- South Korea

- /

- Entertainment

- /

- KOSE:A352820

KRX Value Stocks Estimated To Be Below Intrinsic Worth For September 2024

Reviewed by Simply Wall St

The South Korea stock market has experienced a recent downturn, with the KOSPI index resting just above the 2,660-point mark after a series of mixed performances across various sectors. As investors navigate these fluctuating conditions, identifying undervalued stocks that are estimated to be below their intrinsic worth can present compelling opportunities for long-term growth and stability.

Top 10 Undervalued Stocks Based On Cash Flows In South Korea

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| APR (KOSE:A278470) | ₩257000.00 | ₩510973.20 | 49.7% |

| T'Way Air (KOSE:A091810) | ₩2940.00 | ₩5767.81 | 49% |

| Cosmecca Korea (KOSDAQ:A241710) | ₩78300.00 | ₩143617.44 | 45.5% |

| Genohco (KOSDAQ:A361390) | ₩13850.00 | ₩26160.95 | 47.1% |

| Global Tax Free (KOSDAQ:A204620) | ₩3605.00 | ₩6780.99 | 46.8% |

| ABCO Electronics (KOSDAQ:A036010) | ₩5780.00 | ₩11447.73 | 49.5% |

| Shinsung E&GLtd (KOSE:A011930) | ₩1676.00 | ₩2986.13 | 43.9% |

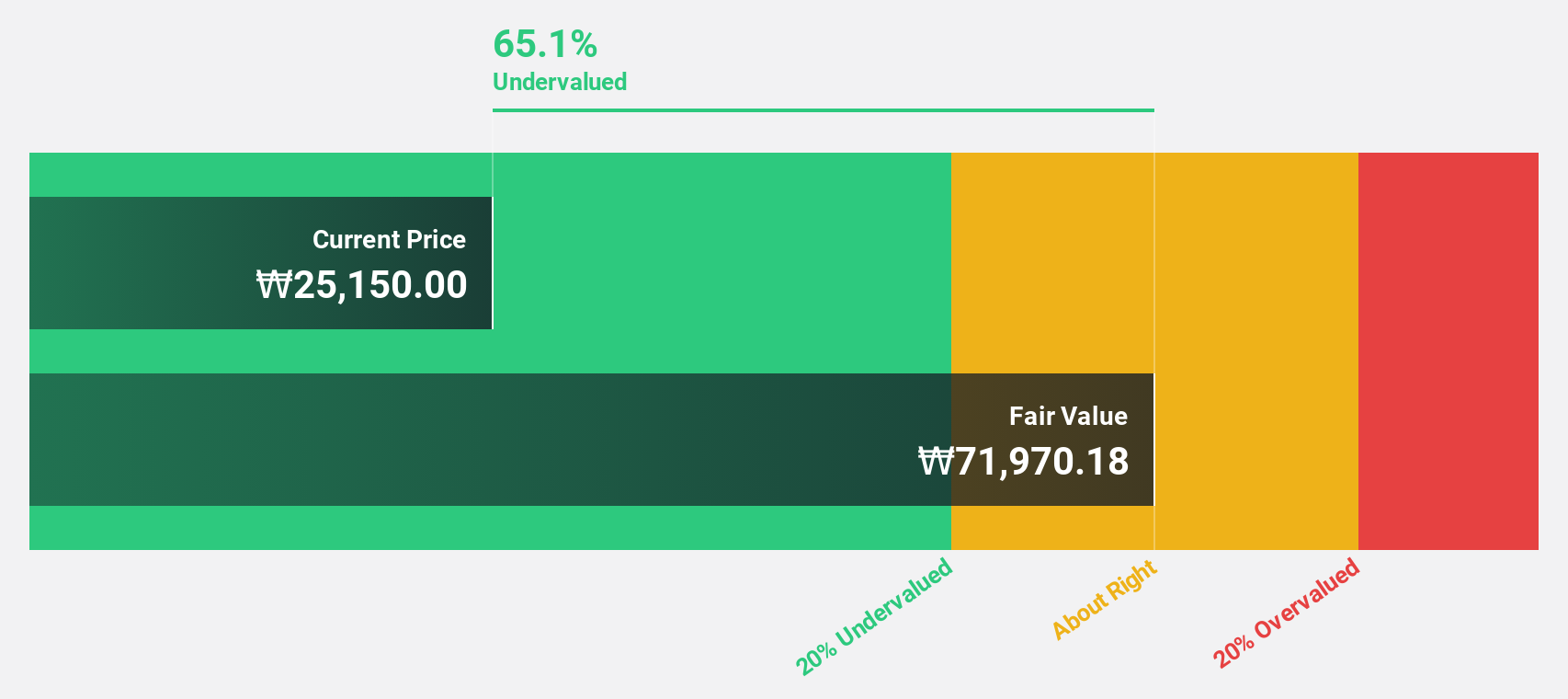

| Hanall Biopharma (KOSE:A009420) | ₩40050.00 | ₩70271.91 | 43% |

| Raonsecure (KOSDAQ:A042510) | ₩2390.00 | ₩4409.63 | 45.8% |

| Hotel ShillaLtd (KOSE:A008770) | ₩47450.00 | ₩83235.67 | 43% |

Underneath we present a selection of stocks filtered out by our screen.

Hanall Biopharma (KOSE:A009420)

Overview: Hanall Biopharma Co., Ltd. is a pharmaceutical company that manufactures and sells pharmaceutical products both in South Korea and internationally, with a market cap of ₩2.03 billion.

Operations: Revenue from the manufacture and sale of pharmaceuticals is ₩130.37 billion.

Estimated Discount To Fair Value: 43%

Hanall Biopharma is trading 43% below its estimated fair value of ₩70,271.91, indicating it is highly undervalued based on discounted cash flows. Despite recent earnings showing a significant net loss of ₩3.65 billion for the first half of 2024 compared to a net income of ₩6.05 billion a year ago, analysts forecast revenue growth at 16.4% per year and expect profitability within three years, outpacing average market growth in South Korea.

- Insights from our recent growth report point to a promising forecast for Hanall Biopharma's business outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Hanall Biopharma.

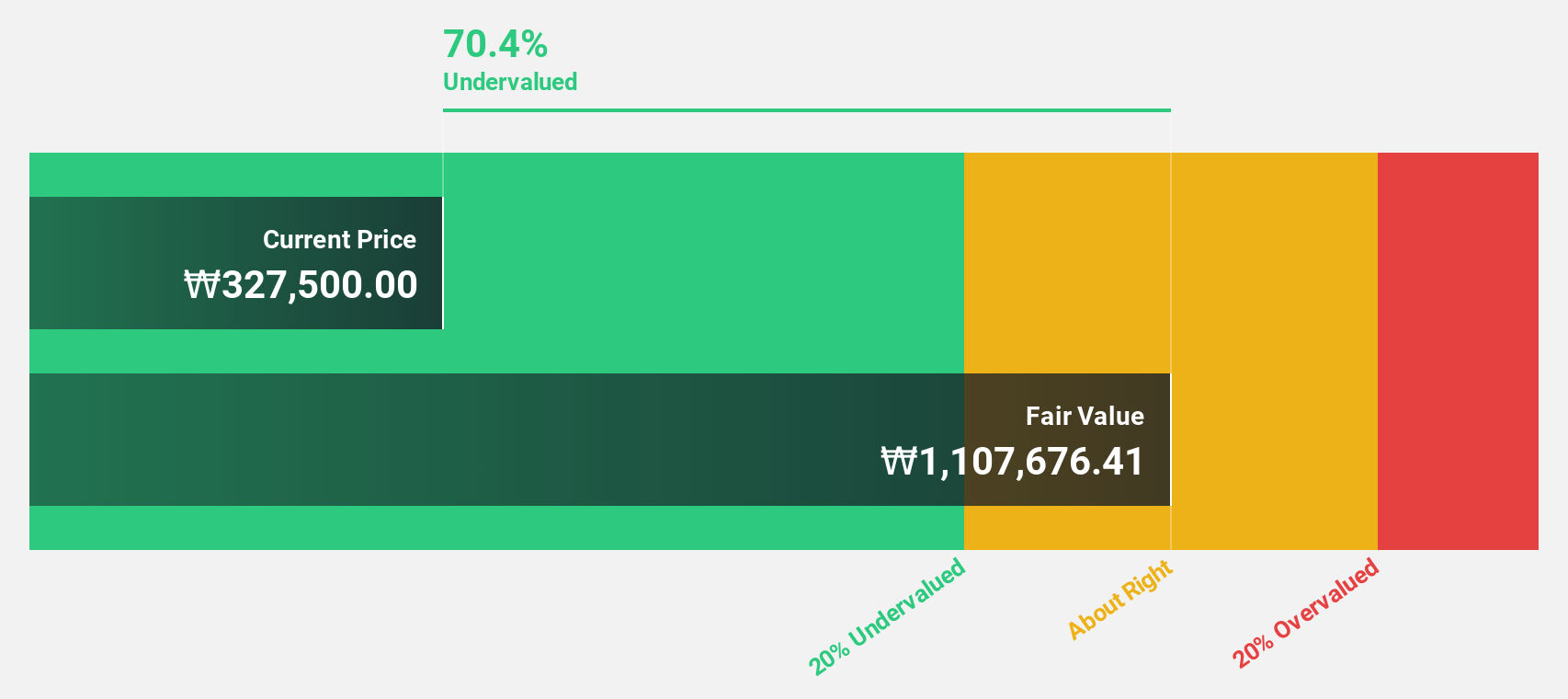

HD Korea Shipbuilding & Offshore Engineering (KOSE:A009540)

Overview: HD Korea Shipbuilding & Offshore Engineering Co., Ltd. (KOSE:A009540) operates in the shipbuilding and offshore engineering industry with a market cap of approximately ₩13.53 trillion.

Operations: The company's revenue segments include Shipbuilding (₩21.80 billion), Engine (₩4.21 billion), Green Energy (₩467.66 million), and Marine Plant (₩802.72 million).

Estimated Discount To Fair Value: 34.3%

HD Korea Shipbuilding & Offshore Engineering reported robust earnings for Q2 2024, with net income surging to ₩292.13 billion from ₩49.78 billion a year ago, driven by strong sales growth. Trading at ₩191,400, it is significantly undervalued compared to its estimated fair value of ₩291,415.06 based on discounted cash flows. Analysts forecast annual earnings growth of 38.72% over the next three years and revenue growth of 11.6% per year, outpacing the market average in South Korea.

- The analysis detailed in our HD Korea Shipbuilding & Offshore Engineering growth report hints at robust future financial performance.

- Dive into the specifics of HD Korea Shipbuilding & Offshore Engineering here with our thorough financial health report.

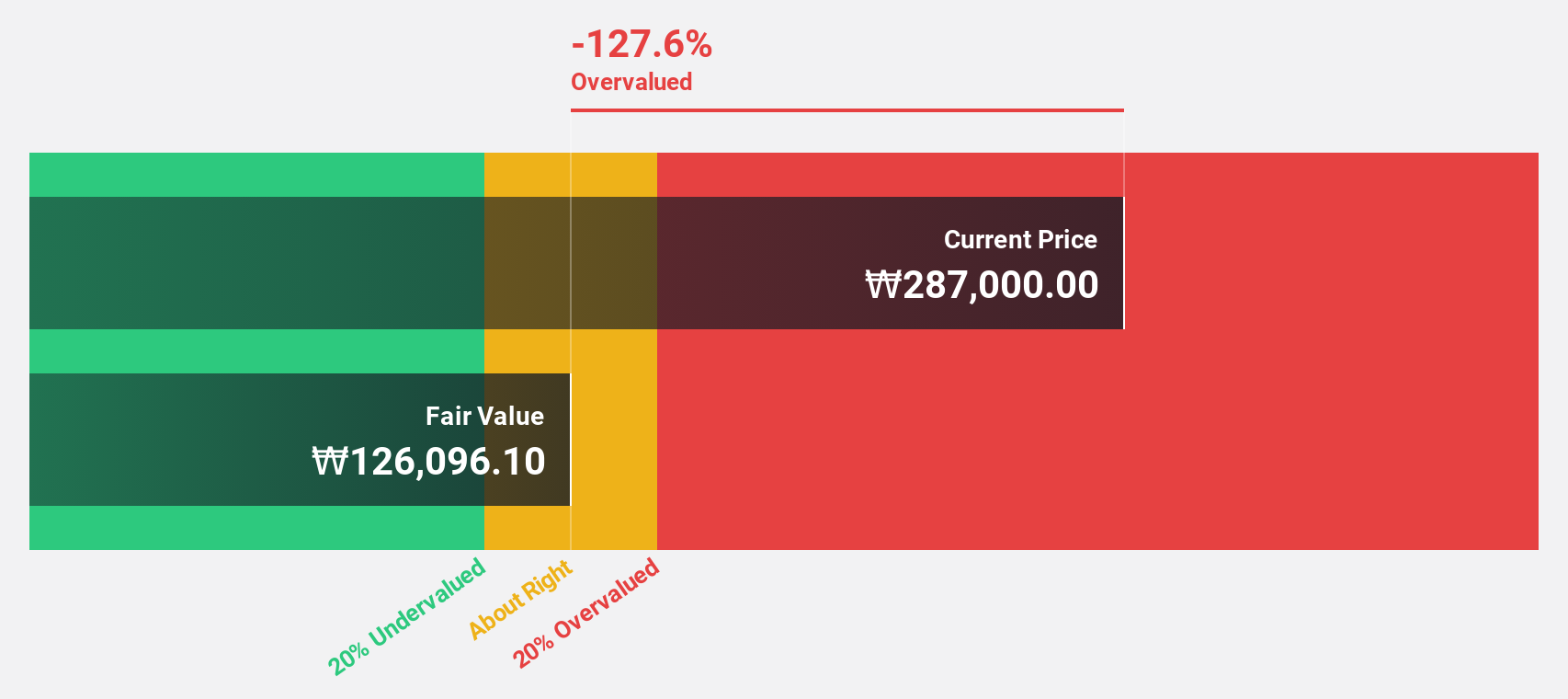

HYBE (KOSE:A352820)

Overview: HYBE Co., Ltd. operates in music production, publishing, and artist development and management with a market cap of ₩7.68 billion.

Operations: HYBE Co., Ltd. generates revenue from three main segments: Label (₩1.28 billion), Platform (₩361.12 million), and Solution (₩1.24 billion).

Estimated Discount To Fair Value: 19.3%

HYBE Co., Ltd. is trading at ₩184,400, below its estimated fair value of ₩228,529.11 based on discounted cash flows. Despite recent earnings declines and one-off items impacting results, the company’s annual profit growth is forecast at 42.47%, outpacing the KR market's 29.1%. Revenue growth is expected at 14.1% per year, faster than the market average of 10.8%. Additionally, HYBE announced a share repurchase program to stabilize stock prices.

- Our earnings growth report unveils the potential for significant increases in HYBE's future results.

- Unlock comprehensive insights into our analysis of HYBE stock in this financial health report.

Key Takeaways

- Unlock our comprehensive list of 31 Undervalued KRX Stocks Based On Cash Flows by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HYBE might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A352820

HYBE

Engages in the music production, publishing, and artist development and management businesses.

Excellent balance sheet with reasonable growth potential.