Advertisement

- Japan

- /

- Communications

- /

- TSE:6659

Media Links Co.,Ltd. (TSE:6659) Shares May Have Slumped 26% But Getting In Cheap Is Still Unlikely

To the annoyance of some shareholders, Media Links Co.,Ltd. (TSE:6659) shares are down a considerable 26% in the last month, which continues a horrid run for the company. The good news is that in the last year, the stock has shone bright like a diamond, gaining 111%.

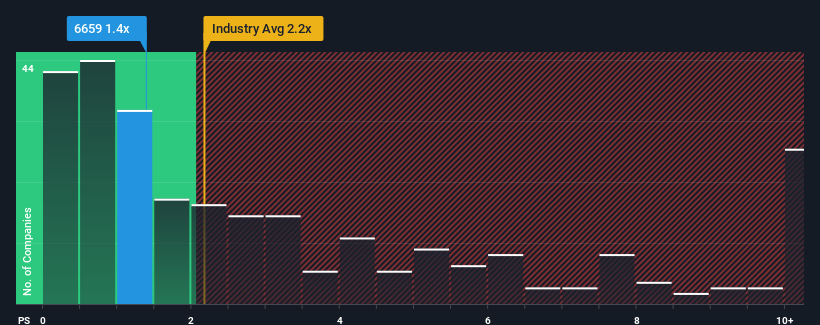

In spite of the heavy fall in price, when almost half of the companies in Japan's Communications industry have price-to-sales ratios (or "P/S") below 0.7x, you may still consider Media LinksLtd as a stock probably not worth researching with its 1.4x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

View our latest analysis for Media LinksLtd

What Does Media LinksLtd's P/S Mean For Shareholders?

Revenue has risen firmly for Media LinksLtd recently, which is pleasing to see. Perhaps the market is expecting this decent revenue performance to beat out the industry over the near term, which has kept the P/S propped up. However, if this isn't the case, investors might get caught out paying too much for the stock.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Media LinksLtd's earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For Media LinksLtd?

In order to justify its P/S ratio, Media LinksLtd would need to produce impressive growth in excess of the industry.

Retrospectively, the last year delivered an exceptional 23% gain to the company's top line. Revenue has also lifted 20% in aggregate from three years ago, mostly thanks to the last 12 months of growth. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 38% shows it's noticeably less attractive.

With this information, we find it concerning that Media LinksLtd is trading at a P/S higher than the industry. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

The Final Word

There's still some elevation in Media LinksLtd's P/S, even if the same can't be said for its share price recently. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Media LinksLtd revealed its poor three-year revenue trends aren't detracting from the P/S as much as we though, given they look worse than current industry expectations. Right now we aren't comfortable with the high P/S as this revenue performance isn't likely to support such positive sentiment for long. Unless there is a significant improvement in the company's medium-term performance, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

You need to take note of risks, for example - Media LinksLtd has 3 warning signs (and 2 which are potentially serious) we think you should know about.

If you're unsure about the strength of Media LinksLtd's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6659

Media LinksLtd

Develops, manufactures, and sells video communication equipment for broadcast industry in Japan and internationally.

Flawless balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor