Advertisement

- South Korea

- /

- Consumer Durables

- /

- KOSE:A009140

Kyungin Electronics' (KRX:009140) Returns On Capital Tell Us There Is Reason To Feel Uneasy

When it comes to investing, there are some useful financial metrics that can warn us when a business is potentially in trouble. More often than not, we'll see a declining return on capital employed (ROCE) and a declining amount of capital employed. This reveals that the company isn't compounding shareholder wealth because returns are falling and its net asset base is shrinking. So after glancing at the trends within Kyungin Electronics (KRX:009140), we weren't too hopeful.

What is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Kyungin Electronics, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

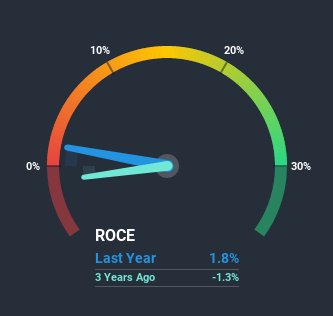

0.018 = ₩969m ÷ (₩58b - ₩2.5b) (Based on the trailing twelve months to December 2020).

So, Kyungin Electronics has an ROCE of 1.8%. Ultimately, that's a low return and it under-performs the Consumer Durables industry average of 9.4%.

See our latest analysis for Kyungin Electronics

Historical performance is a great place to start when researching a stock so above you can see the gauge for Kyungin Electronics' ROCE against it's prior returns. If you want to delve into the historical earnings, revenue and cash flow of Kyungin Electronics, check out these free graphs here.

How Are Returns Trending?

In terms of Kyungin Electronics' historical ROCE movements, the trend doesn't inspire confidence. To be more specific, the ROCE was 2.7% five years ago, but since then it has dropped noticeably. And on the capital employed front, the business is utilizing roughly the same amount of capital as it was back then. Since returns are falling and the business has the same amount of assets employed, this can suggest it's a mature business that hasn't had much growth in the last five years. If these trends continue, we wouldn't expect Kyungin Electronics to turn into a multi-bagger.

The Key Takeaway

All in all, the lower returns from the same amount of capital employed aren't exactly signs of a compounding machine. Yet despite these concerning fundamentals, the stock has performed strongly with a 42% return over the last five years, so investors appear very optimistic. Regardless, we don't feel too comfortable with the fundamentals so we'd be steering clear of this stock for now.

Kyungin Electronics does have some risks, we noticed 3 warning signs (and 2 which shouldn't be ignored) we think you should know about.

While Kyungin Electronics may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

If you decide to trade Kyungin Electronics, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Kyungin Electronics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A009140

Kyungin Electronics

Manufactures and sells electronic components in South Korea.

Flawless balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor