Advertisement

- South Korea

- /

- Semiconductors

- /

- KOSDAQ:A082850

Does Wooree BioLtd (KOSDAQ:082850) Have A Healthy Balance Sheet?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Wooree Bio Co.,Ltd (KOSDAQ:082850) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Wooree BioLtd

How Much Debt Does Wooree BioLtd Carry?

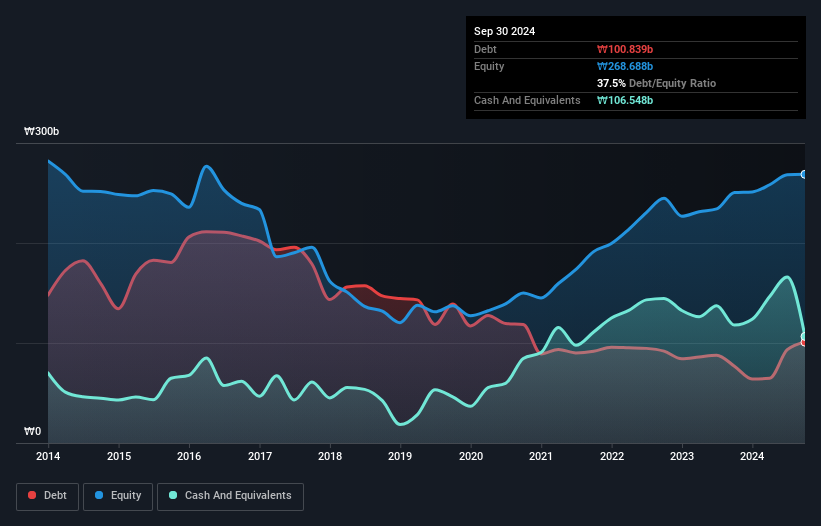

You can click the graphic below for the historical numbers, but it shows that as of September 2024 Wooree BioLtd had ₩100.8b of debt, an increase on ₩76.8b, over one year. However, it does have ₩106.5b in cash offsetting this, leading to net cash of ₩5.71b.

How Strong Is Wooree BioLtd's Balance Sheet?

The latest balance sheet data shows that Wooree BioLtd had liabilities of ₩322.5b due within a year, and liabilities of ₩54.8b falling due after that. Offsetting this, it had ₩106.5b in cash and ₩219.7b in receivables that were due within 12 months. So its liabilities total ₩51.1b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Wooree BioLtd has a market capitalization of ₩133.6b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt. While it does have liabilities worth noting, Wooree BioLtd also has more cash than debt, so we're pretty confident it can manage its debt safely.

Also good is that Wooree BioLtd grew its EBIT at 17% over the last year, further increasing its ability to manage debt. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Wooree BioLtd will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Wooree BioLtd has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Wooree BioLtd created free cash flow amounting to 13% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Summing Up

While Wooree BioLtd does have more liabilities than liquid assets, it also has net cash of ₩5.71b. And it impressed us with its EBIT growth of 17% over the last year. So we don't have any problem with Wooree BioLtd's use of debt. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for Wooree BioLtd you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Wooree BioLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A082850

Wooree BioLtd

Engages in the production and sale of flexible circuit boards in South Korea.

Good value with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor