Advertisement

- South Korea

- /

- Chemicals

- /

- KOSDAQ:A126600

Here's Why BGFecomaterials (KOSDAQ:126600) Can Manage Its Debt Responsibly

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, BGFecomaterials CO., LTD. (KOSDAQ:126600) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for BGFecomaterials

How Much Debt Does BGFecomaterials Carry?

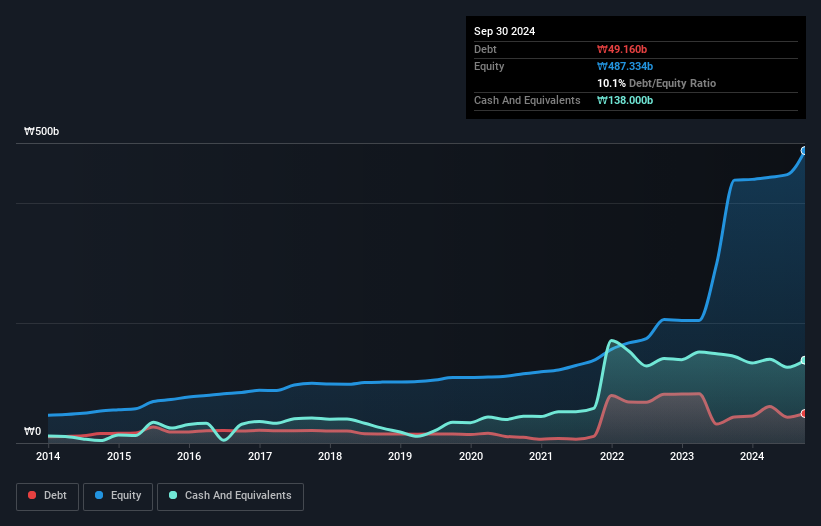

You can click the graphic below for the historical numbers, but it shows that as of September 2024 BGFecomaterials had ₩49.2b of debt, an increase on ₩43.4b, over one year. But on the other hand it also has ₩138.0b in cash, leading to a ₩88.8b net cash position.

How Strong Is BGFecomaterials' Balance Sheet?

We can see from the most recent balance sheet that BGFecomaterials had liabilities of ₩85.9b falling due within a year, and liabilities of ₩54.0b due beyond that. On the other hand, it had cash of ₩138.0b and ₩65.4b worth of receivables due within a year. So it actually has ₩63.5b more liquid assets than total liabilities.

This excess liquidity is a great indication that BGFecomaterials' balance sheet is almost as strong as Fort Knox. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Succinctly put, BGFecomaterials boasts net cash, so it's fair to say it does not have a heavy debt load!

Also good is that BGFecomaterials grew its EBIT at 11% over the last year, further increasing its ability to manage debt. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since BGFecomaterials will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While BGFecomaterials has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, BGFecomaterials burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that BGFecomaterials has net cash of ₩88.8b, as well as more liquid assets than liabilities. And it also grew its EBIT by 11% over the last year. So we are not troubled with BGFecomaterials's debt use. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 3 warning signs with BGFecomaterials (at least 1 which is significant) , and understanding them should be part of your investment process.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if BGFecomaterials might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A126600

BGFecomaterials

Manufactures and sells engineering plastic resins in South Korea and internationally.

Adequate balance sheet unattractive dividend payer.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor