Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:5214

Assessing Nippon Electric Glass (TSE:5214) Valuation After Recent Share Price Surge

Simply Wall St

Reviewed by Simply Wall St

If you have been tracking Nippon Electric Glass (TSE:5214) lately, you might be wondering what is behind the recent attention. While there has not been a headline-grabbing event, the stock’s movement over the past month is beginning to turn heads among investors. Moves like this, even without a specific announcement, can sometimes signal that the market is reassessing a company’s prospects or getting positioned ahead of an anticipated change.

Over the past year, Nippon Electric Glass shares have logged gains of nearly 59%, with momentum picking up pace in the past quarter. The stock has jumped 43% in the past three months and is up 17% over the past month alone, suggesting a shift in sentiment or renewed interest. This stands in strong contrast to the more muted results earlier in the year, which could indicate either optimism for the business or a change in risk appetite among investors.

Given this run-up, the key question is whether Nippon Electric Glass has more room to climb, or if the current price already reflects its best-case scenario.

Price-to-Sales of 1.2x: Is it justified?

Based on the preferred valuation metric, Nippon Electric Glass currently trades at a price-to-sales (P/S) ratio of 1.2x. Compared to the Japanese Electronic industry average of 0.7x and the estimated fair P/S ratio of 0.7x, this places the stock at a premium.

The price-to-sales ratio compares a company’s market capitalization to its total sales. This offers a simple measure of how much investors are willing to pay for each unit of revenue. It is particularly useful for evaluating companies that are currently unprofitable, as it helps strip out distortions from negative earnings.

A P/S ratio higher than the sector average may indicate that investors expect stronger future growth or improved profitability. However, in this case it suggests the market could be overvaluing the company's current revenue given its ongoing losses.

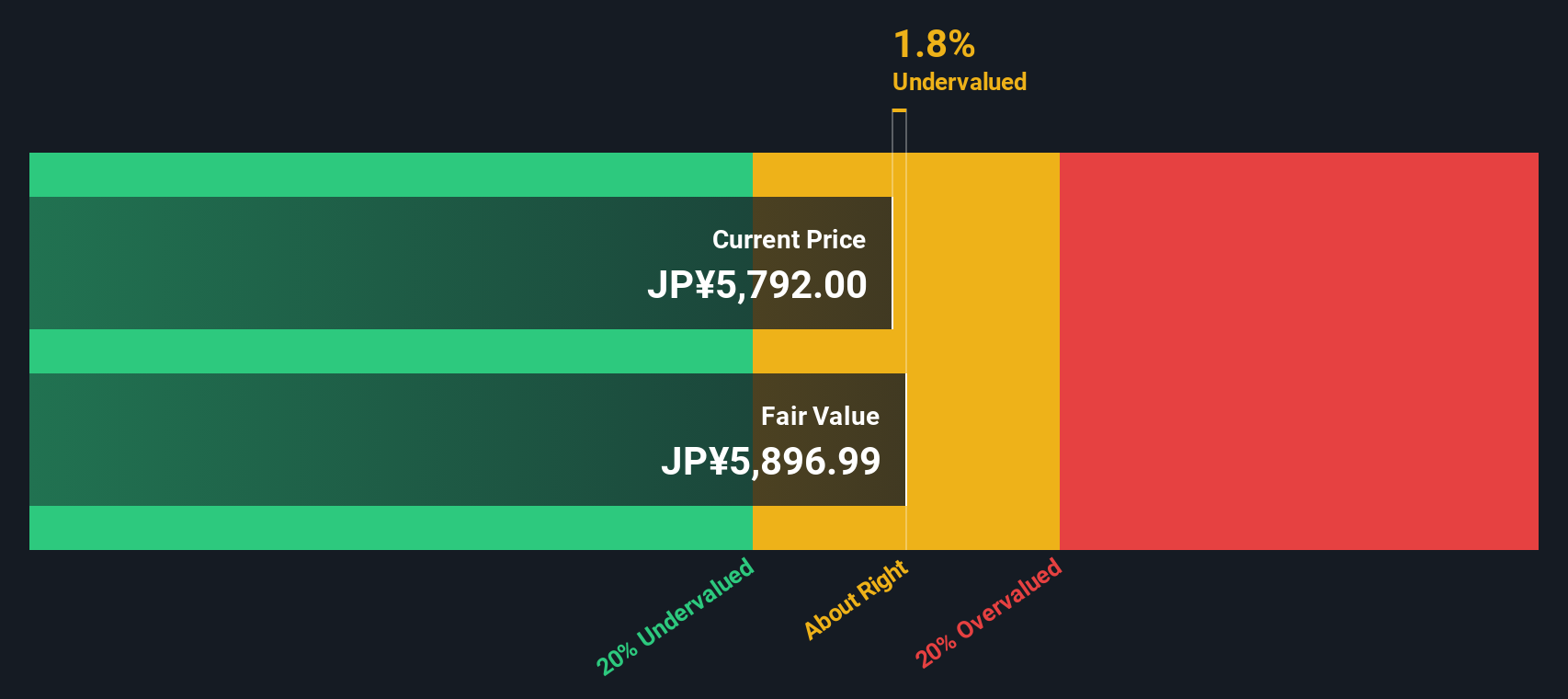

Result: Fair Value of ¥5,393.96 (UNDERVALUED)

See our latest analysis for Nippon Electric Glass.However, weak net income and a price above analyst targets could signal downside if growth expectations are not met in upcoming quarters.

Find out about the key risks to this Nippon Electric Glass narrative.Another View: What Does Our DCF Model Say?

While the current price-to-sales ratio puts Nippon Electric Glass at a premium, our DCF model offers a different perspective by factoring in expected future cash flows. This approach also suggests the shares could be undervalued. However, can both views be right?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Nippon Electric Glass Narrative

If you see things differently or want to dig into the details yourself, you can craft your own view in just a few minutes. Do it your way

A great starting point for your Nippon Electric Glass research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Give yourself an edge in your portfolio by checking out dynamic opportunities that most investors are missing. Let Simply Wall Street’s tools guide you to smarter investing moves today.

- Unlock stable returns with assets that offer attractive yields by using our guide to dividend stocks with yields > 3%.

- Spot hidden gems primed for growth by investigating companies ranked as undervalued stocks based on cash flows.

- Power your strategy with exposure to cutting-edge breakthroughs in medicine through the world of healthcare AI stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nippon Electric Glass might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:5214

Nippon Electric Glass

Manufactures and sells specialty glass products and glass manufacturing machinery in Japan and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

934 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative