Advertisement

- South Korea

- /

- Construction

- /

- KOSE:A028100

A Piece Of The Puzzle Missing From Dong-Ah Geological Engineering Company Ltd.'s (KRX:028100) Share Price

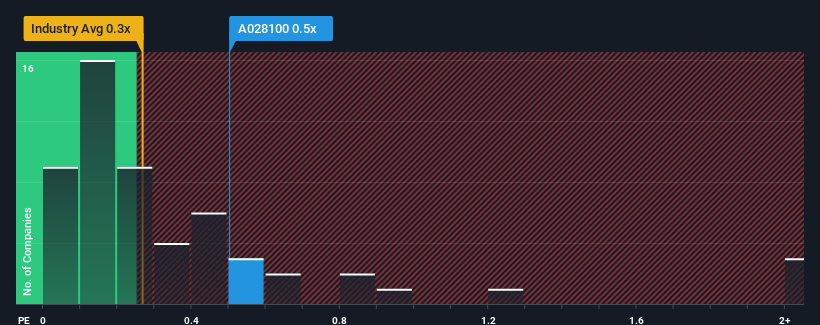

There wouldn't be many who think Dong-Ah Geological Engineering Company Ltd.'s (KRX:028100) price-to-sales (or "P/S") ratio of 0.5x is worth a mention when the median P/S for the Construction industry in Korea is similar at about 0.3x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Dong-Ah Geological Engineering

How Dong-Ah Geological Engineering Has Been Performing

The revenue growth achieved at Dong-Ah Geological Engineering over the last year would be more than acceptable for most companies. It might be that many expect the respectable revenue performance to wane, which has kept the P/S from rising. Those who are bullish on Dong-Ah Geological Engineering will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Dong-Ah Geological Engineering's earnings, revenue and cash flow.How Is Dong-Ah Geological Engineering's Revenue Growth Trending?

In order to justify its P/S ratio, Dong-Ah Geological Engineering would need to produce growth that's similar to the industry.

Taking a look back first, we see that the company grew revenue by an impressive 18% last year. The latest three year period has also seen a 22% overall rise in revenue, aided extensively by its short-term performance. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

When compared to the industry's one-year growth forecast of 0.5%, the most recent medium-term revenue trajectory is noticeably more alluring

With this information, we find it interesting that Dong-Ah Geological Engineering is trading at a fairly similar P/S compared to the industry. It may be that most investors are not convinced the company can maintain its recent growth rates.

The Bottom Line On Dong-Ah Geological Engineering's P/S

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Dong-Ah Geological Engineering currently trades on a lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. When we see strong revenue with faster-than-industry growth, we can only assume potential risks are what might be placing pressure on the P/S ratio. At least the risk of a price drop looks to be subdued if recent medium-term revenue trends continue, but investors seem to think future revenue could see some volatility.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Dong-Ah Geological Engineering (1 is a bit concerning!) that you need to be mindful of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A028100

Dong-Ah Geological Engineering

Dong-Ah Geological Engineering Company Ltd.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor