Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:6856

Evaluating HORIBA (TSE:6856): Is There Value Left After the Recent Stock Surge?

Simply Wall St

Reviewed by Kshitija Bhandaru

HORIBA (TSE:6856) has seen its stock price move steadily higher over the past month, catching the interest of investors looking for opportunities in the Japanese technology sector. The company's recent gains prompt a closer look at what is driving sentiment now.

See our latest analysis for HORIBA.

HORIBA’s share price is showing real momentum, with a 41.58% year-to-date share price return and a 41.59% one-year total shareholder return. This signals that optimism is building around its outlook. The steady climb reflects growing investor confidence, supported by recent gains and a strong multi-year performance.

If strong share price surges in the tech sector have your attention, now is a smart time to see who else is making moves with our See the full list for free.

With such impressive momentum, the essential question is whether HORIBA’s stock remains undervalued at current levels, or if the recent rally means future growth is already factored in by the market. Is there still room to buy, or is it all priced in?

Price-to-Earnings of 14.9x: Is it justified?

HORIBA's shares are trading at a price-to-earnings (P/E) ratio of 14.9x, which puts the company's valuation slightly below the average P/E ratio of direct peers at 17.1x. This suggests that investors may be assigning a modest discount compared to comparable companies.

The P/E ratio is a widely used measure for valuing technology sector stocks because it reflects the market's expectations for future earnings relative to current profitability. In HORIBA's case, a lower-than-peer P/E may indicate the market has more modest growth expectations or is being conservative despite the recent momentum in the share price.

Against the broader JP Electronic industry, however, the company's P/E is actually a bit above the sector average of 14.7x. This hints at nuanced market sentiment; while investors aren't prepared to pay a full sector premium, they see slightly more earnings potential than many other electronics firms. Compared to the estimated Fair Price-to-Earnings Ratio (17.5x), there's still some headroom. If multiples move closer to the fair value, there could be further upside.

Explore the SWS fair ratio for HORIBA

Result: Price-to-Earnings of 14.9x (UNDERVALUED)

However, despite current momentum, slower revenue growth or weaker net income trends could present challenges for HORIBA's positive outlook going forward.

Find out about the key risks to this HORIBA narrative.

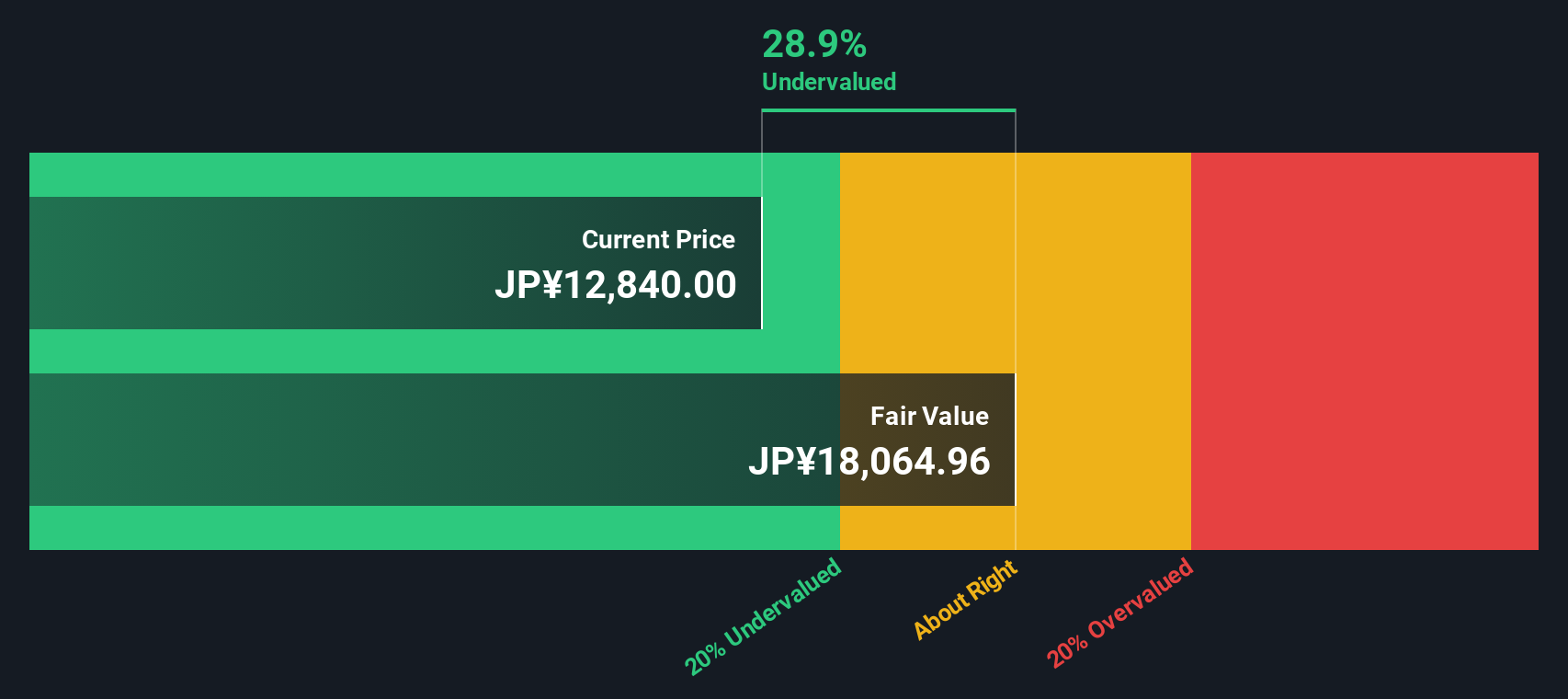

Another View: What Does the DCF Model Say?

While multiples suggest HORIBA is trading at a discount compared to peers, our SWS DCF model provides a different perspective. It estimates the company’s fair value at ¥17,996.6, which makes the current price of ¥12,870 appear undervalued by almost 29%. Does this deeper value suggest real opportunity, or could there be hidden risks in the forecast?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out HORIBA for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own HORIBA Narrative

If you want to take a different approach or prefer to investigate the numbers for yourself, it's quick and easy to build your own perspective on HORIBA, usually in under three minutes. Do it your way

A great starting point for your HORIBA research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors never settle for just one opportunity. Take the next step and broaden your horizons with these compelling stock ideas that could shape your portfolio’s future.

- Boost your income by tapping into these 18 dividend stocks with yields > 3%, which offers yields above 3% and strong fundamentals backing every payout.

- Ride powerful megatrends in tech by checking out these 24 AI penny stocks, where artificial intelligence drives tomorrow’s breakthrough growth stories.

- Position for future innovation with these 26 quantum computing stocks, unlocking the game-changers in quantum computing and next-level problem solving potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HORIBA might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6856

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor