Stock Analysis

Discover 3 Japanese Exchange Growth Companies With High Insider Ownership And Up To 83% Earnings Growth

Reviewed by Simply Wall St

Amid a backdrop of modest declines in Japan's stock markets and heightened uncertainty around the Bank of Japan’s monetary policy, investors may find reassurance in growth companies with high insider ownership. These firms often signal strong confidence from those closest to the company's operations, potentially offering stability in turbulent times.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| SHIFT (TSE:3697) | 35.4% | 26.8% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.9% |

| Hottolink (TSE:3680) | 27% | 57.3% |

| Medley (TSE:4480) | 34% | 28.7% |

| Micronics Japan (TSE:6871) | 15.3% | 39.8% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.8% | 44.6% |

| ExaWizards (TSE:4259) | 24.8% | 91.1% |

| AeroEdge (TSE:7409) | 10.7% | 28.5% |

| Soracom (TSE:147A) | 17.2% | 54.1% |

| freee K.K (TSE:4478) | 24% | 81% |

Let's uncover some gems from our specialized screener.

PeptiDream (TSE:4587)

Simply Wall St Growth Rating: ★★★★★☆

Overview: PeptiDream Inc. is a biopharmaceutical company focused on the discovery and development of constrained peptides, small molecules, and peptide-drug conjugate therapeutics, with a market capitalization of approximately ¥326.16 billion.

Operations: The company generates revenue primarily from its biopharmaceutical activities, focusing on novel peptides and molecular therapeutics.

Insider Ownership: 26.1%

Earnings Growth Forecast: 22.3% p.a.

PeptiDream, a Japanese biotech firm, is notable for its high insider ownership and growth trajectory. Recently, the company has made significant strides in clinical research with its first patient dosing in a study targeting renal cell carcinoma, showcasing its innovative peptide technology. Additionally, PeptiDream revised its fiscal year revenue and profit forecasts upward substantially following strategic expansions with Novartis. Despite these positives, the company's share price remains volatile and profit margins have decreased from the previous year.

- Click here to discover the nuances of PeptiDream with our detailed analytical future growth report.

- The analysis detailed in our PeptiDream valuation report hints at an inflated share price compared to its estimated value.

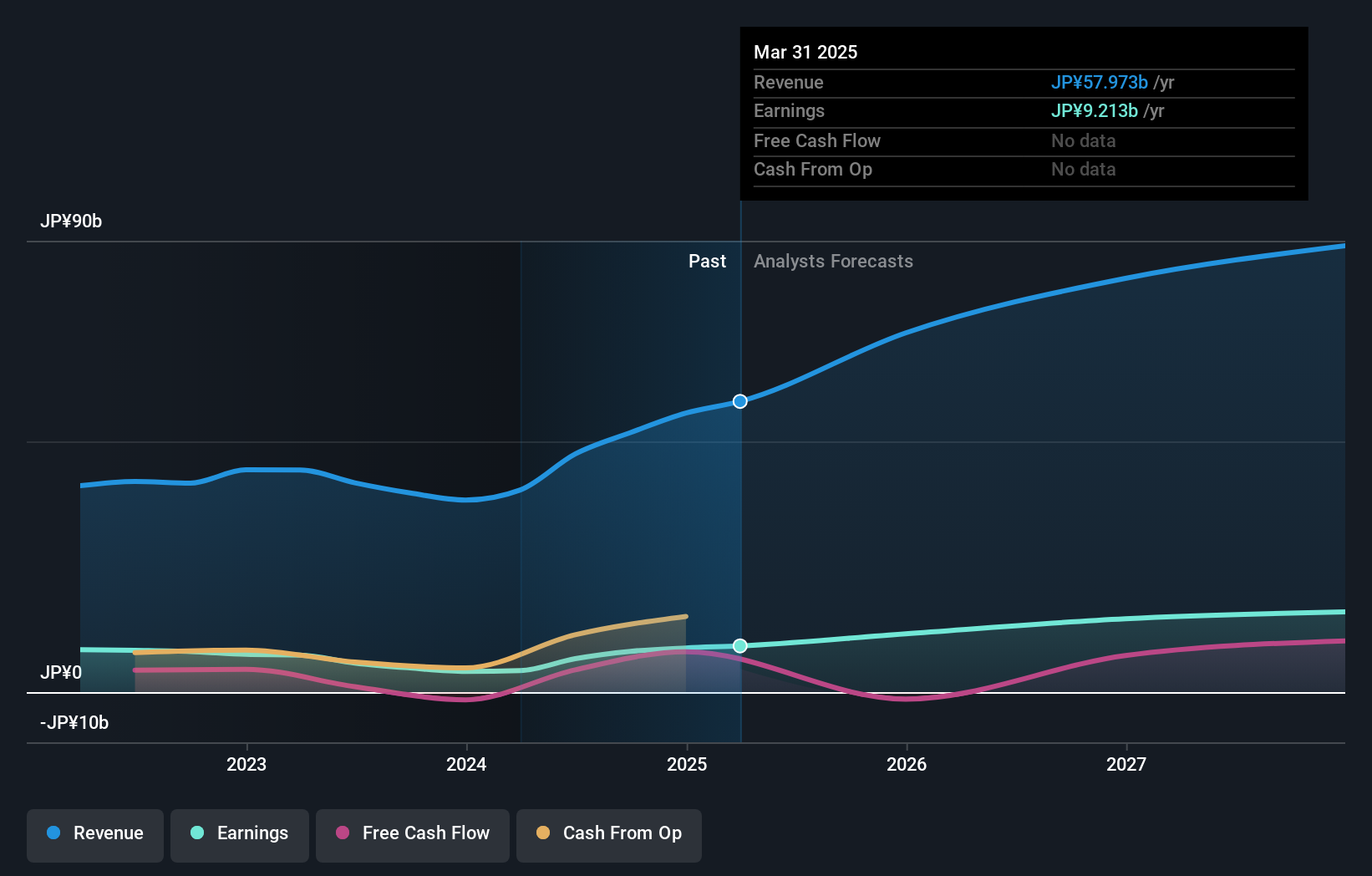

Rakuten Group (TSE:4755)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Rakuten Group, Inc. operates globally, offering e-commerce, fintech, digital content, and communications services with a market capitalization of approximately ¥1.82 trillion.

Operations: The company generates revenue through its diverse operations in e-commerce, fintech, digital content, and communications services.

Insider Ownership: 17.3%

Earnings Growth Forecast: 83.9% p.a.

Rakuten Group is poised for substantial growth, with earnings expected to increase significantly at 83.88% annually. The company forecasts a shift to profitability within three years, outpacing average market growth. Recent activities include a successful $1.99 billion fixed-income offering and robust corporate guidance predicting double-digit revenue growth for 2024, excluding its securities business affected by market volatility. However, its forecasted revenue growth of 7.4% per year, though above the Japanese market average, remains modest compared to high-growth benchmarks.

- Click here and access our complete growth analysis report to understand the dynamics of Rakuten Group.

- Our valuation report here indicates Rakuten Group may be undervalued.

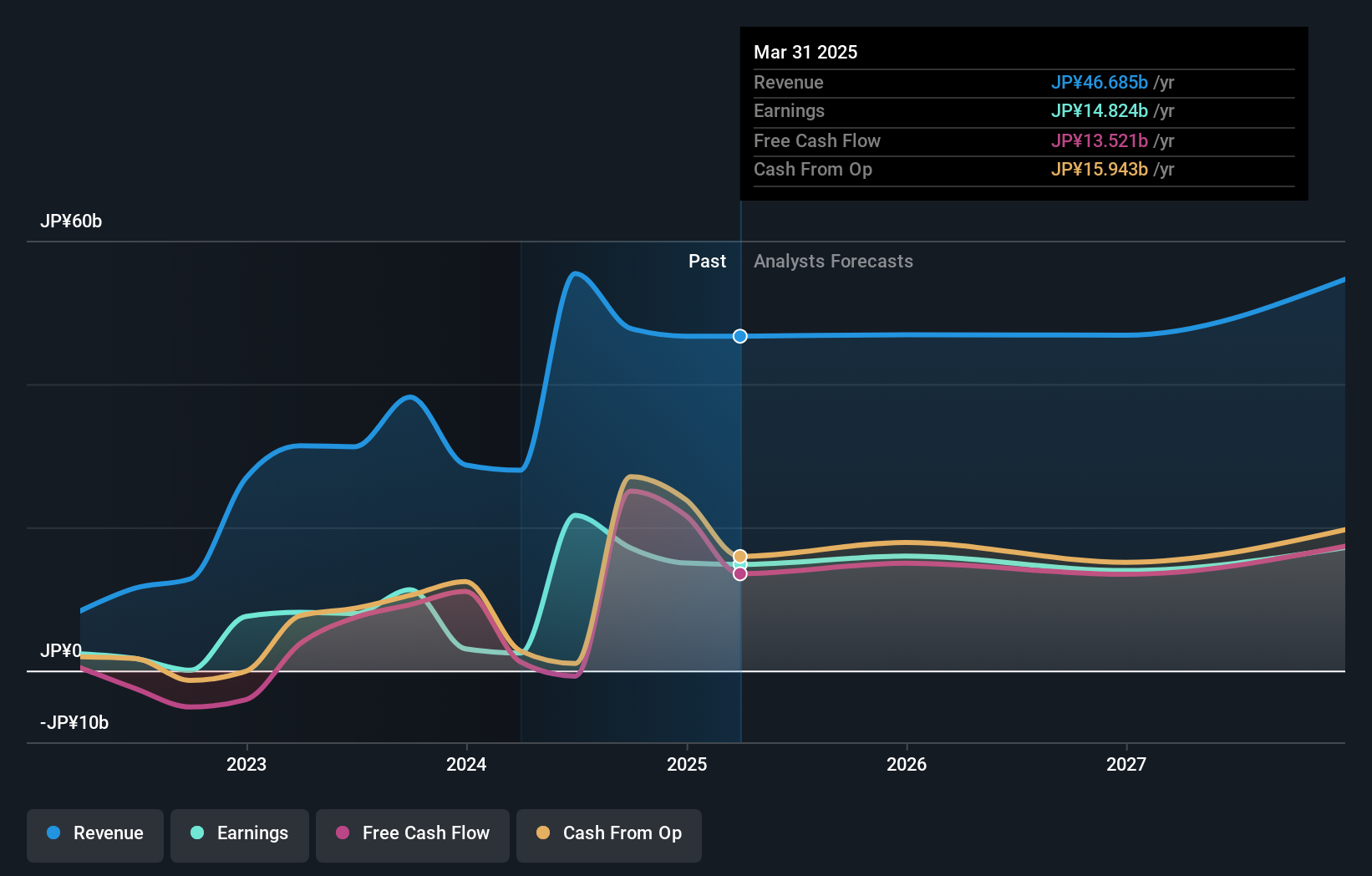

Micronics Japan (TSE:6871)

Simply Wall St Growth Rating: ★★★★★★

Overview: Micronics Japan Co., Ltd. specializes in developing, manufacturing, and selling testing and measurement equipment for semiconductors and LCD systems globally, with a market capitalization of approximately ¥271.22 billion.

Operations: The company primarily generates revenue from the development, manufacture, and sale of semiconductor and LCD testing and measurement equipment.

Insider Ownership: 15.3%

Earnings Growth Forecast: 39.8% p.a.

Micronics Japan is anticipated to experience robust growth, with earnings projected to rise by 39.78% annually, significantly outpacing the Japanese market average. Despite a highly volatile share price in recent months and lower profit margins compared to last year, the company remains well-positioned below analyst price targets by 32.4%, suggesting potential undervaluation. Insider ownership remains stable with no significant buying or selling reported recently, aligning interests with long-term shareholders amidst promising financial forecasts.

- Navigate through the intricacies of Micronics Japan with our comprehensive analyst estimates report here.

- Our expertly prepared valuation report Micronics Japan implies its share price may be lower than expected.

Seize The Opportunity

- Discover the full array of 99 Fast Growing Japanese Companies With High Insider Ownership right here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether PeptiDream is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4587

PeptiDream

A biopharmaceutical company, engages in the discovery and development of constrained peptides, small molecules, and peptide-drug conjugate therapeutics.

High growth potential with adequate balance sheet.