Advertisement

- South Korea

- /

- Communications

- /

- KOSDAQ:A051390

Yw (KOSDAQ:051390) Strong Profits May Be Masking Some Underlying Issues

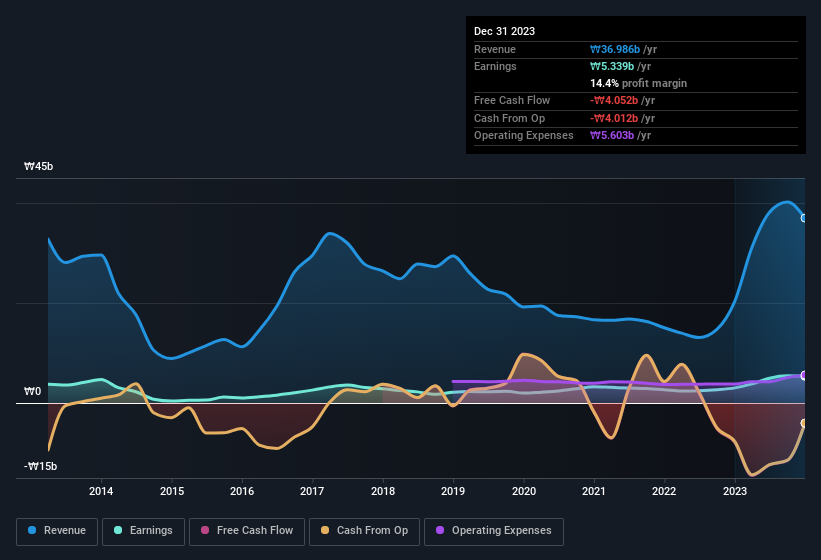

The recent earnings posted by Yw Company Limited (KOSDAQ:051390) were solid, but the stock didn't move as much as we expected. We believe that shareholders have noticed some concerning factors beyond the statutory profit numbers.

See our latest analysis for Yw

The Impact Of Unusual Items On Profit

For anyone who wants to understand Yw's profit beyond the statutory numbers, it's important to note that during the last twelve months statutory profit gained from ₩880m worth of unusual items. We can't deny that higher profits generally leave us optimistic, but we'd prefer it if the profit were to be sustainable. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. If Yw doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Yw.

Our Take On Yw's Profit Performance

Arguably, Yw's statutory earnings have been distorted by unusual items boosting profit. Therefore, it seems possible to us that Yw's true underlying earnings power is actually less than its statutory profit. But at least holders can take some solace from the 66% per annum growth in EPS for the last three. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. So while earnings quality is important, it's equally important to consider the risks facing Yw at this point in time. Every company has risks, and we've spotted 2 warning signs for Yw you should know about.

Today we've zoomed in on a single data point to better understand the nature of Yw's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A051390

Yw

Develops, supplies, and installs wired and wireless communication equipment in Japan, China, and Indonesia.

Flawless balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor