- South Korea

- /

- Airlines

- /

- KOSE:A091810

ST PharmLtd And 2 More Value Stocks On The KRX For Potential Growth

Reviewed by Simply Wall St

The South Korean market has climbed 2.3% in the last 7 days and is up 5.0% over the last 12 months, with earnings expected to grow by 29% per annum over the next few years. In this promising environment, identifying undervalued stocks like ST Pharm Ltd can offer potential growth opportunities for investors seeking value in their portfolios.

Top 10 Undervalued Stocks Based On Cash Flows In South Korea

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Samwha ElectricLtd (KOSE:A009470) | ₩49200.00 | ₩92743.12 | 47% |

| APR (KOSE:A278470) | ₩266500.00 | ₩520638.47 | 48.8% |

| VIOL (KOSDAQ:A335890) | ₩8900.00 | ₩17740.97 | 49.8% |

| T'Way Air (KOSE:A091810) | ₩3070.00 | ₩5668.20 | 45.8% |

| SK Biopharmaceuticals (KOSE:A326030) | ₩104000.00 | ₩179969.09 | 42.2% |

| Lutronic (KOSDAQ:A085370) | ₩36700.00 | ₩63217.94 | 41.9% |

| ABCO Electronics (KOSDAQ:A036010) | ₩5810.00 | ₩11478.19 | 49.4% |

| Oscotec (KOSDAQ:A039200) | ₩34700.00 | ₩65156.22 | 46.7% |

| Shinsung E&GLtd (KOSE:A011930) | ₩1691.00 | ₩3000.80 | 43.6% |

| Hotel ShillaLtd (KOSE:A008770) | ₩47800.00 | ₩82629.19 | 42.2% |

Underneath we present a selection of stocks filtered out by our screen.

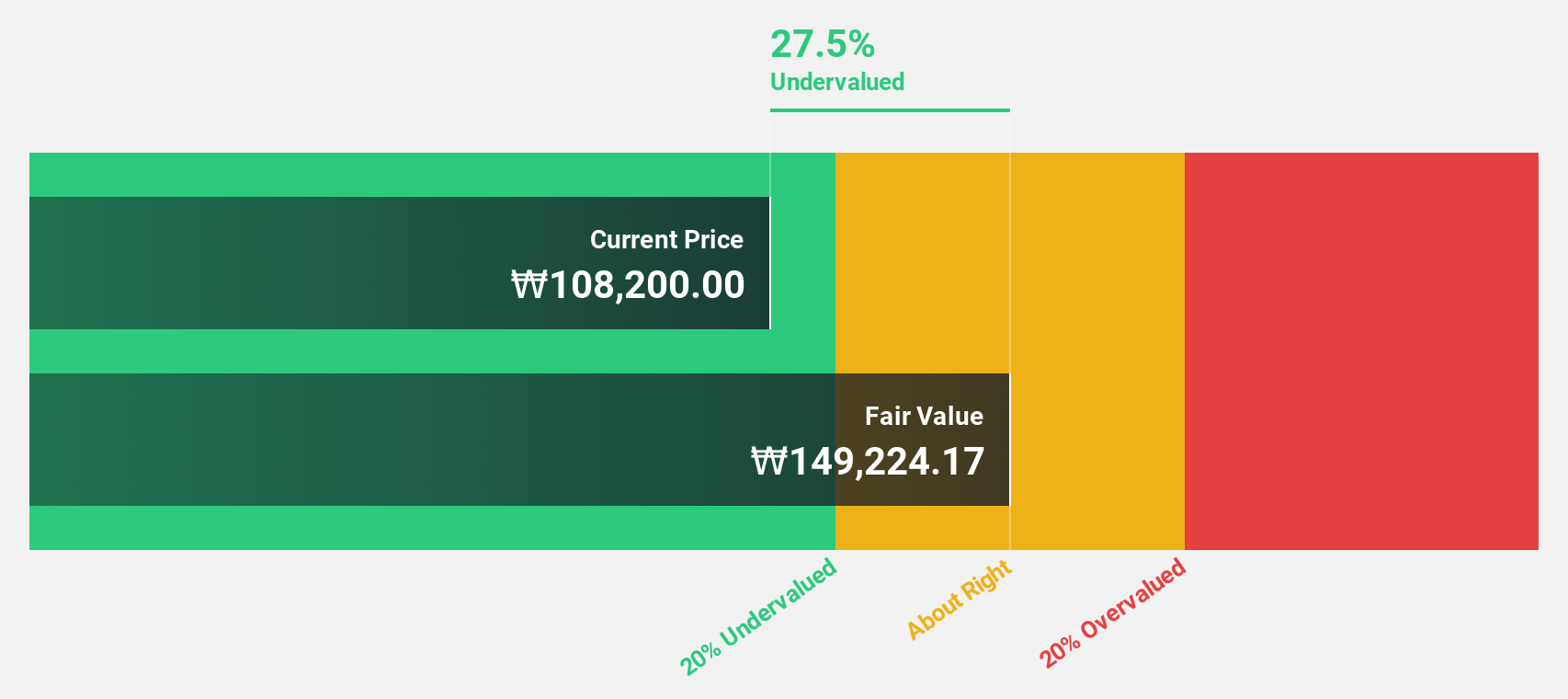

ST PharmLtd (KOSDAQ:A237690)

Overview: ST Pharm Co., Ltd. provides custom manufacturing services for active pharmaceutical ingredients and intermediates in South Korea and internationally, with a market cap of ₩2.02 trillion.

Operations: ST Pharm Ltd. generates revenue primarily from raw material manufacturing (₩236.78 billion) and clinical trial site consignment research institute services (₩36.38 billion).

Estimated Discount To Fair Value: 32.6%

ST Pharm Ltd. is trading at ₩100,700, which is 32.6% below its estimated fair value of ₩149,324.42. Despite recent high volatility and past shareholder dilution, the company shows strong earnings growth potential at 37.36% per year, outpacing the South Korean market's 29.3%. However, large one-off items have impacted financial results recently and its Return on Equity forecast remains low at 13.1%.

- Our growth report here indicates ST PharmLtd may be poised for an improving outlook.

- Get an in-depth perspective on ST PharmLtd's balance sheet by reading our health report here.

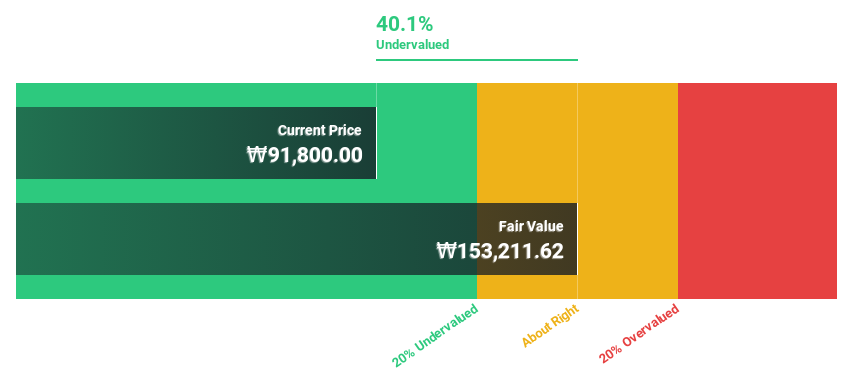

Cosmecca Korea (KOSDAQ:A241710)

Overview: Cosmecca Korea Co., Ltd. engages in the research, development, manufacture, and sale of skincare products both domestically and internationally, with a market cap of ₩980.42 billion.

Operations: Cosmecca Korea's revenue primarily comes from its cosmetics segment, which generated ₩558.96 billion, and technology fees amounting to ₩3.17 billion.

Estimated Discount To Fair Value: 40.1%

Cosmecca Korea, trading at ₩91,800, is significantly undervalued with an estimated fair value of ₩153,211.62. The company's earnings are forecast to grow 21.57% annually over the next three years but slower than the market's 29.3%. Revenue growth is expected at 14.8% per year, outpacing the market average of 10.5%. Despite these positive indicators, investors should consider that past earnings surged by a very large amount due to exceptional items.

- According our earnings growth report, there's an indication that Cosmecca Korea might be ready to expand.

- Unlock comprehensive insights into our analysis of Cosmecca Korea stock in this financial health report.

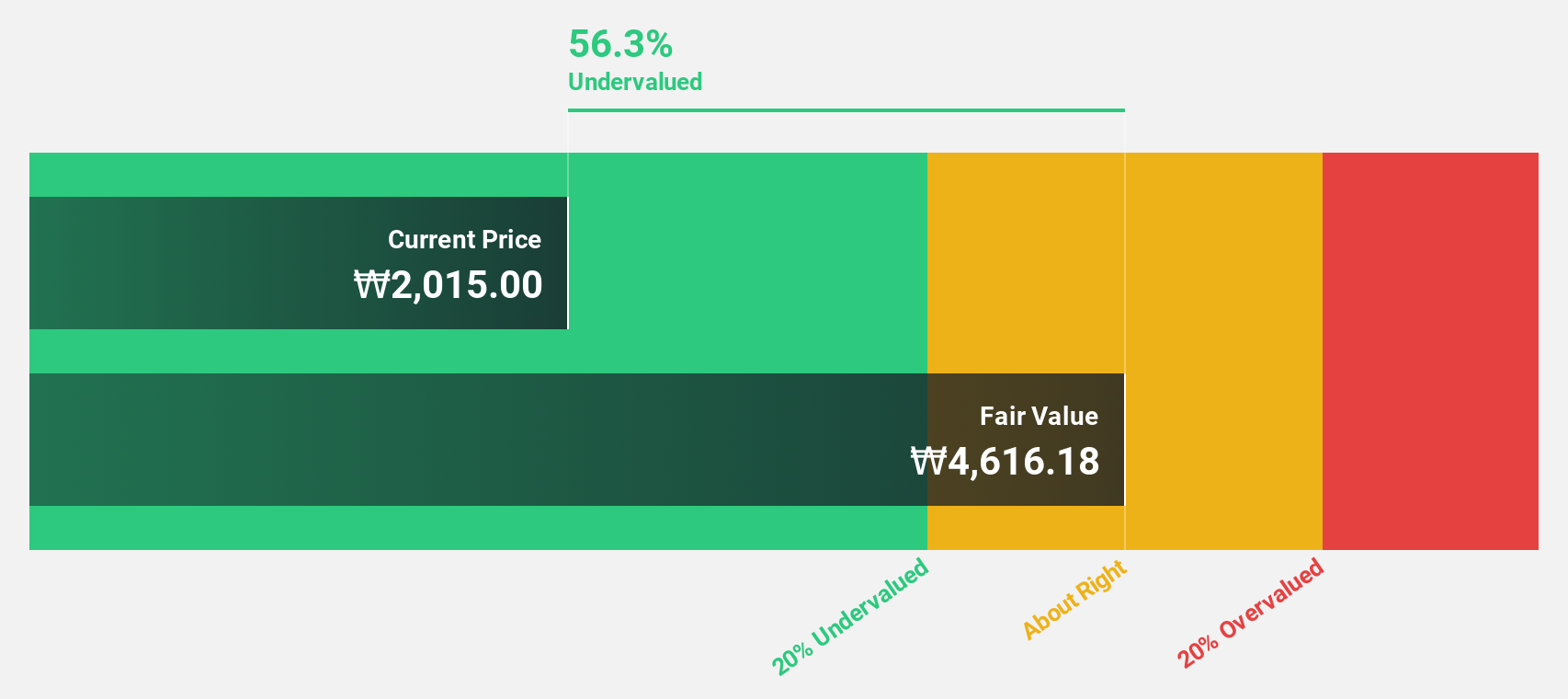

T'Way Air (KOSE:A091810)

Overview: T'Way Air Co., Ltd. provides air transportation services both domestically in South Korea and internationally, with a market cap of approximately ₩660.58 billion.

Operations: The company's primary revenue segment is its aviation business, which generated approximately ₩1.45 billion.

Estimated Discount To Fair Value: 45.8%

T'Way Air, currently trading at ₩3070, is significantly undervalued with an estimated fair value of ₩5668.2. The company's earnings are projected to grow 23.39% annually over the next three years, though slower than the market's 29.3%. Recent M&A activity includes Daemyung Sonoseason acquiring a 10% stake for ₩70.86 billion and Sono International acquiring a 14.90% stake for approximately ₩110 billion, indicating strategic interest in T'Way's potential despite past shareholder dilution.

- Our comprehensive growth report raises the possibility that T'Way Air is poised for substantial financial growth.

- Take a closer look at T'Way Air's balance sheet health here in our report.

Make It Happen

- Navigate through the entire inventory of 35 Undervalued KRX Stocks Based On Cash Flows here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if T'Way Air might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A091810

T'Way Air

Provides air transportation services in South Korea and internationally.

Outstanding track record and good value.