital were 30%, but since then they've fallen to 5.0%. Given the business is employing more capital while revenue has slipped, this is a bit concerning. If this were to continue, you might be looking at a company that is trying to reinvest for growth but is actually losing market share since sales haven't increased.

On a side note, Advancecon Holdings Berhad has done well to pay down its current liabilities to 37% of total assets. So we could link some of this to the decrease in ROCE. What's more, this can reduce some aspects of risk to the business because now the company's suppliers or short-term creditors are funding less of its operations. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.In Conclusion...

In summary, we're somewhat concerned by Advancecon Holdings Berhad's diminishing returns on increasing amounts of capital. Investors haven't taken kindly to these developments, since the stock has declined 54% from where it was three years ago. Unless there is a shift to a more positive trajectory in these metrics, we would look elsewhere.

If you want to know some of the risks facing Advancecon Holdings Berhad we've found 4 warning signs (1 can't be ignored!) that you should be aware of before investing here.

While Advancecon Holdings Berhad may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

When trading Advancecon Holdings Berhad or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:ADVCON

Advancecon Holdings Berhad

Provides earthworks and civil engineering services in Malaysia.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|12.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|21.7% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.1% undervalued

EA

Community Contributor