Advertisement

- South Korea

- /

- Auto Components

- /

- KOSE:A033250

It's Down 26% But CHASYS Co., Ltd. (KRX:033250) Could Be Riskier Than It Looks

CHASYS Co., Ltd. (KRX:033250) shareholders that were waiting for something to happen have been dealt a blow with a 26% share price drop in the last month. Looking at the bigger picture, even after this poor month the stock is up 52% in the last year.

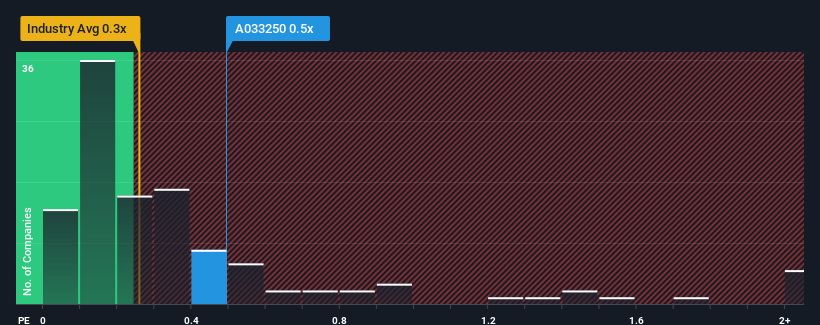

Even after such a large drop in price, it's still not a stretch to say that CHASYS' price-to-sales (or "P/S") ratio of 0.5x right now seems quite "middle-of-the-road" compared to the Auto Components industry in Korea, where the median P/S ratio is around 0.3x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for CHASYS

How Has CHASYS Performed Recently?

With revenue growth that's exceedingly strong of late, CHASYS has been doing very well. Perhaps the market is expecting future revenue performance to taper off, which has kept the P/S from rising. Those who are bullish on CHASYS will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

Although there are no analyst estimates available for CHASYS, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.How Is CHASYS' Revenue Growth Trending?

There's an inherent assumption that a company should be matching the industry for P/S ratios like CHASYS' to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 84%. The strong recent performance means it was also able to grow revenue by 86% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 5.9% shows it's noticeably more attractive.

With this information, we find it interesting that CHASYS is trading at a fairly similar P/S compared to the industry. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

The Key Takeaway

With its share price dropping off a cliff, the P/S for CHASYS looks to be in line with the rest of the Auto Components industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that CHASYS currently trades on a lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. When we see strong revenue with faster-than-industry growth, we can only assume potential risks are what might be placing pressure on the P/S ratio. At least the risk of a price drop looks to be subdued if recent medium-term revenue trends continue, but investors seem to think future revenue could see some volatility.

Having said that, be aware CHASYS is showing 2 warning signs in our investment analysis, you should know about.

If you're unsure about the strength of CHASYS' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A033250

CHASYS

Manufactures and sells automotive chassis systems and rear axles in South Korea and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor