Advertisement

- South Korea

- /

- Media

- /

- KOSE:A095720

Woongjin Thinkbig Co., Ltd. (KRX:095720) Stock Rockets 25% But Many Are Still Ignoring The Company

Woongjin Thinkbig Co., Ltd. (KRX:095720) shares have continued their recent momentum with a 25% gain in the last month alone. Notwithstanding the latest gain, the annual share price return of 4.6% isn't as impressive.

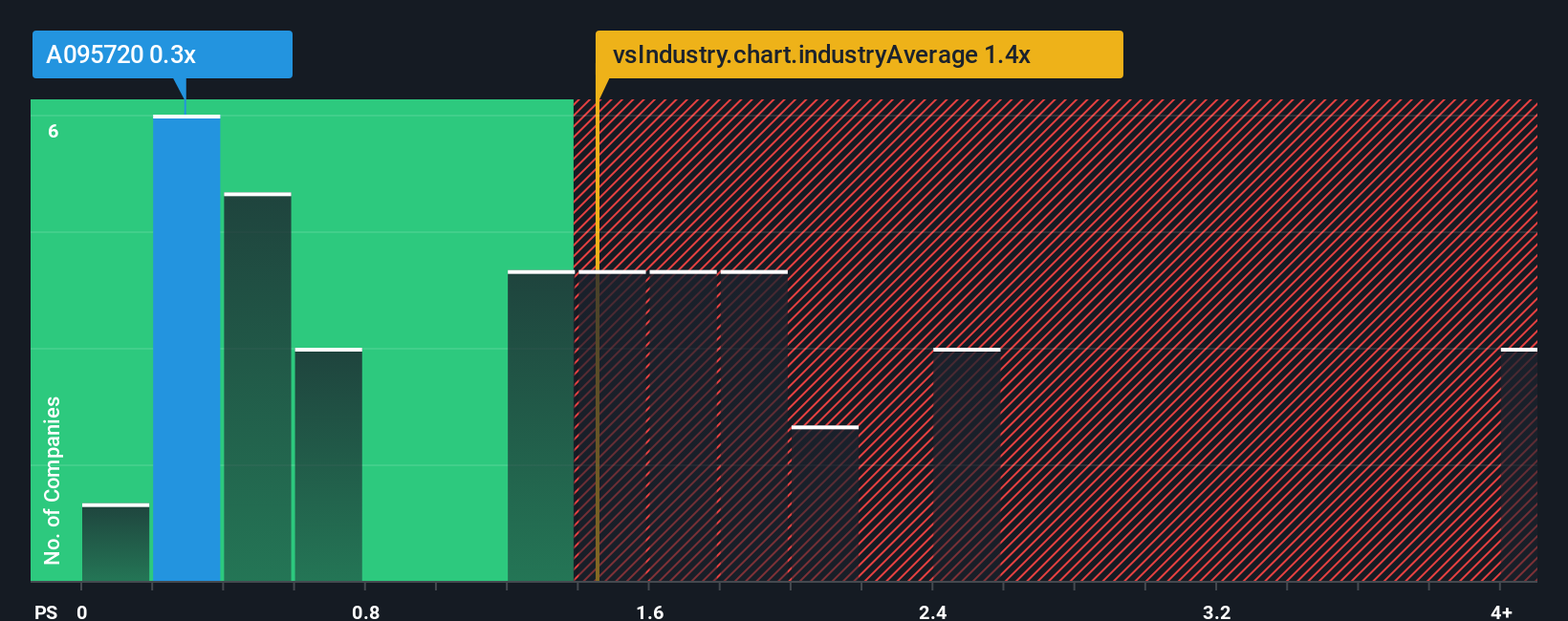

In spite of the firm bounce in price, when close to half the companies operating in Korea's Media industry have price-to-sales ratios (or "P/S") above 1.4x, you may still consider Woongjin Thinkbig as an enticing stock to check out with its 0.3x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

Check out our latest analysis for Woongjin Thinkbig

How Woongjin Thinkbig Has Been Performing

Woongjin Thinkbig hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. The P/S ratio is probably low because investors think this poor revenue performance isn't going to get any better. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Keen to find out how analysts think Woongjin Thinkbig's future stacks up against the industry? In that case, our free report is a great place to start.What Are Revenue Growth Metrics Telling Us About The Low P/S?

In order to justify its P/S ratio, Woongjin Thinkbig would need to produce sluggish growth that's trailing the industry.

Retrospectively, the last year delivered a frustrating 3.9% decrease to the company's top line. The last three years don't look nice either as the company has shrunk revenue by 2.5% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 6.1% during the coming year according to the lone analyst following the company. Meanwhile, the rest of the industry is forecast to only expand by 0.9%, which is noticeably less attractive.

With this in consideration, we find it intriguing that Woongjin Thinkbig's P/S sits behind most of its industry peers. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

What Does Woongjin Thinkbig's P/S Mean For Investors?

Despite Woongjin Thinkbig's share price climbing recently, its P/S still lags most other companies. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Woongjin Thinkbig's analyst forecasts revealed that its superior revenue outlook isn't contributing to its P/S anywhere near as much as we would have predicted. When we see strong growth forecasts like this, we can only assume potential risks are what might be placing significant pressure on the P/S ratio. While the possibility of the share price plunging seems unlikely due to the high growth forecasted for the company, the market does appear to have some hesitation.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Woongjin Thinkbig, and understanding should be part of your investment process.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Woongjin Thinkbig might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A095720

Woongjin Thinkbig

Engages in the publishing and education service business in South Korea.

Mediocre balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor