Advertisement

- South Korea

- /

- Food and Staples Retail

- /

- KOSE:A007070

Market Participants Recognise GS Retail Co., Ltd.'s (KRX:007070) Earnings

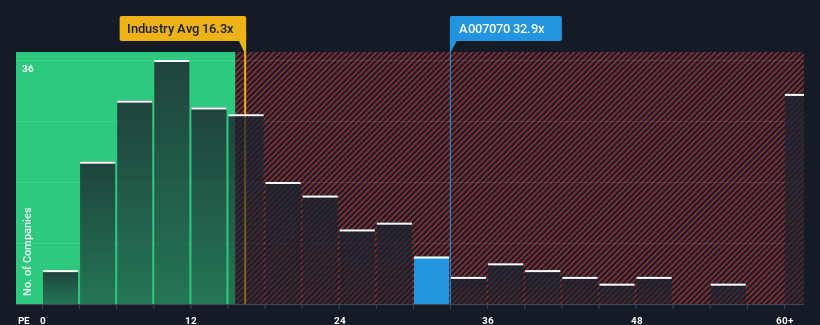

With a price-to-earnings (or "P/E") ratio of 32.9x GS Retail Co., Ltd. (KRX:007070) may be sending very bearish signals at the moment, given that almost half of all companies in Korea have P/E ratios under 11x and even P/E's lower than 6x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

While the market has experienced earnings growth lately, GS Retail's earnings have gone into reverse gear, which is not great. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

See our latest analysis for GS Retail

Is There Enough Growth For GS Retail?

In order to justify its P/E ratio, GS Retail would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered a frustrating 59% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 65% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Looking ahead now, EPS is anticipated to climb by 63% per year during the coming three years according to the analysts following the company. Meanwhile, the rest of the market is forecast to only expand by 16% each year, which is noticeably less attractive.

In light of this, it's understandable that GS Retail's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From GS Retail's P/E?

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that GS Retail maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

We don't want to rain on the parade too much, but we did also find 3 warning signs for GS Retail that you need to be mindful of.

Of course, you might also be able to find a better stock than GS Retail. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A007070

Undervalued with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor