Advertisement

- South Korea

- /

- Healthcare Services

- /

- KOSDAQ:A067630

HLB Life Science (KOSDAQ:067630) Shareholders Should Be Cautious Despite Solid Earnings

The healthy profit announcement from HLB Life Science Co., Ltd. (KOSDAQ:067630 ) didn't seem to impress investors. We did some digging and found some worrying factors that they might be paying attention to.

View our latest analysis for HLB Life Science

A Closer Look At HLB Life Science's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. This ratio tells us how much of a company's profit is not backed by free cashflow.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

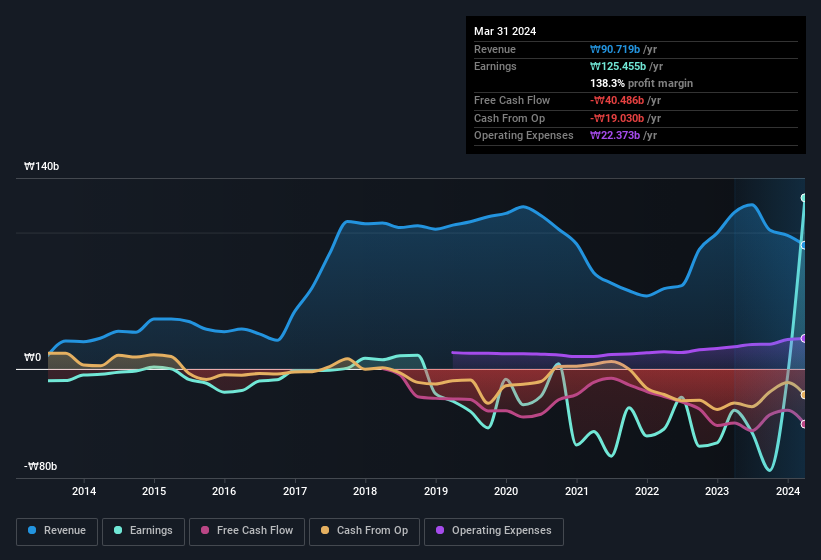

HLB Life Science has an accrual ratio of 0.48 for the year to March 2024. Statistically speaking, that's a real negative for future earnings. And indeed, during the period the company didn't produce any free cash flow whatsoever. Over the last year it actually had negative free cash flow of ₩40b, in contrast to the aforementioned profit of ₩125.5b. Coming off the back of negative free cash flow last year, we imagine some shareholders might wonder if its cash burn of ₩40b, this year, indicates high risk. Having said that, there is more to consider. We must also consider the impact of unusual items on statutory profit (and thus the accrual ratio), as well as note the ramifications of the company issuing new shares.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of HLB Life Science.

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. As it happens, HLB Life Science issued 5.8% more new shares over the last year. That means its earnings are split among a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of HLB Life Science's EPS by clicking here.

How Is Dilution Impacting HLB Life Science's Earnings Per Share (EPS)?

HLB Life Science was losing money three years ago. And even focusing only on the last twelve months, we don't have a meaningful growth rate because it made a loss a year ago, too. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). And so, you can see quite clearly that dilution is influencing shareholder earnings.

If HLB Life Science's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

The Impact Of Unusual Items On Profit

Given the accrual ratio, it's not overly surprising that HLB Life Science's profit was boosted by unusual items worth ₩41b in the last twelve months. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. Which is hardly surprising, given the name. HLB Life Science had a rather significant contribution from unusual items relative to its profit to March 2024. As a result, we can surmise that the unusual items are making its statutory profit significantly stronger than it would otherwise be.

Our Take On HLB Life Science's Profit Performance

In conclusion, HLB Life Science's weak accrual ratio suggested its statutory earnings have been inflated by the unusual items. The dilution means the results are weaker when viewed from a per-share perspective. For all the reasons mentioned above, we think that, at a glance, HLB Life Science's statutory profits could be considered to be low quality, because they are likely to give investors an overly positive impression of the company. Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. For example, HLB Life Science has 3 warning signs (and 2 which are a bit concerning) we think you should know about.

Our examination of HLB Life Science has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if HLB Life Science might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A067630

HLB Life Science

Develops and manufactures in vitro diagnostic medical devices and quasi-drugs in South Korea and internationally.

Imperfect balance sheet with minimal risk.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.6% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|14.9% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.2% undervalued

AG

Community Contributor