Advertisement

- South Korea

- /

- Entertainment

- /

- KOSDAQ:A035760

There Are Reasons To Feel Uneasy About CJ ENM's (KOSDAQ:035760) Returns On Capital

There are a few key trends to look for if we want to identify the next multi-bagger. Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. However, after investigating CJ ENM (KOSDAQ:035760), we don't think it's current trends fit the mold of a multi-bagger.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for CJ ENM, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

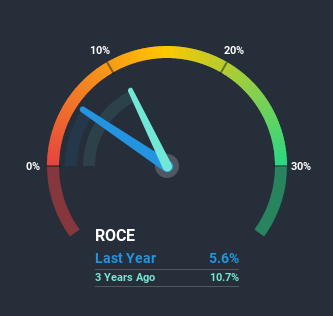

0.056 = ₩267b ÷ (₩6.3t - ₩1.6t) (Based on the trailing twelve months to December 2020).

So, CJ ENM has an ROCE of 5.6%. Even though it's in line with the industry average of 5.9%, it's still a low return by itself.

Check out our latest analysis for CJ ENM

In the above chart we have measured CJ ENM's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for CJ ENM.

What Can We Tell From CJ ENM's ROCE Trend?

Unfortunately, the trend isn't great with ROCE falling from 10% five years ago, while capital employed has grown 136%. That being said, CJ ENM raised some capital prior to their latest results being released, so that could partly explain the increase in capital employed. CJ ENM probably hasn't received a full year of earnings yet from the new funds it raised, so these figures should be taken with a grain of salt. It's also worth noting the company's latest EBIT figure is within 10% of the previous year, so it's fair to assign the ROCE drop largely to the capital raise.

Our Take On CJ ENM's ROCE

In summary, we're somewhat concerned by CJ ENM's diminishing returns on increasing amounts of capital. It should come as no surprise then that the stock has fallen 24% over the last five years, so it looks like investors are recognizing these changes. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

If you'd like to know about the risks facing CJ ENM, we've discovered 3 warning signs that you should be aware of.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

If you’re looking to trade CJ ENM, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A035760

CJ ENM

Engages in media platform, film/drama, music, and commerce businesses in South Korea.

Fair value with questionable track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor