- South Korea

- /

- Oil and Gas

- /

- KOSE:A002960

Exploring South Korea's Undiscovered Gems In October 2024

Reviewed by Simply Wall St

Over the last seven days, the South Korean market has remained flat, though it has seen a 7.8% increase over the past year with earnings forecasted to grow by 29% annually. In this dynamic environment, identifying stocks that are poised for growth yet remain underappreciated can offer unique opportunities for investors seeking to capitalize on emerging trends.

Top 10 Undiscovered Gems With Strong Fundamentals In South Korea

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| NOROO PAINT & COATINGS | 13.99% | 5.04% | 7.74% | ★★★★★★ |

| Miwon Chemicals | 0.08% | 11.70% | 14.38% | ★★★★★★ |

| Namuga | 14.47% | 0.88% | 38.25% | ★★★★★★ |

| Synergy Innovation | 12.39% | 12.87% | 28.82% | ★★★★★★ |

| ONEJOON | 10.13% | 35.30% | -5.78% | ★★★★★☆ |

| Oriental Precision & EngineeringLtd | 54.53% | 3.14% | 0.80% | ★★★★★☆ |

| iMarketKorea | 28.53% | 5.35% | 1.30% | ★★★★★☆ |

| Daewon Cable | 30.50% | 8.72% | 60.28% | ★★★★★☆ |

| PaperCorea | 53.09% | 1.31% | 77.27% | ★★★★★☆ |

| Itcen | 64.57% | 14.33% | -24.39% | ★★★★★☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

Boditech Med (KOSDAQ:A206640)

Simply Wall St Value Rating: ★★★★★★

Overview: Boditech Med Inc. provides instruments and diagnostic reagents both in South Korea and internationally, with a market cap of ₩351.61 billion.

Operations: Boditech Med generates revenue primarily from diagnostic kits and equipment, amounting to ₩139.13 billion. The company's market cap stands at ₩351.61 billion.

Boditech Med, a nimble player in South Korea's medical equipment sector, has shown impressive earnings growth of 34.6% over the past year, outpacing the industry average of 4%. The company is trading at a significant discount, about 53.6% below its estimated fair value. Financially robust, Boditech holds more cash than total debt and has reduced its debt-to-equity ratio from 31.2% to 4.3% over five years. Recently announcing a KRW 3 billion share repurchase plan to enhance shareholder value, it seems poised for continued growth with forecasted earnings expansion of about 16.55% annually.

- Click here and access our complete health analysis report to understand the dynamics of Boditech Med.

Assess Boditech Med's past performance with our detailed historical performance reports.

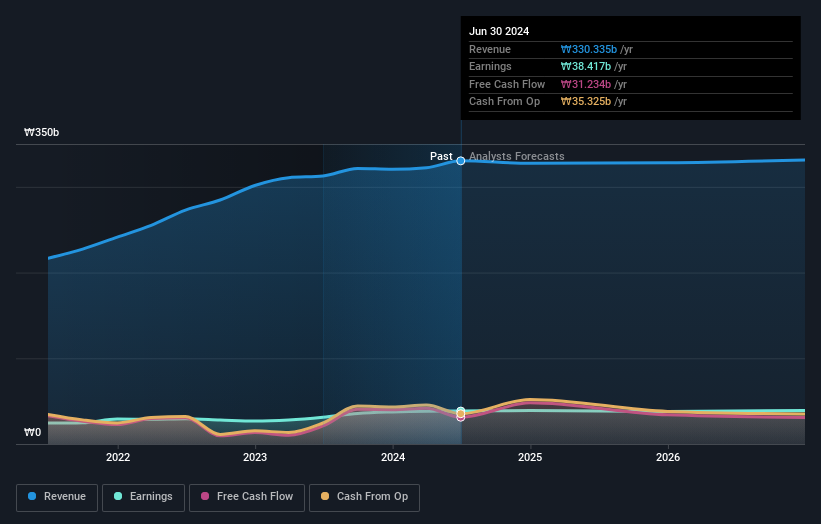

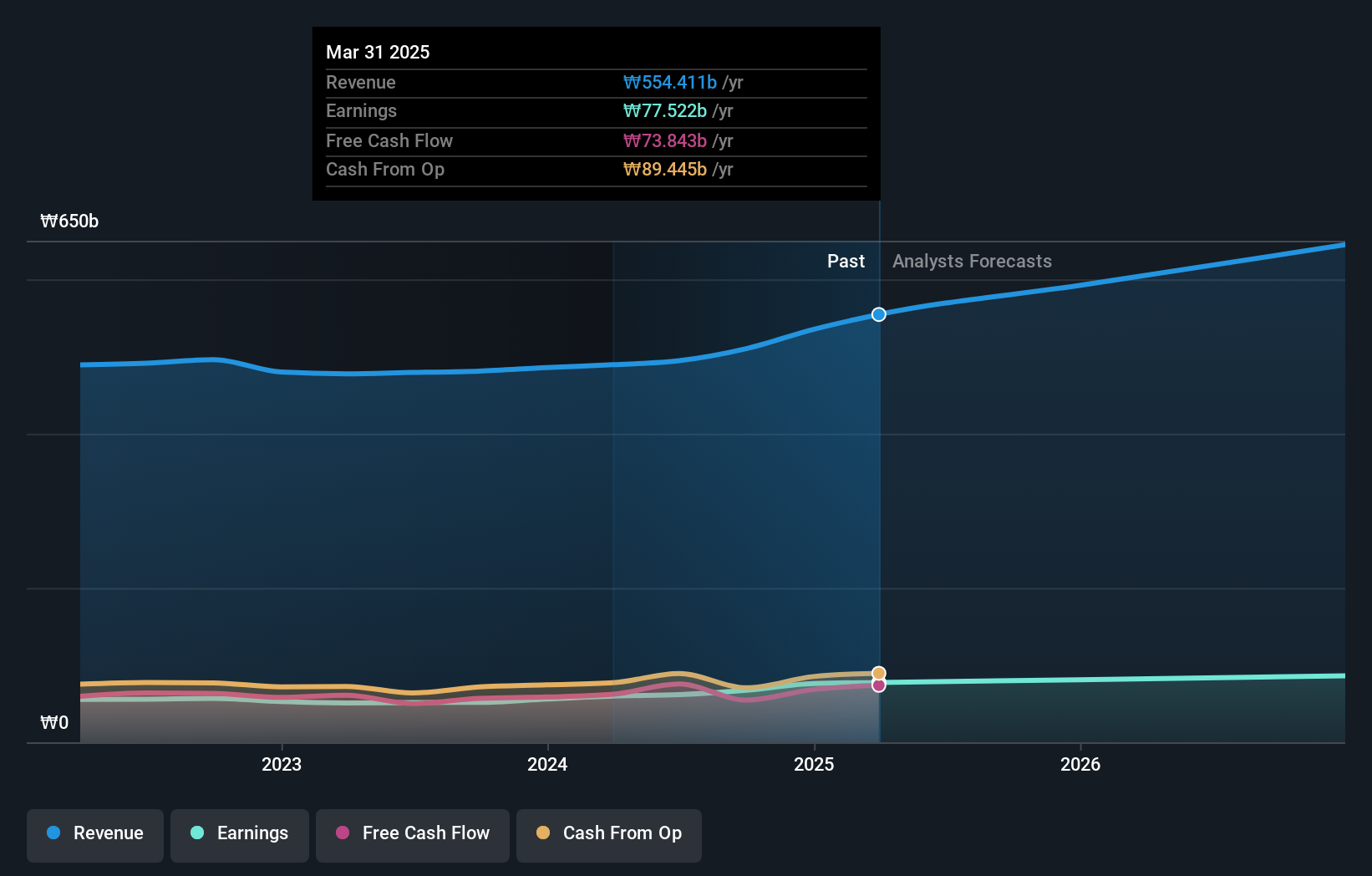

Hankook Shell OilLtd (KOSE:A002960)

Simply Wall St Value Rating: ★★★★★★

Overview: Hankook Shell Oil Co., Ltd. is involved in the manufacture, assembly, distribution, and marketing of lubricants, grease, and other petroleum-related products with a market cap of ₩417.95 billion.

Operations: Hankook Shell Oil Co., Ltd. generates revenue primarily from the sale of lubricants, grease, and petroleum-related products. The company's financial performance is influenced by its cost structure and market demand for these products.

Hankook Shell Oil, a nimble player in South Korea's oil and gas sector, has been making waves with its impressive financial health. The company boasts a 23.6% earnings growth over the past year, outpacing the industry average of -22.5%. Free from debt for five years, it eliminates concerns about interest coverage and showcases high-quality earnings. Recently added to the S&P Global BMI Index, Hankook Shell Oil trades at 17% below its estimated fair value, suggesting potential undervaluation. Its robust free cash flow further underscores financial stability amidst industry challenges.

NICE Information Service (KOSE:A030190)

Simply Wall St Value Rating: ★★★★★☆

Overview: NICE Information Service Co., Ltd. operates in South Korea offering credit evaluation, credit inquiries, credit investigations, and debt collection services with a market cap of approximately ₩663.84 billion.

Operations: NICE Information Service generates revenue primarily from corporate and personal credit information services, totaling ₩426.03 billion, and debt collection services, which contribute ₩68.44 billion.

NICE Information Service, a notable player in South Korea's financial sector, has shown impressive performance with earnings growing 19.9% over the past year, outpacing the Professional Services industry. The company reported net income of ₩18.75 billion for Q2 2024, up from ₩16.81 billion last year, and basic earnings per share increased to ₩319 from ₩284. With a debt-to-equity ratio rising modestly to 0.4% over five years and trading at 68.2% below its estimated fair value, it seems well-positioned financially while maintaining high-quality earnings and positive free cash flow prospects.

Seize The Opportunity

- Click through to start exploring the rest of the 177 KRX Undiscovered Gems With Strong Fundamentals now.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hankook Shell OilLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A002960

Hankook Shell OilLtd

Engages in the manufacture, assembly, distribution, and marketing of lubricants and grease, and other petroleum products and related products.

Outstanding track record with flawless balance sheet.