Advertisement

- South Korea

- /

- Auto Components

- /

- KOSE:A004100

Taeyang Metal Industrial's (KRX:004100) Returns On Capital Are Heading Higher

What trends should we look for it we want to identify stocks that can multiply in value over the long term? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. So when we looked at Taeyang Metal Industrial (KRX:004100) and its trend of ROCE, we really liked what we saw.

Return On Capital Employed (ROCE): What Is It?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Taeyang Metal Industrial, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

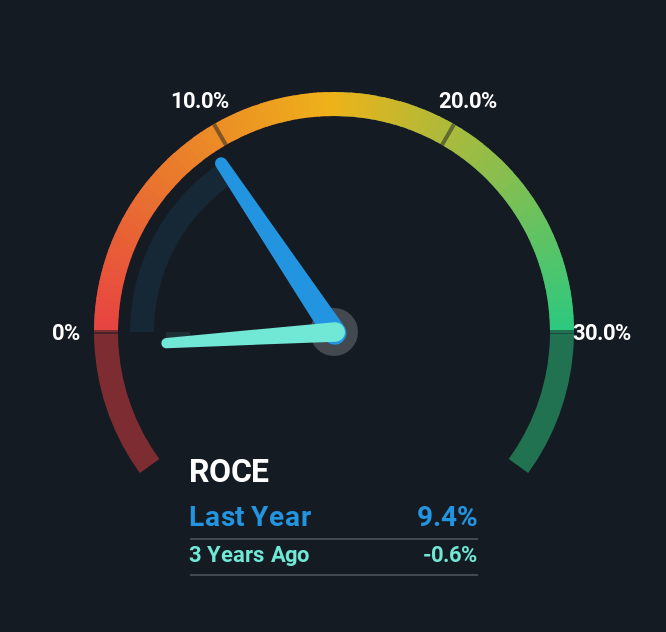

0.094 = ₩18b ÷ (₩543b - ₩352b) (Based on the trailing twelve months to March 2025).

Thus, Taeyang Metal Industrial has an ROCE of 9.4%. In absolute terms, that's a low return but it's around the Auto Components industry average of 7.9%.

Check out our latest analysis for Taeyang Metal Industrial

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how Taeyang Metal Industrial has performed in the past in other metrics, you can view this free graph of Taeyang Metal Industrial's past earnings, revenue and cash flow.

What Can We Tell From Taeyang Metal Industrial's ROCE Trend?

Taeyang Metal Industrial has recently broken into profitability so their prior investments seem to be paying off. The company was generating losses five years ago, but now it's earning 9.4% which is a sight for sore eyes. And unsurprisingly, like most companies trying to break into the black, Taeyang Metal Industrial is utilizing 25% more capital than it was five years ago. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, both common traits of a multi-bagger.

On a separate but related note, it's important to know that Taeyang Metal Industrial has a current liabilities to total assets ratio of 65%, which we'd consider pretty high. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

In Conclusion...

Long story short, we're delighted to see that Taeyang Metal Industrial's reinvestment activities have paid off and the company is now profitable. And a remarkable 126% total return over the last five years tells us that investors are expecting more good things to come in the future. Therefore, we think it would be worth your time to check if these trends are going to continue.

Taeyang Metal Industrial does have some risks, we noticed 5 warning signs (and 1 which is potentially serious) we think you should know about.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if Taeyang Metal Industrial might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A004100

Taeyang Metal Industrial

Produces and sells cold forging and precision machining parts for automobiles in South Korea and internationally.

Slightly overvalued with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor