Stock Analysis

- South Korea

- /

- Semiconductors

- /

- KOSE:A281820

KCTech Co., Ltd.'s (KRX:281820) Stock On An Uptrend: Could Fundamentals Be Driving The Momentum?

KCTech's (KRX:281820) stock is up by a considerable 26% over the past month. As most would know, fundamentals are what usually guide market price movements over the long-term, so we decided to look at the company's key financial indicators today to determine if they have any role to play in the recent price movement. Specifically, we decided to study KCTech's ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

See our latest analysis for KCTech

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for KCTech is:

8.7% = ₩40b ÷ ₩461b (Based on the trailing twelve months to March 2024).

The 'return' is the profit over the last twelve months. That means that for every ₩1 worth of shareholders' equity, the company generated ₩0.09 in profit.

Why Is ROE Important For Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

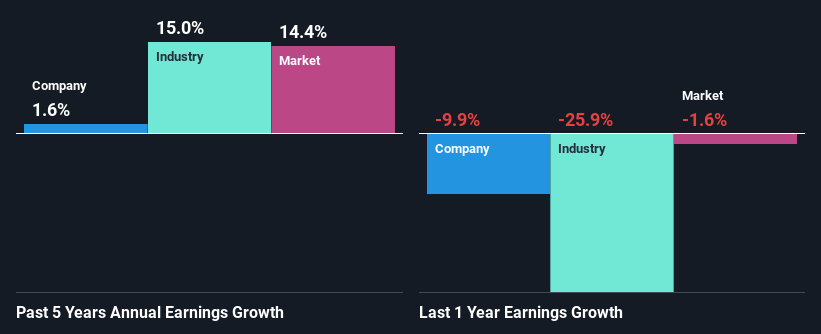

A Side By Side comparison of KCTech's Earnings Growth And 8.7% ROE

On the face of it, KCTech's ROE is not much to talk about. Although a closer study shows that the company's ROE is higher than the industry average of 7.3% which we definitely can't overlook. However, KCTech has seen a flattish net income growth over the past five years, which is not saying much. Bear in mind, the company does have a slightly low ROE. It is just that the industry ROE is lower. So that could be one of the factors that are causing earnings growth to stay flat.

We then compared KCTech's net income growth with the industry and found that the company's growth figure is lower than the average industry growth rate of 15% in the same 5-year period, which is a bit concerning.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. If you're wondering about KCTech's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is KCTech Using Its Retained Earnings Effectively?

KCTech doesn't pay any regular dividends, meaning that potentially all of its profits are being reinvested in the business. However, this doesn't explain why the company hasn't seen any growth. So there could be some other explanations in that regard. For instance, the company's business may be deteriorating.

Conclusion

Overall, we feel that KCTech certainly does have some positive factors to consider. Although, we are disappointed to see a lack of growth in earnings even in spite of a moderate ROE and and a high reinvestment rate. We believe that there might be some outside factors that could be having a negative impact on the business. Having said that, looking at the current analyst estimates, we found that the company's earnings are expected to gain momentum. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

Valuation is complex, but we're helping make it simple.

Find out whether KCTech is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A281820

KCTech

Engages in the manufacture and distribution of semiconductor systems, display systems, and electronic materials in South Korea.

Flawless balance sheet with moderate growth potential.