Advertisement

- South Korea

- /

- Personal Products

- /

- KOSDAQ:A263920

Additional Considerations Required While Assessing HuM&C's (KOSDAQ:263920) Strong Earnings

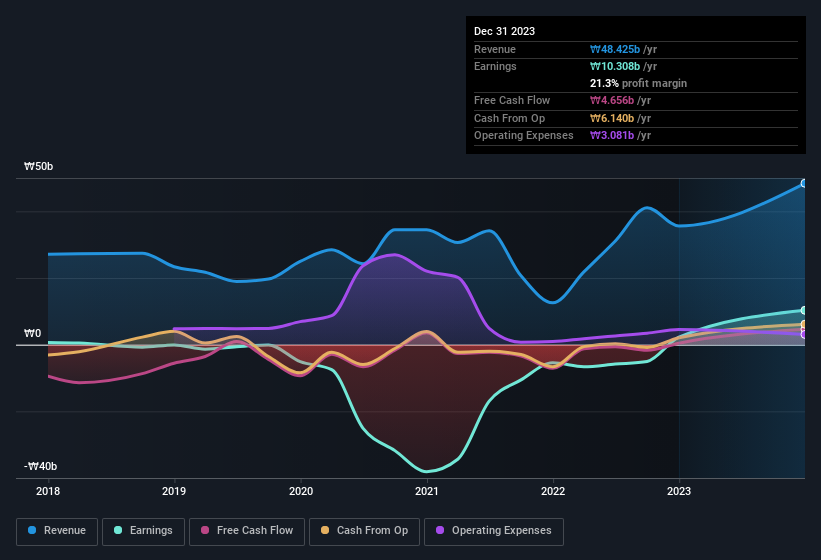

HuM&C Co., Ltd. (KOSDAQ:263920) announced strong profits, but the stock was stagnant. We did some digging, and we found some concerning factors in the details.

Check out our latest analysis for HuM&C

An Unusual Tax Situation

HuM&C reported a tax benefit of ₩2.2b, which is well worth noting. This is of course a bit out of the ordinary, given it is more common for companies to be paying tax than receiving tax benefits! Of course, prima facie it's great to receive a tax benefit. However, our data indicates that tax benefits can temporarily boost statutory profit in the year it is booked, but subsequently profit may fall back. In the likely event the tax benefit is not repeated, we'd expect to see its statutory profit levels drop, at least in the absence of strong growth. While we think it's good that the company has booked a tax benefit, it does mean that there's every chance the statutory profit will come in a lot higher than it would be if the income was adjusted for one-off factors.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of HuM&C.

Our Take On HuM&C's Profit Performance

As we have already discussed HuM&C reported that it received a tax benefit, rather than paying tax, in the last year. As a result we don't think its profit result, which includes that tax-boost, is a good guide to its sustainable profit levels. Therefore, it seems possible to us that HuM&C's true underlying earnings power is actually less than its statutory profit. The silver lining is that its EPS growth over the last year has been really wonderful, even if it's not a perfect measure. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. At Simply Wall St, we found 1 warning sign for HuM&C and we think they deserve your attention.

Today we've zoomed in on a single data point to better understand the nature of HuM&C's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

Valuation is complex, but we're here to simplify it.

Discover if HuM&C might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A263920

HuM&C

Engages in the manufacture and sale of various types of makeup products in South Korea and internationally.

Excellent balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|32.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.4% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|37.0% undervalued

AG

Community Contributor