Advertisement

- China

- /

- Auto Components

- /

- SZSE:300100

Undiscovered Gems Three Promising Small Caps To Consider

Simply Wall St

Reviewed by Simply Wall St

In recent weeks, global markets have been marked by cautious sentiment following the Federal Reserve's rate cuts and hawkish forecasts, with smaller-cap indexes experiencing notable declines. Amid this backdrop of economic uncertainty and fluctuating investor confidence, small-cap stocks can present unique opportunities for those seeking potential growth in overlooked areas of the market. Identifying promising small caps involves looking for companies with strong fundamentals and innovative business models that can thrive even in challenging economic conditions.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Bahnhof | NA | 8.70% | 14.93% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| ABG Sundal Collier Holding | 18.07% | 0.55% | -4.76% | ★★★★★☆ |

| Evergent Investments | 5.49% | 1.15% | 8.81% | ★★★★★☆ |

| Intellego Technologies | 12.32% | 73.44% | 78.22% | ★★★★★☆ |

| HOMAG Group | NA | -31.14% | 23.43% | ★★★★★☆ |

| Nederman Holding | 73.66% | 10.94% | 15.88% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Lavipharm | 39.21% | 9.47% | -15.70% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

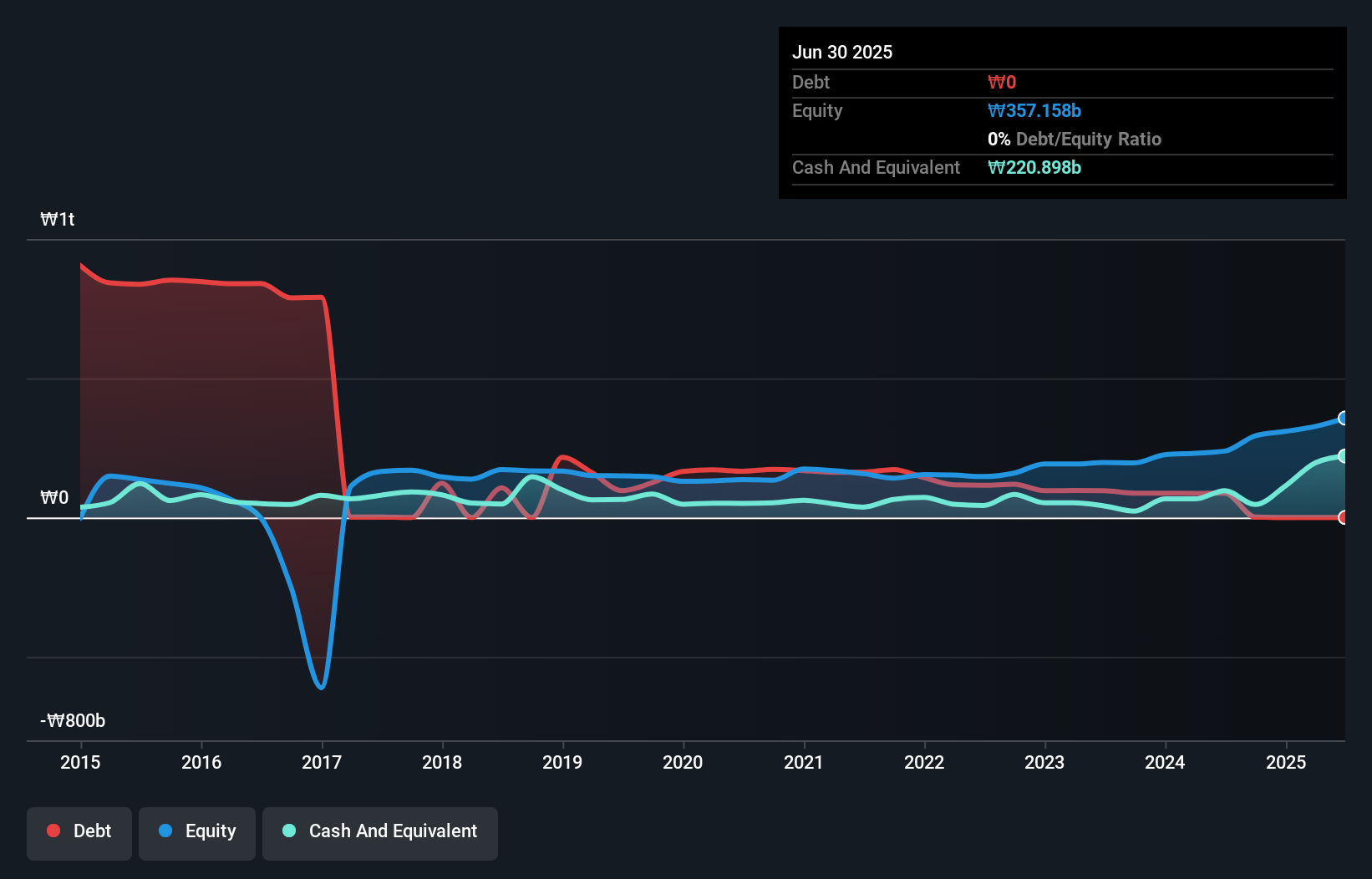

HD-Hyundai Marine Engine (KOSE:A071970)

Simply Wall St Value Rating: ★★★★★★

Overview: HD-Hyundai Marine Engine Co., Ltd. manufactures and sells marine engines, industrial facilities, and plants in South Korea and internationally with a market cap of ₩814.12 billion.

Operations: HD-Hyundai Marine Engine generates revenue primarily from its Engine and Equipment segment, which accounts for ₩307.81 billion. The company's financial performance is influenced by its cost structure and market dynamics within the marine engine industry.

HD-Hyundai Marine Engine has shown impressive earnings growth, with a 581.8% increase in the past year, outpacing the Machinery industry's -1.8%. The company reported third-quarter sales of KRW 80.79 million, up from KRW 69.23 million last year, and net income of KRW 9.51 million compared to a net loss previously recorded. Despite shareholder dilution over the past year, HD-Hyundai maintains high-quality earnings and boasts a debt-to-equity ratio that has improved significantly from 85.5% to just 0.6% over five years, indicating effective debt management and financial health amidst industry challenges.

- Click to explore a detailed breakdown of our findings in HD-Hyundai Marine Engine's health report.

Assess HD-Hyundai Marine Engine's past performance with our detailed historical performance reports.

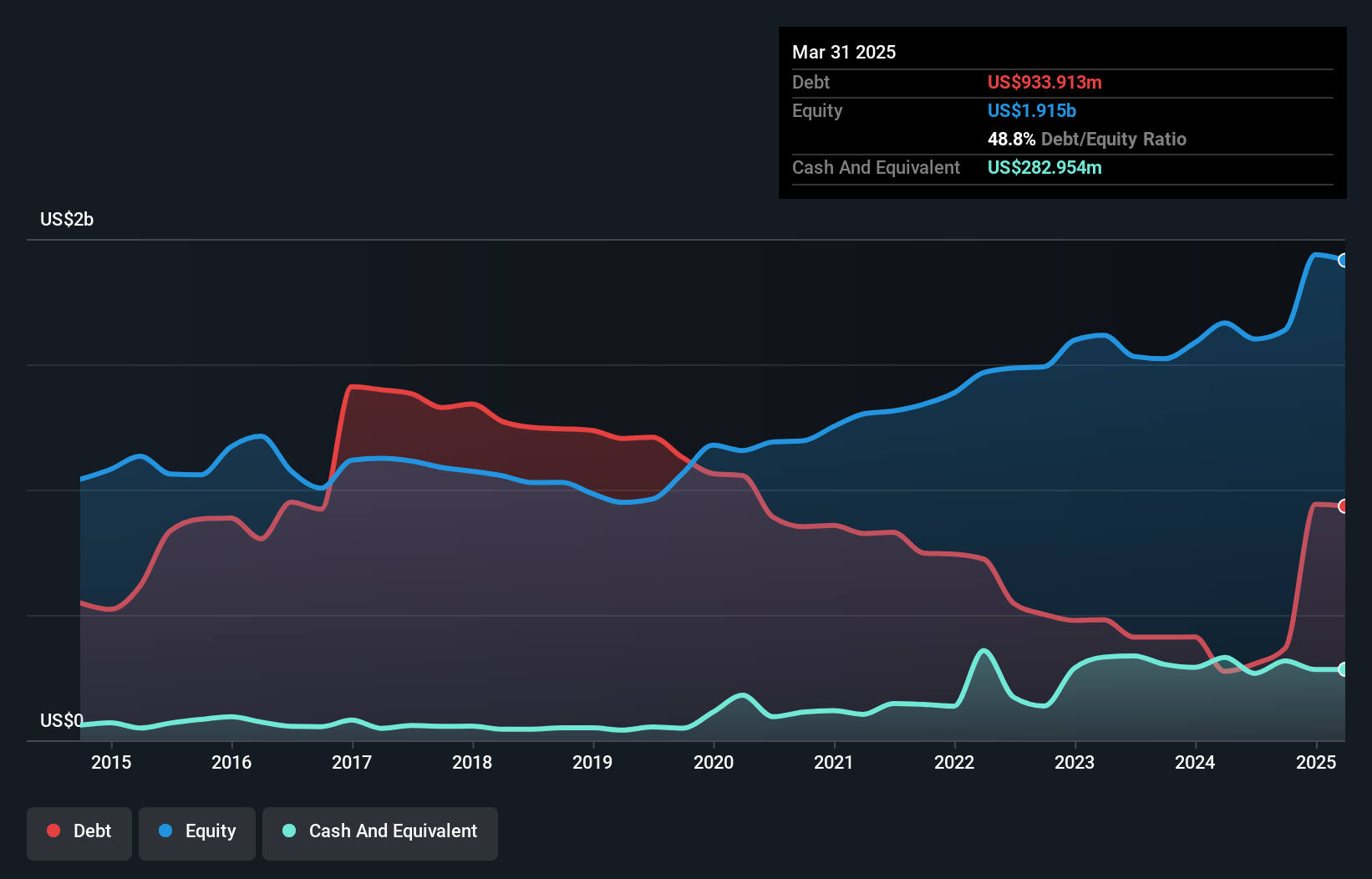

BWG (OB:BWLPG)

Simply Wall St Value Rating: ★★★★★★

Overview: BW LPG Limited is an investment holding company involved in ship owning and chartering activities globally, with a market capitalization of NOK17.26 billion.

Operations: BW LPG Limited generates revenue primarily from its Shipping and Product Services segments, with the latter contributing $2.57 billion. The company's net profit margin is 12.5%, reflecting its profitability in these operations.

BW LPG, a notable player in the oil and gas sector, has demonstrated robust financial health with a net debt to equity ratio of 3.1%, considered satisfactory. The company recently expanded its fleet by acquiring several Very Large Gas Carriers (VLGCs), issuing new shares as partial payment. Despite significant insider selling over the past three months, BW LPG's earnings grew by 15.7% last year, outpacing industry growth of -3.7%. Trading at 80.9% below estimated fair value and boasting high-quality earnings, it presents an intriguing investment opportunity amidst current market conditions.

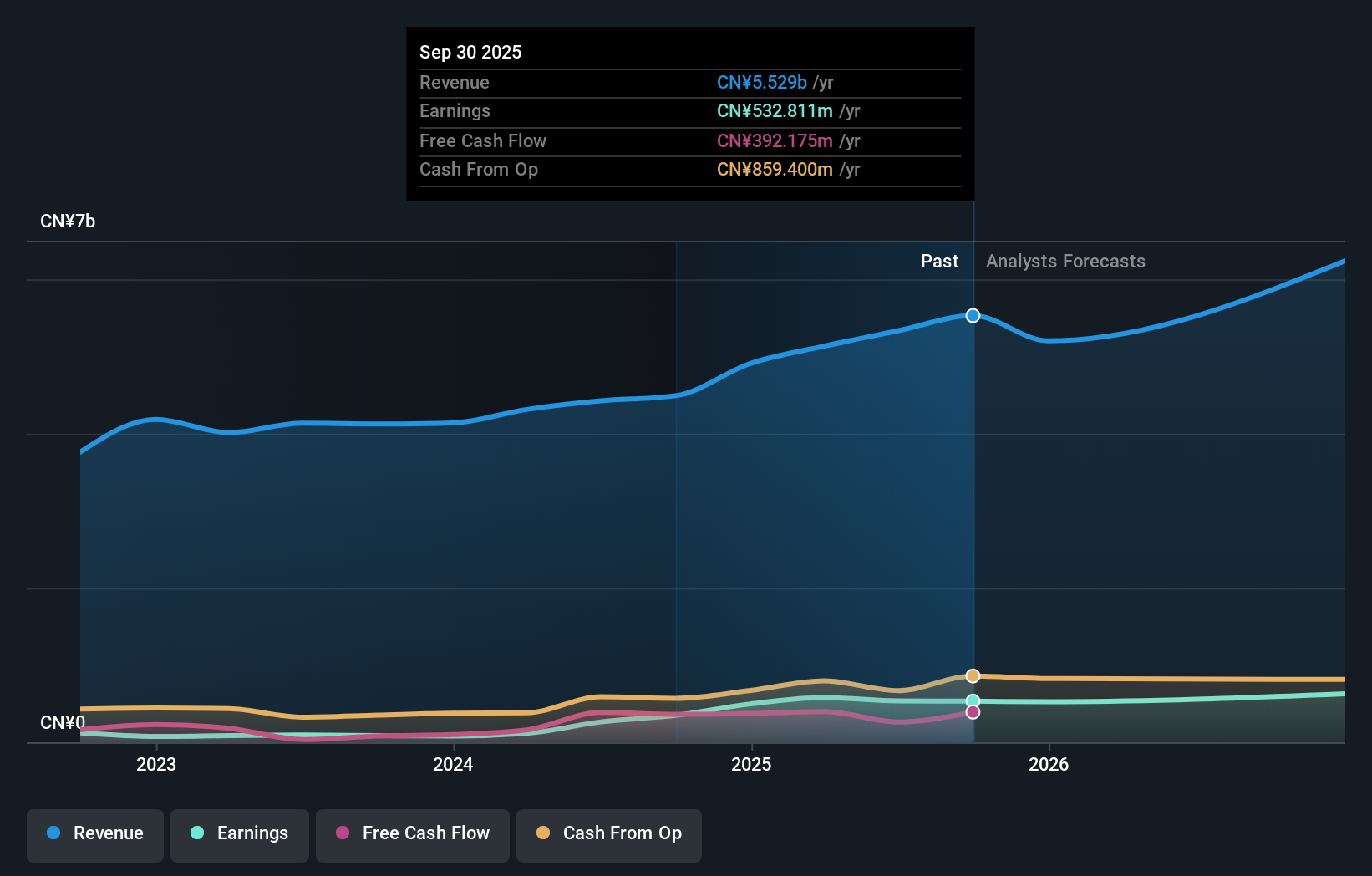

Ningbo Shuanglin Auto PartsLtd (SZSE:300100)

Simply Wall St Value Rating: ★★★★★★

Overview: Ningbo Shuanglin Auto Parts Co., Ltd. is involved in the research, development, manufacture, and sale of auto parts both in China and internationally, with a market cap of CN¥12.11 billion.

Operations: Shuanglin Auto Parts generates revenue primarily from the sale of auto parts in both domestic and international markets. The company's net profit margin stands at 6.5%, reflecting its profitability after accounting for all expenses.

Ningbo Shuanglin Auto Parts, known for its robust performance in the auto components sector, has demonstrated impressive growth. Over the past year, earnings surged by 300.1%, outpacing industry averages of 10.5%. The company's net debt to equity ratio stands at a satisfactory 15.5%, reflecting prudent financial management as it reduced from 75% to 32% over five years. Recent earnings reports highlight sales of CNY 3.24 billion and net income of CNY 366 million for nine months ending September, a significant rise from last year's figures. Despite recent volatility in share price, future earnings are projected to grow annually by nearly 12%.

Summing It All Up

- Navigate through the entire inventory of 4621 Undiscovered Gems With Strong Fundamentals here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300100

Shuanglin

Engages in the research and development, manufacture, and sale of auto parts in China and internationally.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor