- South Korea

- /

- Biotech

- /

- KOSDAQ:A196170

3 High Insider Ownership Growth Companies On KRX With Revenue Increases Up To 103%

Reviewed by Simply Wall St

The South Korean market has shown resilience, remaining stable over the past week and achieving a 7.2% increase over the past year, with earnings expected to grow by 30% annually. In such an environment, stocks with high insider ownership can be particularly appealing as they often indicate confidence from those who know the company best.

Top 10 Growth Companies With High Insider Ownership In South Korea

| Name | Insider Ownership | Earnings Growth |

| ALTEOGEN (KOSDAQ:A196170) | 26.6% | 73.1% |

| Seojin SystemLtd (KOSDAQ:A178320) | 29.8% | 58.7% |

| Global Tax Free (KOSDAQ:A204620) | 18.1% | 72.4% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.3% | 36.4% |

| Park Systems (KOSDAQ:A140860) | 33% | 35.6% |

| Vuno (KOSDAQ:A338220) | 19.5% | 105% |

| UTI (KOSDAQ:A179900) | 34.1% | 122.7% |

| HANA Micron (KOSDAQ:A067310) | 20% | 96.3% |

| INTEKPLUS (KOSDAQ:A064290) | 16.3% | 77.4% |

| Techwing (KOSDAQ:A089030) | 18.7% | 77.8% |

Let's explore several standout options from the results in the screener.

UTI (KOSDAQ:A179900)

Simply Wall St Growth Rating: ★★★★★★

Overview: UTI Inc., a company based in South Korea, specializes in the research, development, manufacture, and sale of smartphone camera windows and sensor glasses both domestically and internationally, with a market capitalization of approximately ₩520.53 billion.

Operations: The firm operates primarily in the production and global distribution of smartphone camera windows and sensor glasses.

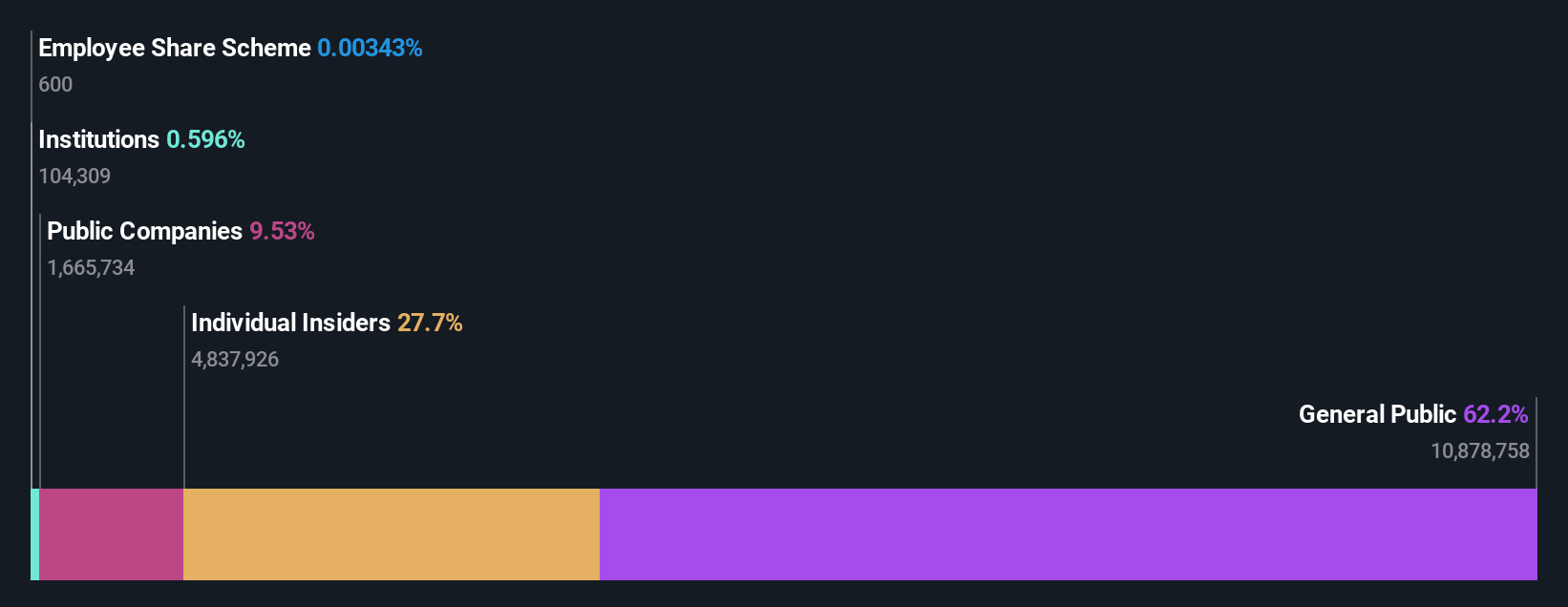

Insider Ownership: 34.1%

Revenue Growth Forecast: 103.6% p.a.

UTI Inc. in South Korea has been active in private placements, issuing significant amounts of convertible preferred stock and bonds to bolster its financial standing, with transactions closing on May 28 and July 5, 2024. These moves underscore a strategic push to secure growth capital amidst highly volatile share prices. The company's revenue is projected to grow at an impressive rate of 103.6% annually, outpacing the Korean market significantly. Moreover, UTI's return on equity is expected to be very high at 71.4% in three years, reflecting potentially efficient use of shareholder funds despite no substantial insider buying reported over the past three months.

- Get an in-depth perspective on UTI's performance by reading our analyst estimates report here.

- The valuation report we've compiled suggests that UTI's current price could be inflated.

ALTEOGEN (KOSDAQ:A196170)

Simply Wall St Growth Rating: ★★★★★★

Overview: ALTEOGEN Inc. is a biopharmaceutical company engaged in developing long-acting biobetters, proprietary antibody-drug conjugates, and antibody biosimilars, with a market capitalization of approximately ₩14.50 billion.

Operations: The company generates revenue primarily through the development of long-acting biobetters, proprietary antibody-drug conjugates, and antibody biosimilars.

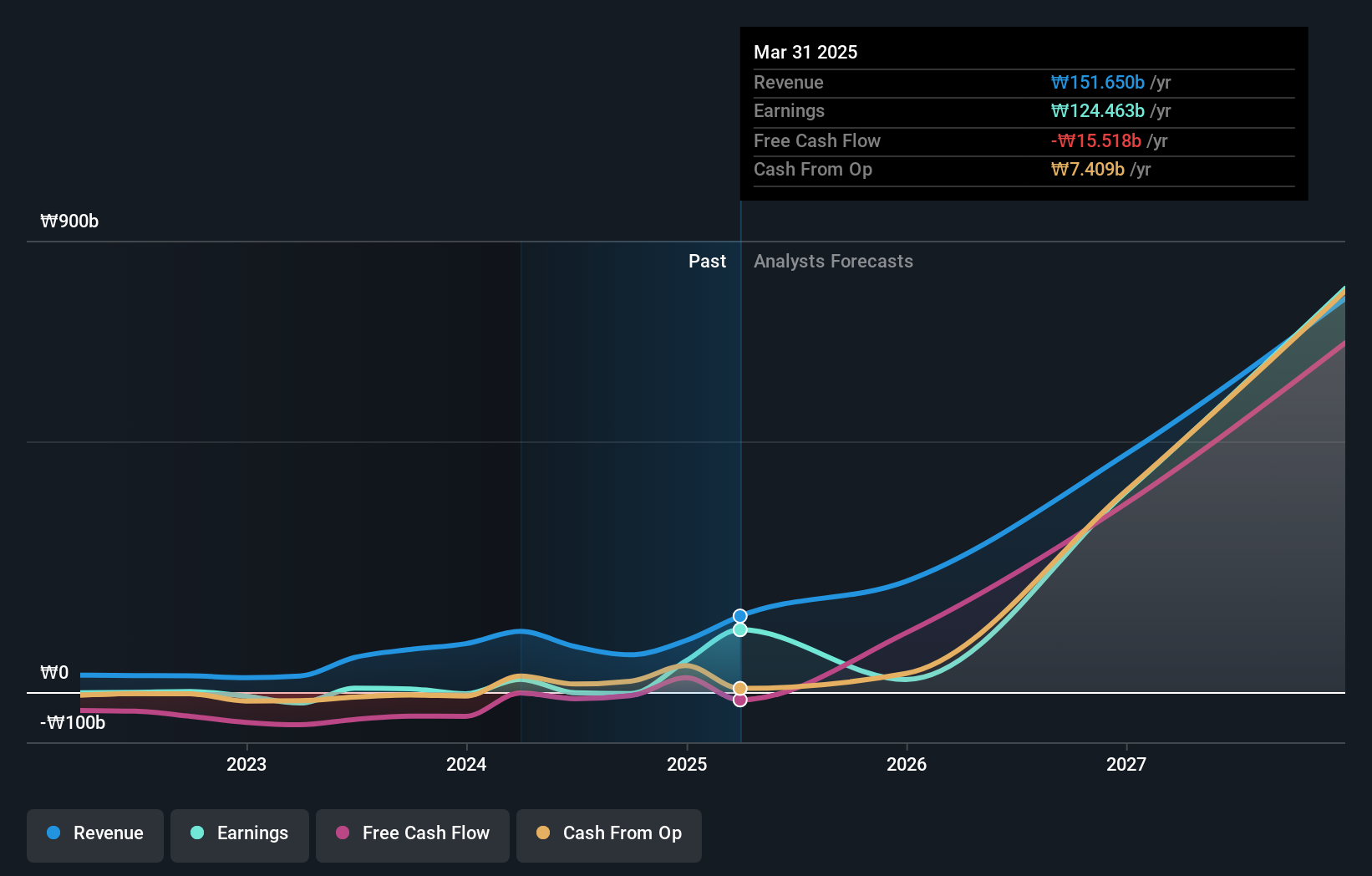

Insider Ownership: 26.6%

Revenue Growth Forecast: 48.3% p.a.

ALTEOGEN, a South Korean biotech firm, recently received approval from the Ministry of Food and Drug Safety for Tergase®, a high-purity recombinant hyaluronidase. This approval is pivotal as it marks ALTEOGEN's transition to commercial-stage operations. Despite a highly volatile share price in recent months, the company's forecasted revenue growth at 48.3% annually outstrips the national market average significantly. Additionally, earnings are expected to surge by 73.06% annually over the next three years, underpinned by robust non-cash earnings and recent profitability achievements. However, shareholder dilution has occurred over the past year, and there is no recent insider buying activity reported.

- Take a closer look at ALTEOGEN's potential here in our earnings growth report.

- Upon reviewing our latest valuation report, ALTEOGEN's share price might be too optimistic.

Vuno (KOSDAQ:A338220)

Simply Wall St Growth Rating: ★★★★★★

Overview: Vuno Inc. is a medical artificial intelligence (AI) solution development company with a market cap of approximately ₩457.62 billion.

Operations: The company generates revenue primarily from its artificial intelligence medical software production, totaling approximately ₩17.04 billion.

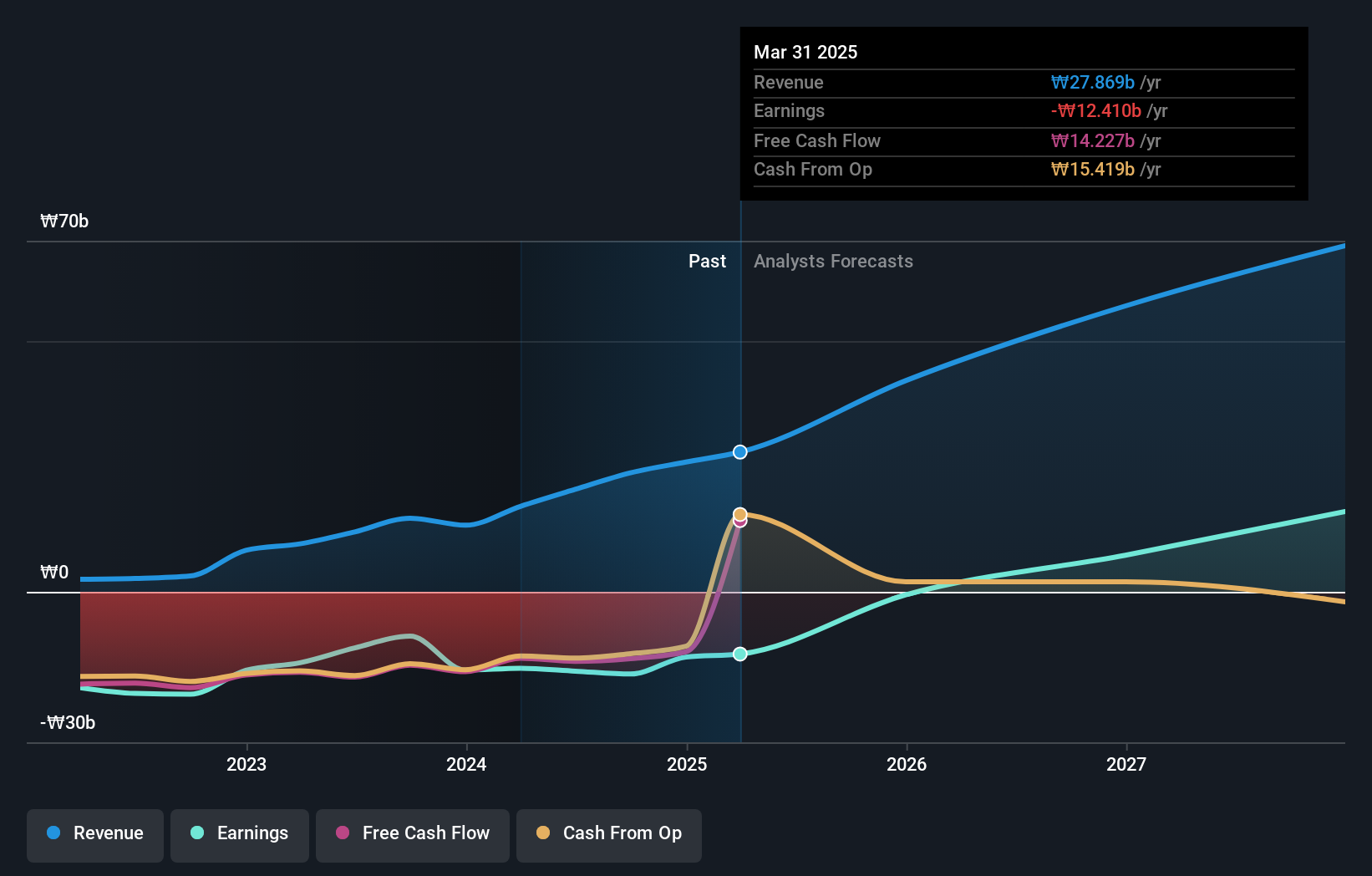

Insider Ownership: 19.5%

Revenue Growth Forecast: 41.4% p.a.

Vuno, a South Korean company, is poised for significant growth with expected revenue increases of 41.4% annually, surpassing the local market's 10.8%. It's projected to turn profitable within three years—a rate above the market average. Despite this promising outlook, challenges include a highly volatile share price and recent shareholder dilution. Additionally, its Return on Equity is anticipated to reach a very high level (117%) in three years, reflecting potentially efficient use of shareholders' equity.

- Navigate through the intricacies of Vuno with our comprehensive analyst estimates report here.

- According our valuation report, there's an indication that Vuno's share price might be on the expensive side.

Summing It All Up

- Dive into all 81 of the Fast Growing KRX Companies With High Insider Ownership we have identified here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A196170

ALTEOGEN

A bio company, focuses on developing long-acting biobetters, proprietary antibody-drug conjugates, and antibody biosimilars.

Exceptional growth potential with flawless balance sheet.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Meta’s Bold Bet on AI Pays Off

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Visa Stock: The Toll Booth at the Center of Global Commerce

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion