Advertisement

- South Korea

- /

- Machinery

- /

- KOSDAQ:A382480

Why G.I. Tech's (KOSDAQ:382480) Shaky Earnings Are Just The Beginning Of Its Problems

G.I. Tech Co., Ltd.'s (KOSDAQ:382480) recent weak earnings report didn't cause a big stock movement. We think that investors are worried about some weaknesses underlying the earnings.

Check out our latest analysis for G.I. Tech

Zooming In On G.I. Tech's Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. This ratio tells us how much of a company's profit is not backed by free cashflow.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

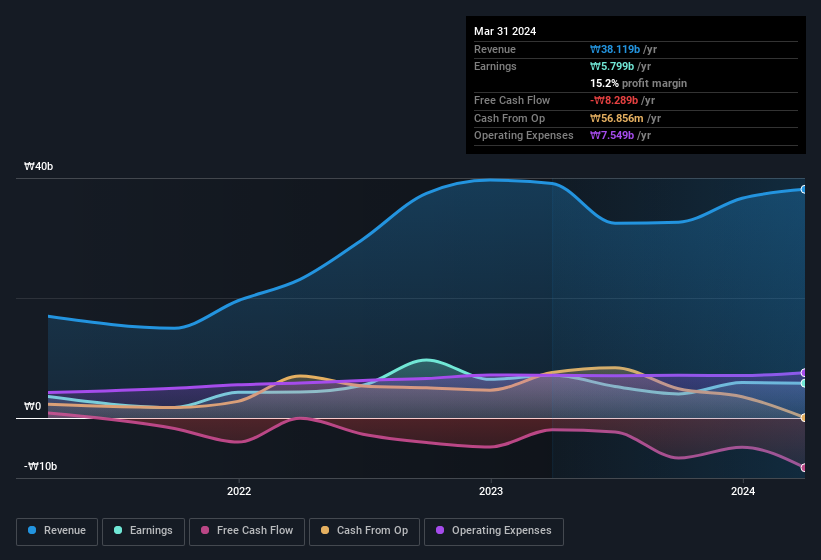

G.I. Tech has an accrual ratio of 0.27 for the year to March 2024. We can therefore deduce that its free cash flow fell well short of covering its statutory profit. Even though it reported a profit of ₩5.80b, a look at free cash flow indicates it actually burnt through ₩8.3b in the last year. We also note that G.I. Tech's free cash flow was actually negative last year as well, so we could understand if shareholders were bothered by its outflow of ₩8.3b. Importantly, we note an unusual tax situation, which we discuss below, has impacted the accruals ratio. This would partially explain why the accrual ratio was so poor.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of G.I. Tech.

An Unusual Tax Situation

Moving on from the accrual ratio, we note that G.I. Tech profited from a tax benefit which contributed ₩720m to profit. This is meaningful because companies usually pay tax rather than receive tax benefits. Of course, prima facie it's great to receive a tax benefit. However, the devil in the detail is that these kind of benefits only impact in the year they are booked, and are often one-off in nature. In the likely event the tax benefit is not repeated, we'd expect to see its statutory profit levels drop, at least in the absence of strong growth. So while we think it's great to receive a tax benefit, it does tend to imply an increased risk that the statutory profit overstates the sustainable earnings power of the business.

Our Take On G.I. Tech's Profit Performance

G.I. Tech's accrual ratio indicates weak cashflow relative to earnings, which perhaps arises in part from the tax benefit it received this year. If the tax benefit is not repeated, then profit would drop next year, all else being equal. Considering all this we'd argue G.I. Tech's profits probably give an overly generous impression of its sustainable level of profitability. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. Every company has risks, and we've spotted 3 warning signs for G.I. Tech (of which 2 are potentially serious!) you should know about.

Our examination of G.I. Tech has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A382480

G.I. Tech

Engages in the manufacture of special-purpose machinery products in South Korea.

Adequate balance sheet slight.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|31.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.7% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|35.8% undervalued

AG

Community Contributor