Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:6762

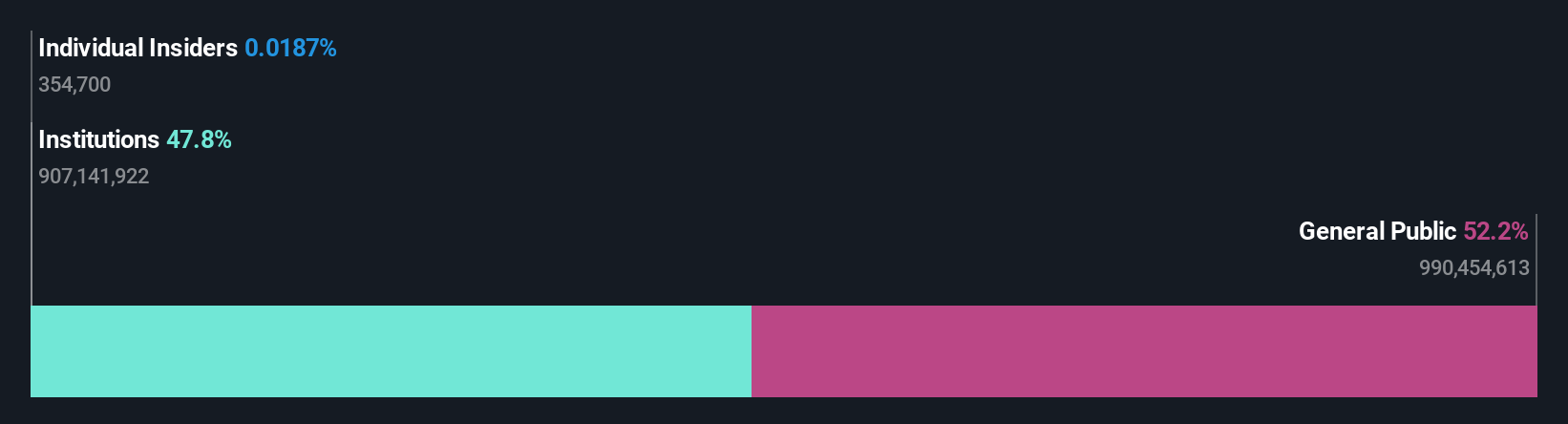

Retail investors who hold 52% of TDK Corporation (TSE:6762) gained 6.0%, institutions profited as well

Key Insights

- Significant control over TDK by retail investors implies that the general public has more power to influence management and governance-related decisions

- 42% of the business is held by the top 25 shareholders

- Institutional ownership in TDK is 48%

If you want to know who really controls TDK Corporation (TSE:6762), then you'll have to look at the makeup of its share registry. The group holding the most number of shares in the company, around 52% to be precise, is retail investors. Put another way, the group faces the maximum upside potential (or downside risk).

Retail investors gained the most after market cap touched JP¥4.9t last week, while institutions who own 48% also benefitted.

In the chart below, we zoom in on the different ownership groups of TDK.

Check out our latest analysis for TDK

What Does The Institutional Ownership Tell Us About TDK?

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index.

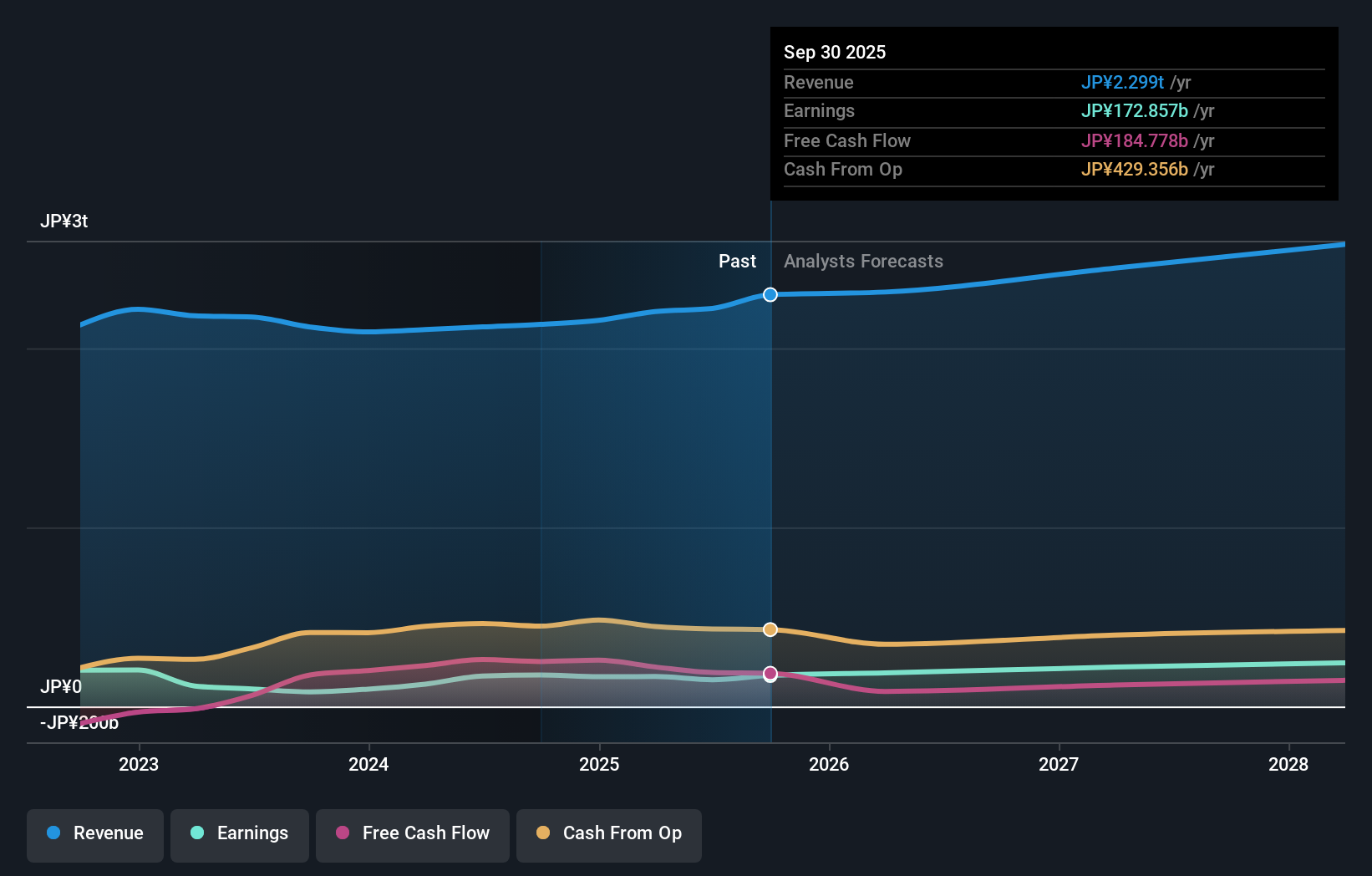

We can see that TDK does have institutional investors; and they hold a good portion of the company's stock. This can indicate that the company has a certain degree of credibility in the investment community. However, it is best to be wary of relying on the supposed validation that comes with institutional investors. They too, get it wrong sometimes. If multiple institutions change their view on a stock at the same time, you could see the share price drop fast. It's therefore worth looking at TDK's earnings history below. Of course, the future is what really matters.

We note that hedge funds don't have a meaningful investment in TDK. BlackRock, Inc. is currently the company's largest shareholder with 8.3% of shares outstanding. Amova Asset Management Co., Ltd. is the second largest shareholder owning 5.8% of common stock, and Daiwa Asset Management Co., Ltd. holds about 5.0% of the company stock.

Our studies suggest that the top 25 shareholders collectively control less than half of the company's shares, meaning that the company's shares are widely disseminated and there is no dominant shareholder.

Researching institutional ownership is a good way to gauge and filter a stock's expected performance. The same can be achieved by studying analyst sentiments. There are plenty of analysts covering the stock, so it might be worth seeing what they are forecasting, too.

Insider Ownership Of TDK

The definition of company insiders can be subjective and does vary between jurisdictions. Our data reflects individual insiders, capturing board members at the very least. Management ultimately answers to the board. However, it is not uncommon for managers to be executive board members, especially if they are a founder or the CEO.

I generally consider insider ownership to be a good thing. However, on some occasions it makes it more difficult for other shareholders to hold the board accountable for decisions.

Our data suggests that insiders own under 1% of TDK Corporation in their own names. As it is a large company, we'd only expect insiders to own a small percentage of it. But it's worth noting that they own JP¥908m worth of shares. It is good to see board members owning shares, but it might be worth checking if those insiders have been buying.

General Public Ownership

The general public -- including retail investors -- own 52% of TDK. This size of ownership gives investors from the general public some collective power. They can and probably do influence decisions on executive compensation, dividend policies and proposed business acquisitions.

Next Steps:

It's always worth thinking about the different groups who own shares in a company. But to understand TDK better, we need to consider many other factors. Case in point: We've spotted 1 warning sign for TDK you should be aware of.

If you would prefer discover what analysts are predicting in terms of future growth, do not miss this free report on analyst forecasts.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Valuation is complex, but we're here to simplify it.

Discover if TDK might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6762

TDK

Engages in manufacture and sale of electronic components in Japan, Europe, China, Asia, the Americas, and internationally.

Flawless balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

106 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

936 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

143 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative