Advertisement

- Japan

- /

- Renewable Energy

- /

- TSE:9517

Industry Analysts Just Upgraded Their eREX Co.,Ltd. (TSE:9517) Revenue Forecasts By 14%

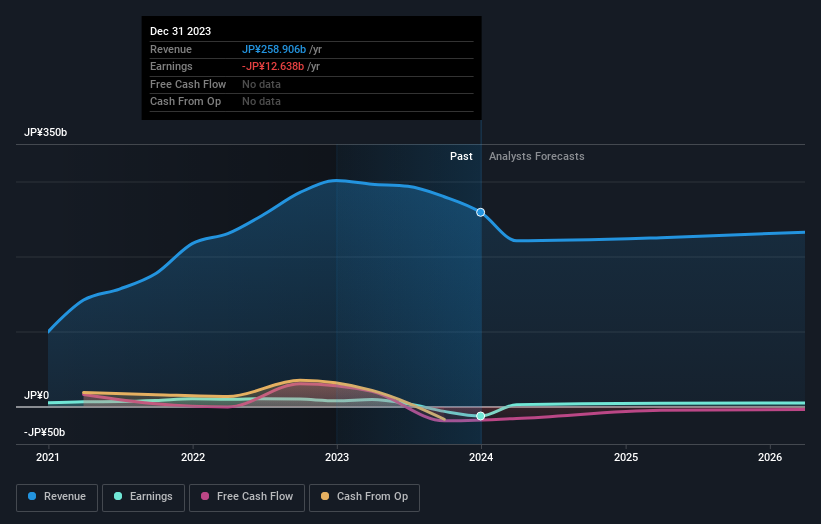

eREX Co.,Ltd. (TSE:9517) shareholders will have a reason to smile today, with the analysts making substantial upgrades to next year's forecasts. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects.

After the upgrade, the consensus from eREXLtd's twin analysts is for revenues of JP¥225b in 2025, which would reflect a not inconsiderable 13% decline in sales compared to the last year of performance. The losses are expected to disappear over the next year or so, with forecasts for a profit of JP¥73.37 per share next year. Before this latest update, the analysts had been forecasting revenues of JP¥198b and earnings per share (EPS) of JP¥70.83 in 2025. Sentiment certainly seems to have improved in recent times, with a decent improvement in revenue and a small lift in earnings per share estimates.

View our latest analysis for eREXLtd

With these upgrades, we're not surprised to see that the analysts have lifted their price target 5.7% to JP¥840 per share.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 11% by the end of 2025. This indicates a significant reduction from annual growth of 33% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 2.8% annually for the foreseeable future. It's pretty clear that eREXLtd's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that analysts upgraded their earnings per share estimates for next year, expecting improving business conditions. Pleasantly, analysts also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow slower than the wider market. There was also an increase in the price target, suggesting that there is more optimism baked into the forecasts than there was previously. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at eREXLtd.

These earnings upgrades look like a sterling endorsement, but before diving in - you should know that we've spotted 3 potential concern with eREXLtd, including the risk of cutting its dividend. You can learn more, and discover the 1 other concern we've identified, for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:9517

eREXLtd

Engages in the electric power business in Japan and internationally.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor