Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:6996

Nichicon Corporation Just Beat Earnings Expectations: Here's What Analysts Think Will Happen Next

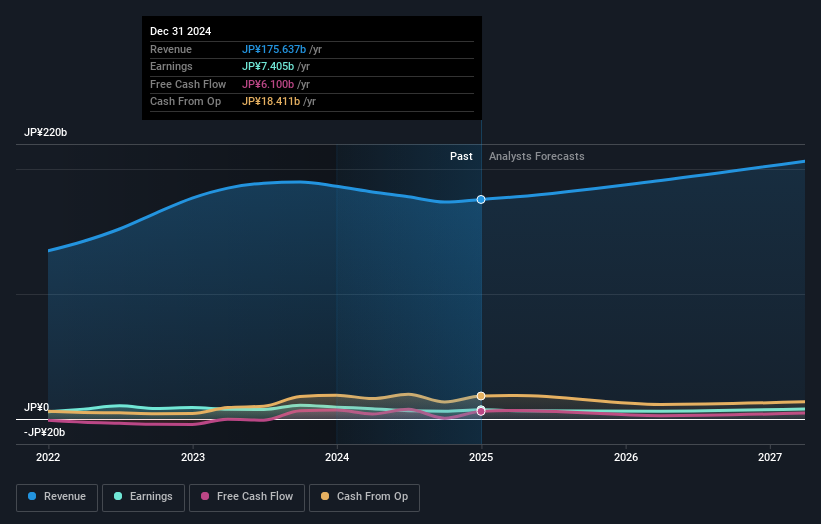

A week ago, Nichicon Corporation (TSE:6996) came out with a strong set of third-quarter numbers that could potentially lead to a re-rate of the stock. The company beat forecasts, with revenue of JP¥48b, some 6.7% above estimates, and statutory earnings per share (EPS) coming in at JP¥45.26, 182% ahead of expectations. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

View our latest analysis for Nichicon

Following the latest results, Nichicon's seven analysts are now forecasting revenues of JP¥190.8b in 2026. This would be a decent 8.6% improvement in revenue compared to the last 12 months. Statutory earnings per share are forecast to descend 15% to JP¥91.67 in the same period. Yet prior to the latest earnings, the analysts had been anticipated revenues of JP¥189.1b and earnings per share (EPS) of JP¥88.82 in 2026. The analysts seems to have become more bullish on the business, judging by their new earnings per share estimates.

The consensus price target rose 10% to JP¥1,220, suggesting that higher earnings estimates flow through to the stock's valuation as well. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on Nichicon, with the most bullish analyst valuing it at JP¥1,400 and the most bearish at JP¥1,000 per share. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Nichicon's past performance and to peers in the same industry. We would highlight that Nichicon's revenue growth is expected to slow, with the forecast 6.9% annualised growth rate until the end of 2026 being well below the historical 11% p.a. growth over the last five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 7.2% annually. So it's pretty clear that, while Nichicon's revenue growth is expected to slow, it's expected to grow roughly in line with the industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Nichicon following these results. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

With that in mind, we wouldn't be too quick to come to a conclusion on Nichicon. Long-term earnings power is much more important than next year's profits. We have forecasts for Nichicon going out to 2027, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 2 warning signs for Nichicon that you should be aware of.

Valuation is complex, but we're here to simplify it.

Discover if Nichicon might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6996

Nichicon

Engages in the development and production of electrical components in Japan, the United States, Asia, Europe, and internationally.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

106 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

936 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

144 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative