Advertisement

- Taiwan

- /

- Electronic Equipment and Components

- /

- TWSE:6191

Three Undiscovered Gems To Enhance Your Portfolio

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate through a period of economic uncertainty, marked by rate cuts from the ECB and SNB and a potential Fed rate cut on the horizon, small-cap stocks have faced challenges, with indices like the Russell 2000 underperforming against their larger counterparts. In such an environment, identifying undiscovered gems that can enhance your portfolio involves looking for stocks with strong fundamentals and growth potential that may not yet be fully recognized by the broader market.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Zona Franca de Iquique | NA | 7.94% | 12.83% | ★★★★★★ |

| SALUS Ljubljana d. d | 13.55% | 13.11% | 9.95% | ★★★★★★ |

| FRoSTA | 8.18% | 4.36% | 16.00% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Standard Bank | 0.13% | 27.78% | 30.36% | ★★★★★★ |

| Aesler Grup Internasional | NA | -17.61% | -40.21% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| MAPFRE Middlesea | NA | 14.56% | 1.77% | ★★★★★☆ |

| Compañía Electro Metalúrgica | 71.27% | 12.50% | 19.90% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

EPC Groupe (ENXTPA:EXPL)

Simply Wall St Value Rating: ★★★★☆☆

Overview: EPC Groupe is involved in the manufacture, storage, and distribution of explosives across Europe, Africa, Asia Pacific, and the Americas with a market capitalization of approximately €408.05 million.

Operations: EPC Groupe generates revenue primarily from its Specialty Chemicals segment, which contributed €487.56 million.

EPC Groupe, a small cap player in the chemicals sector, has shown resilience with earnings growth of 17.4% over the past year, outpacing the industry's -8.2%. Despite trading at 49.8% below estimated fair value, challenges persist as its net debt to equity ratio stands at a high 42.6%, and interest payments are not well covered by EBIT (2.9x). Recent developments highlight EPC's innovative edge; they announced advanced solutions for Microsoft 365 Copilot integration within Fabric, positioning them as leaders in business intelligence consulting and enhancing their data analytics capabilities significantly for clients across North America.

- Click here to discover the nuances of EPC Groupe with our detailed analytical health report.

Review our historical performance report to gain insights into EPC Groupe's's past performance.

Systena (TSE:2317)

Simply Wall St Value Rating: ★★★★★★

Overview: Systena Corporation operates in the solution and framework design, IT service, business solution, and cloud sectors in Japan with a market cap of ¥133.69 billion.

Operations: Systena generates revenue primarily from its Business Solution Business and Solution Design Business, with ¥28.61 billion and ¥19.77 billion respectively. The Framework Design Business contributes ¥7.46 billion to the total revenue stream.

Systena, a dynamic player in the tech industry, has seen its earnings grow 10% annually over the past five years. Despite not outpacing the broader software sector last year, with growth at 10.7%, it remains a solid performer. The company trades at 20% below its estimated fair value and boasts high-quality earnings. Recently, Systena completed a share buyback of approximately 1.33% for ¥1.93 billion and increased its dividend to ¥6 per share from last year's ¥5 per share. Looking ahead, it forecasts net sales between JPY 85-90 billion for fiscal year ending March 2025.

- Get an in-depth perspective on Systena's performance by reading our health report here.

Examine Systena's past performance report to understand how it has performed in the past.

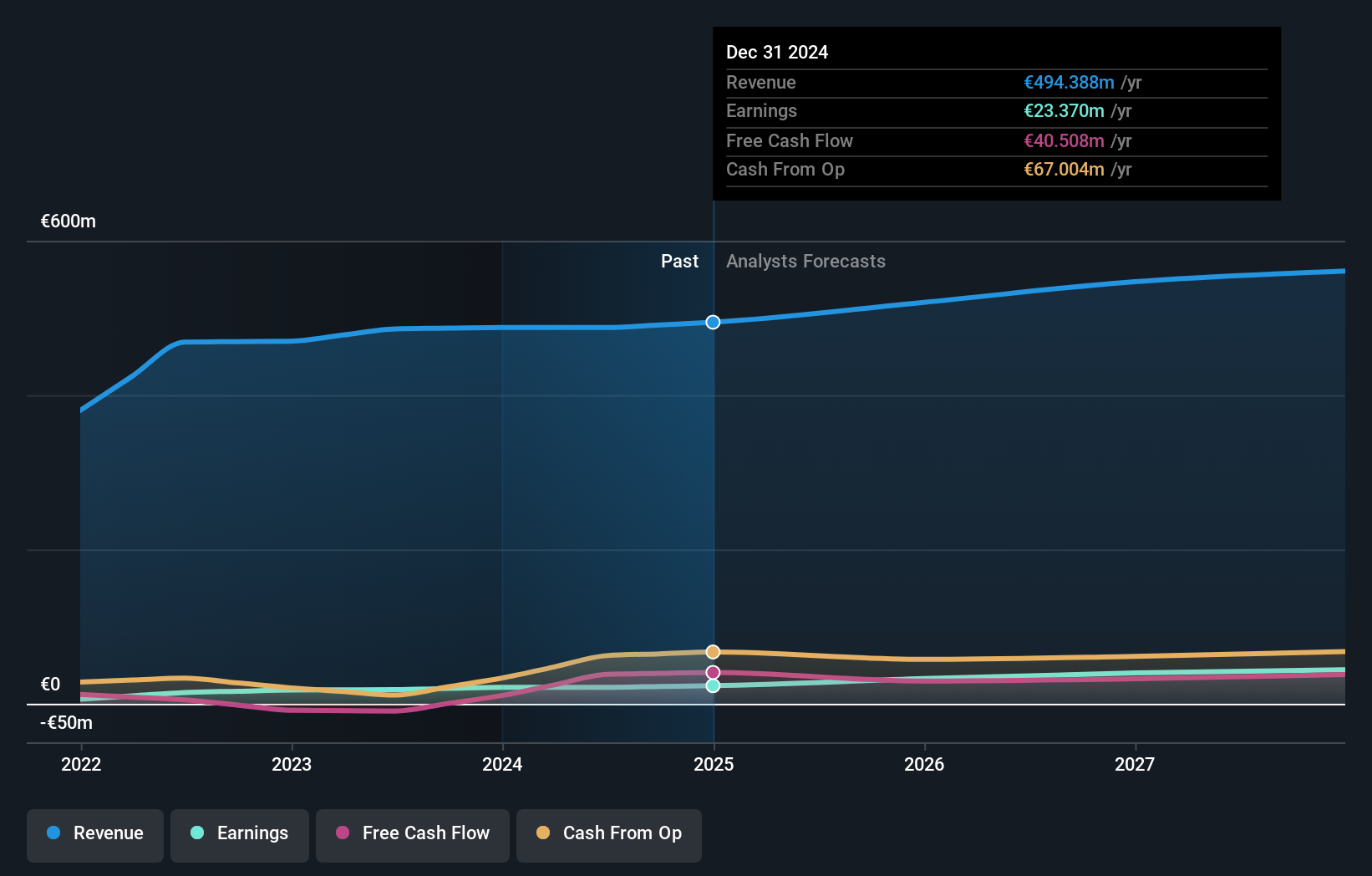

Global Brands Manufacture (TWSE:6191)

Simply Wall St Value Rating: ★★★★★★

Overview: Global Brands Manufacture Ltd. operates in Taiwan, focusing on the production of printed circuit boards and electronic manufacturing services, with a market capitalization of NT$25.47 billion.

Operations: Global Brands Manufacture Ltd. generates revenue primarily from its Printed Circuit Board (PCB) segment, contributing NT$14.10 billion, and its Electronic Manufacturing Service (EMS) segment, which adds NT$7.68 billion. The company's financial performance is significantly influenced by these two segments, reflecting their importance in the overall revenue model.

Global Brands Manufacture, a relatively small player in its sector, showcases high-quality earnings and has managed to reduce its net debt to equity ratio from 63.9% to 49% over five years, reflecting improved financial health. The company trades at about 40.8% below estimated fair value, suggesting potential undervaluation. Despite recent challenges with sales dipping from TWD 6 billion to TWD 5.9 billion and net income falling from TWD 1.2 billion to TWD 901 million year-on-year for Q3, it remains profitable with free cash flow positivity evident in the latest figures of approximately US$2.19 billion as of September 2024.

Make It Happen

- Access the full spectrum of 4621 Undiscovered Gems With Strong Fundamentals by clicking on this link.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:6191

Global Brands Manufacture

Engages in printed circuit boards (PCB) production and electronic manufacturing service (EMS) business in Taiwan.

Excellent balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor