Advertisement

- South Korea

- /

- Retail Distributors

- /

- KOSDAQ:A039980

Polaris AI (KOSDAQ:039980) Seems To Use Debt Rather Sparingly

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Polaris AI Corp. (KOSDAQ:039980) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Polaris AI

How Much Debt Does Polaris AI Carry?

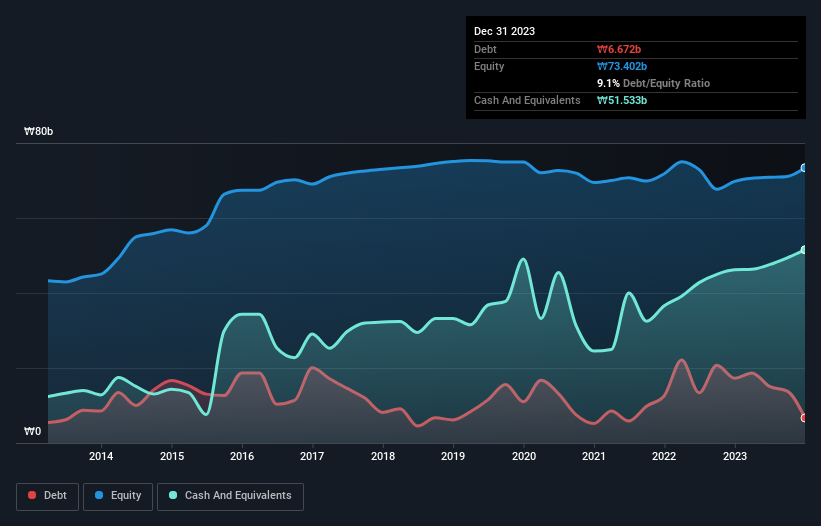

You can click the graphic below for the historical numbers, but it shows that Polaris AI had ₩6.67b of debt in December 2023, down from ₩17.3b, one year before. However, its balance sheet shows it holds ₩51.5b in cash, so it actually has ₩44.9b net cash.

A Look At Polaris AI's Liabilities

We can see from the most recent balance sheet that Polaris AI had liabilities of ₩18.9b falling due within a year, and liabilities of ₩3.21b due beyond that. On the other hand, it had cash of ₩51.5b and ₩3.89b worth of receivables due within a year. So it can boast ₩33.3b more liquid assets than total liabilities.

It's good to see that Polaris AI has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Due to its strong net asset position, it is not likely to face issues with its lenders. Simply put, the fact that Polaris AI has more cash than debt is arguably a good indication that it can manage its debt safely.

Although Polaris AI made a loss at the EBIT level, last year, it was also good to see that it generated ₩1.5b in EBIT over the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But it is Polaris AI's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Polaris AI may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, Polaris AI actually produced more free cash flow than EBIT over the last year. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that Polaris AI has net cash of ₩44.9b, as well as more liquid assets than liabilities. The cherry on top was that in converted 923% of that EBIT to free cash flow, bringing in ₩13b. So we don't think Polaris AI's use of debt is risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Polaris AI has 5 warning signs (and 2 which don't sit too well with us) we think you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A039980

Polaris AI

Operates in the fashion and information technology (IT) businesses in South Korea and internationally.

Excellent balance sheet with very low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor