Advertisement

Health Check: How Prudently Does Tan Chong Motor Holdings Berhad (KLSE:TCHONG) Use Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Tan Chong Motor Holdings Berhad (KLSE:TCHONG) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Tan Chong Motor Holdings Berhad

How Much Debt Does Tan Chong Motor Holdings Berhad Carry?

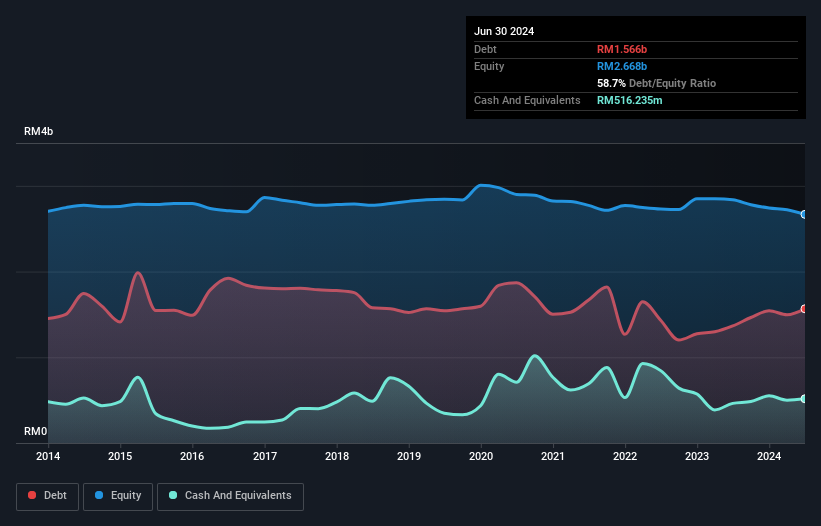

You can click the graphic below for the historical numbers, but it shows that as of June 2024 Tan Chong Motor Holdings Berhad had RM1.57b of debt, an increase on RM1.37b, over one year. However, because it has a cash reserve of RM516.2m, its net debt is less, at about RM1.05b.

How Healthy Is Tan Chong Motor Holdings Berhad's Balance Sheet?

The latest balance sheet data shows that Tan Chong Motor Holdings Berhad had liabilities of RM1.67b due within a year, and liabilities of RM705.2m falling due after that. Offsetting this, it had RM516.2m in cash and RM584.3m in receivables that were due within 12 months. So its liabilities total RM1.27b more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the RM322.6m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. At the end of the day, Tan Chong Motor Holdings Berhad would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Tan Chong Motor Holdings Berhad can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Tan Chong Motor Holdings Berhad had a loss before interest and tax, and actually shrunk its revenue by 11%, to RM2.4b. We would much prefer see growth.

Caveat Emptor

While Tan Chong Motor Holdings Berhad's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost a very considerable RM84m at the EBIT level. Combining this information with the significant liabilities we already touched on makes us very hesitant about this stock, to say the least. Of course, it may be able to improve its situation with a bit of luck and good execution. Nevertheless, we would not bet on it given that it vaporized RM159m in cash over the last twelve months, and it doesn't have much by way of liquid assets. So we consider this a high risk stock and we wouldn't be at all surprised if the company asks shareholders for money before long. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for Tan Chong Motor Holdings Berhad you should be aware of, and 1 of them makes us a bit uncomfortable.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Tan Chong Motor Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TCHONG

Tan Chong Motor Holdings Berhad

An investment holding company, engages in the assembly and distribution of passenger and commercial vehicles in Malaysia, Vietnam, and internationally.

Excellent balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|39.3% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|91.8% undervalued

DO

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.4% undervalued

AG

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|17.3% undervalued

CL

Community Contributor