Advertisement

- Malaysia

- /

- Auto Components

- /

- KLSE:ESAFE

Eversafe Rubber Berhad (KLSE:ESAFE) Is Making Moderate Use Of Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Eversafe Rubber Berhad (KLSE:ESAFE) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Our analysis indicates that ESAFE is potentially overvalued!

How Much Debt Does Eversafe Rubber Berhad Carry?

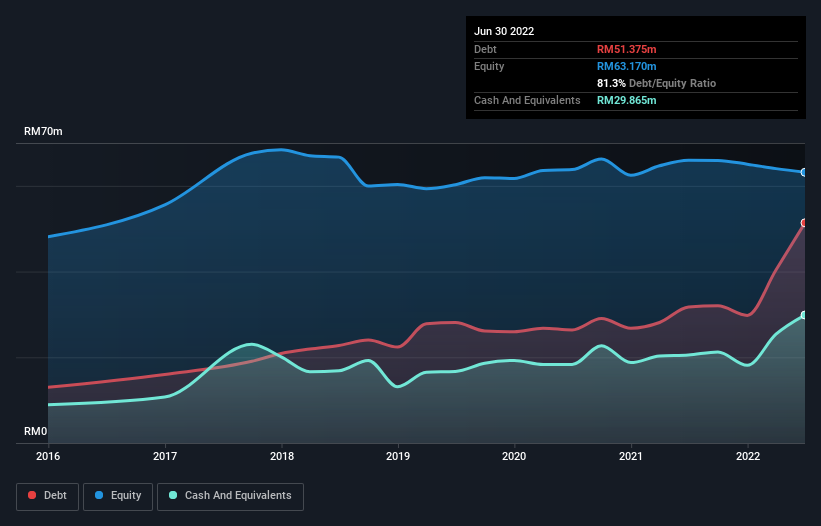

You can click the graphic below for the historical numbers, but it shows that as of June 2022 Eversafe Rubber Berhad had RM51.4m of debt, an increase on RM31.7m, over one year. However, because it has a cash reserve of RM29.9m, its net debt is less, at about RM21.5m.

A Look At Eversafe Rubber Berhad's Liabilities

Zooming in on the latest balance sheet data, we can see that Eversafe Rubber Berhad had liabilities of RM39.4m due within 12 months and liabilities of RM28.4m due beyond that. Offsetting these obligations, it had cash of RM29.9m as well as receivables valued at RM37.1m due within 12 months. So these liquid assets roughly match the total liabilities.

Having regard to Eversafe Rubber Berhad's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the RM43.3m company is struggling for cash, we still think it's worth monitoring its balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. But it is Eversafe Rubber Berhad's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Eversafe Rubber Berhad wasn't profitable at an EBIT level, but managed to grow its revenue by 13%, to RM128m. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Over the last twelve months Eversafe Rubber Berhad produced an earnings before interest and tax (EBIT) loss. To be specific the EBIT loss came in at RM1.5m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. Another cause for caution is that is bled RM3.4m in negative free cash flow over the last twelve months. So in short it's a really risky stock. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Eversafe Rubber Berhad is showing 3 warning signs in our investment analysis , and 2 of those are a bit unpleasant...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Eversafe Rubber Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:ESAFE

Eversafe Rubber Berhad

An investment holding company, develops, manufactures, distributes, and sells tyre retreading materials to tyre retreaders and rubber material traders.

Good value with slight risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$28.1829.5% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on Fiverr International ·

Fiverr International will transform the freelance industry with AI-powered growth

Fair Value:US$36.8143.1% undervalued

78 followersusers have followed this narrative

7 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

108 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

937 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

144 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative