Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies NGeneBio Co., Ltd. (KOSDAQ:354200) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for NGeneBio

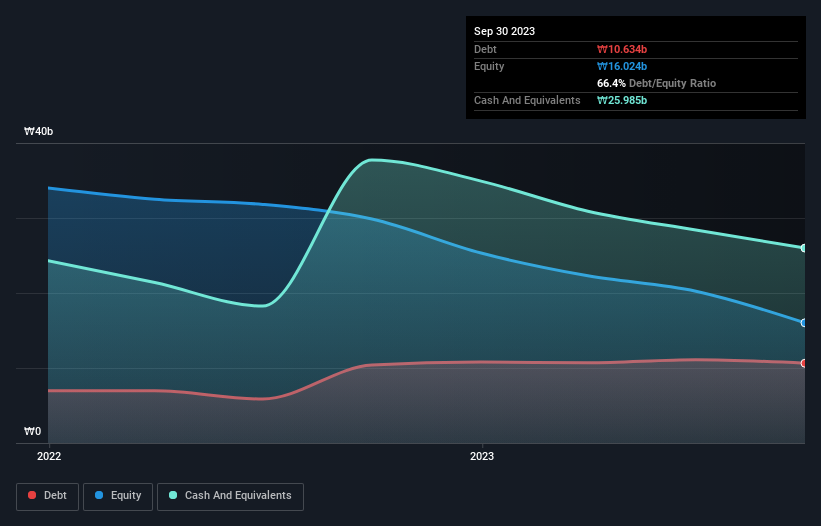

How Much Debt Does NGeneBio Carry?

As you can see below, NGeneBio had ₩10.6b of debt, at September 2023, which is about the same as the year before. You can click the chart for greater detail. But on the other hand it also has ₩26.0b in cash, leading to a ₩15.4b net cash position.

A Look At NGeneBio's Liabilities

We can see from the most recent balance sheet that NGeneBio had liabilities of ₩28.7b falling due within a year, and liabilities of ₩2.06b due beyond that. Offsetting these obligations, it had cash of ₩26.0b as well as receivables valued at ₩981.7m due within 12 months. So its liabilities total ₩3.83b more than the combination of its cash and short-term receivables.

Of course, NGeneBio has a market capitalization of ₩60.7b, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. Despite its noteworthy liabilities, NGeneBio boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since NGeneBio will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, NGeneBio made a loss at the EBIT level, and saw its revenue drop to ₩4.5b, which is a fall of 64%. To be frank that doesn't bode well.

So How Risky Is NGeneBio?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year NGeneBio had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through ₩10b of cash and made a loss of ₩17b. But at least it has ₩15.4b on the balance sheet to spend on growth, near-term. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. We've identified 4 warning signs with NGeneBio (at least 1 which makes us a bit uncomfortable) , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if NGeneBio might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A354200

NGeneBio

Develops in vitro diagnostics companion diagnostics products and bioinformatics software.

Excellent balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor