Advertisement

- South Korea

- /

- Software

- /

- KOSDAQ:A288980

Would Moadata (KOSDAQ:288980) Be Better Off With Less Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Moadata Co., Ltd. (KOSDAQ:288980) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Moadata

What Is Moadata's Net Debt?

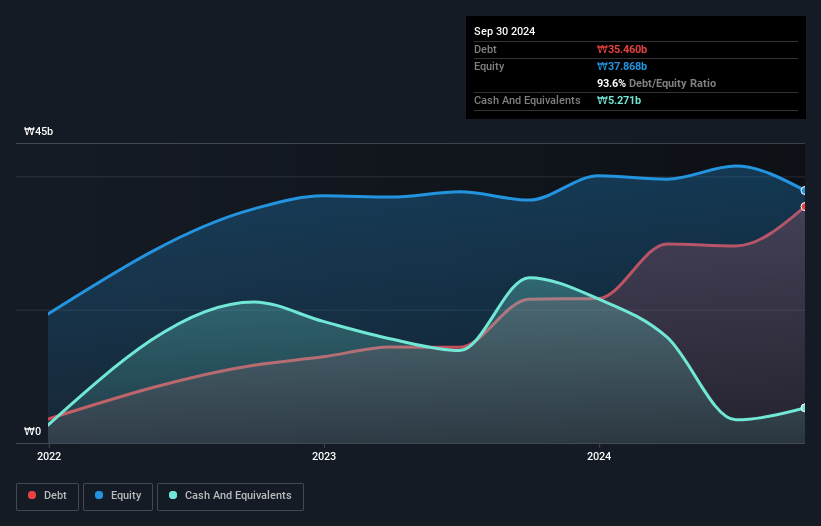

The image below, which you can click on for greater detail, shows that at September 2024 Moadata had debt of ₩35.5b, up from ₩21.6b in one year. However, because it has a cash reserve of ₩5.27b, its net debt is less, at about ₩30.2b.

How Strong Is Moadata's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Moadata had liabilities of ₩47.3b due within 12 months and liabilities of ₩1.15b due beyond that. Offsetting these obligations, it had cash of ₩5.27b as well as receivables valued at ₩8.54b due within 12 months. So it has liabilities totalling ₩34.7b more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of ₩54.6b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Moadata will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Moadata wasn't profitable at an EBIT level, but managed to grow its revenue by 13%, to ₩26b. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Over the last twelve months Moadata produced an earnings before interest and tax (EBIT) loss. Indeed, it lost ₩774m at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. Another cause for caution is that is bled ₩7.9b in negative free cash flow over the last twelve months. So suffice it to say we consider the stock very risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Moadata (1 makes us a bit uncomfortable!) that you should be aware of before investing here.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A288980

Moadata

An artificial intelligence company, provides ICT infrastructure monitoring and healthcare solutions in South Korea.

Mediocre balance sheet with low risk.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2540.0% undervalued

89 followersusers have followed this narrative

0 commentsusers have commented on this narrative

22 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$482.3% overvalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.7% undervalued

57 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$825.3% undervalued

29 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

KE

Kentaiga on Microsoft ·

Microsoft Are Industry Leaders at a Heavy Discount

Fair Value:US$50021.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.529.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on Medibank Private ·

Medibank Private Limited. No Margin of Safety!

Fair Value:AU$3.830.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.1% undervalued

83 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.3% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0544.6% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Trending Discussion

MW

mwod31 on Greatland Resources ·

A great comment, WSB have not done the research imo. I intend to buy more shares in 2026.

0

|0