Advertisement

We Think Nippon Computer Dynamics (TYO:4783) Is Taking Some Risk With Its Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Nippon Computer Dynamics Co., Ltd. (TYO:4783) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Nippon Computer Dynamics

What Is Nippon Computer Dynamics's Net Debt?

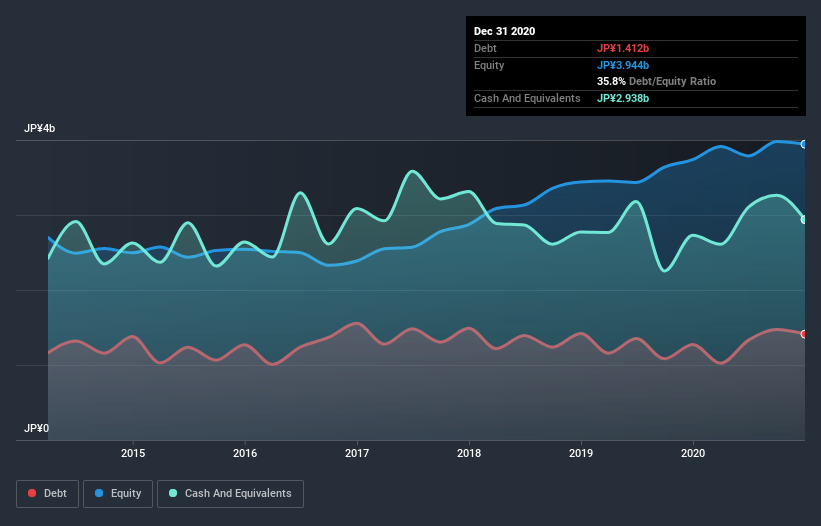

As you can see below, Nippon Computer Dynamics had JP¥578.0m of debt at December 2020, down from JP¥1.27b a year prior. However, its balance sheet shows it holds JP¥2.94b in cash, so it actually has JP¥2.36b net cash.

How Healthy Is Nippon Computer Dynamics' Balance Sheet?

According to the last reported balance sheet, Nippon Computer Dynamics had liabilities of JP¥4.15b due within 12 months, and liabilities of JP¥2.83b due beyond 12 months. Offsetting this, it had JP¥2.94b in cash and JP¥2.22b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by JP¥1.83b.

While this might seem like a lot, it is not so bad since Nippon Computer Dynamics has a market capitalization of JP¥4.96b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. While it does have liabilities worth noting, Nippon Computer Dynamics also has more cash than debt, so we're pretty confident it can manage its debt safely.

The modesty of its debt load may become crucial for Nippon Computer Dynamics if management cannot prevent a repeat of the 56% cut to EBIT over the last year. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. When analysing debt levels, the balance sheet is the obvious place to start. But it is Nippon Computer Dynamics's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Nippon Computer Dynamics has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Nippon Computer Dynamics created free cash flow amounting to 17% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Summing up

Although Nippon Computer Dynamics's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of JP¥2.36b. So while Nippon Computer Dynamics does not have a great balance sheet, it's certainly not too bad. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 3 warning signs we've spotted with Nippon Computer Dynamics .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you’re looking to trade Nippon Computer Dynamics, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if NCD might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSE:4783

NCD

Engages in the system development, support and service, and parking system businesses in Japan.

Flawless balance sheet 6 star dividend payer.

Market Insights

Advertisement

Weekly Picks

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25380.9% overvalued

69 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.4% undervalued

69 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.4% overvalued

11 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

BA

bactrian on Novo Nordisk ·

A Quality Compounder Marked Down on Overblown Fears

Fair Value:US$9542.0% undervalued

95 followersusers have followed this narrative

8 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YI

yiannisz on Etsy ·

Etsy Stock: Defending Differentiation in a World of Infinite Marketplaces

Fair Value:US$64.459.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YI

yiannisz on Align Technology ·

Align Technology Stock: Premium Orthodontics in a Cost-Sensitive World

Fair Value:US$154.623.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.4% undervalued

69 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25380.9% overvalued

69 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0225.6% undervalued

1020 followersusers have followed this narrative

6 commentsusers have commented on this narrative

28 likesusers have liked this narrative

Trending Discussion

ST

StevenM on Excellon Resources ·

Interesting analysis, but the price trajectory assumed for the baseline metals is problematic. These assumptions form the foundation for the entire case, and when compared against historical pricing, don’t appear to be grounded in any reasonable precedent. Even accounting for past commodity super-cycles, inflationary periods, or supply constraints, the forecasted pricing for gold, silver, zinc, and lead are well outside what history would suggest is plausible over comparable timeframes. That creates a fragile premise as the conclusions are driven by aggressive inputs rather than underlying market behavior that is realistic. The analysis would be materially stronger if the price assumptions were anchored to historical ranges and prior cycle peaks, with explicit rationale where the model intentionally departs from those patterns. As it stands, the trajectory feels more aspirational than analytical.

1

|1