- South Korea

- /

- Electronic Equipment and Components

- /

- KOSDAQ:A148150

Why It Might Not Make Sense To Buy Se Gyung Hi Tech Co.,Ltd (KOSDAQ:148150) For Its Upcoming Dividend

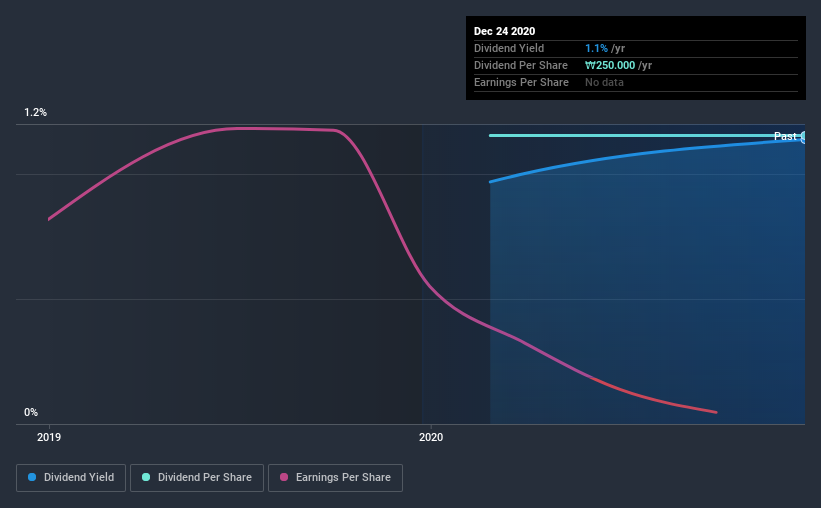

It looks like Se Gyung Hi Tech Co.,Ltd (KOSDAQ:148150) is about to go ex-dividend in the next three days. Investors can purchase shares before the 29th of December in order to be eligible for this dividend, which will be paid on the 10th of April.

Se Gyung Hi TechLtd's next dividend payment will be ₩250 per share. Last year, in total, the company distributed ₩250 to shareholders. Calculating the last year's worth of payments shows that Se Gyung Hi TechLtd has a trailing yield of 1.1% on the current share price of ₩21950. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! As a result, readers should always check whether Se Gyung Hi TechLtd has been able to grow its dividends, or if the dividend might be cut.

See our latest analysis for Se Gyung Hi TechLtd

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Se Gyung Hi TechLtd reported a loss last year, so it's not great to see that it has continued paying a dividend. Given that the company reported a loss last year, we now need to see if it generated enough free cash flow to fund the dividend. If Se Gyung Hi TechLtd didn't generate enough cash to pay the dividend, then it must have either paid from cash in the bank or by borrowing money, neither of which is sustainable in the long term. Se Gyung Hi TechLtd paid a dividend despite reporting negative free cash flow last year. That's typically a bad combination and - if this were more than a one-off - not sustainable.

Click here to see how much of its profit Se Gyung Hi TechLtd paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Se Gyung Hi TechLtd was unprofitable last year, and sadly its loss per share worsened by 114% on the previous year.

Given that Se Gyung Hi TechLtd has only been paying a dividend for a year, there's not much of a past history to draw insight from.

Remember, you can always get a snapshot of Se Gyung Hi TechLtd's financial health, by checking our visualisation of its financial health, here.

Final Takeaway

Is Se Gyung Hi TechLtd an attractive dividend stock, or better left on the shelf? First, it's not great to see the company paying a dividend despite being loss-making over the last year. Second, the dividend was not well covered by cash flow." It's not that we think Se Gyung Hi TechLtd is a bad company, but these characteristics don't generally lead to outstanding dividend performance.

Having said that, if you're looking at this stock without much concern for the dividend, you should still be familiar of the risks involved with Se Gyung Hi TechLtd. For example, we've found 3 warning signs for Se Gyung Hi TechLtd (1 is a bit concerning!) that deserve your attention before investing in the shares.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade Se Gyung Hi TechLtd, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A148150

Se Gyung Hi Tech

Engages in the manufacture and sale of electronic equipment parts.

Flawless balance sheet and undervalued.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion